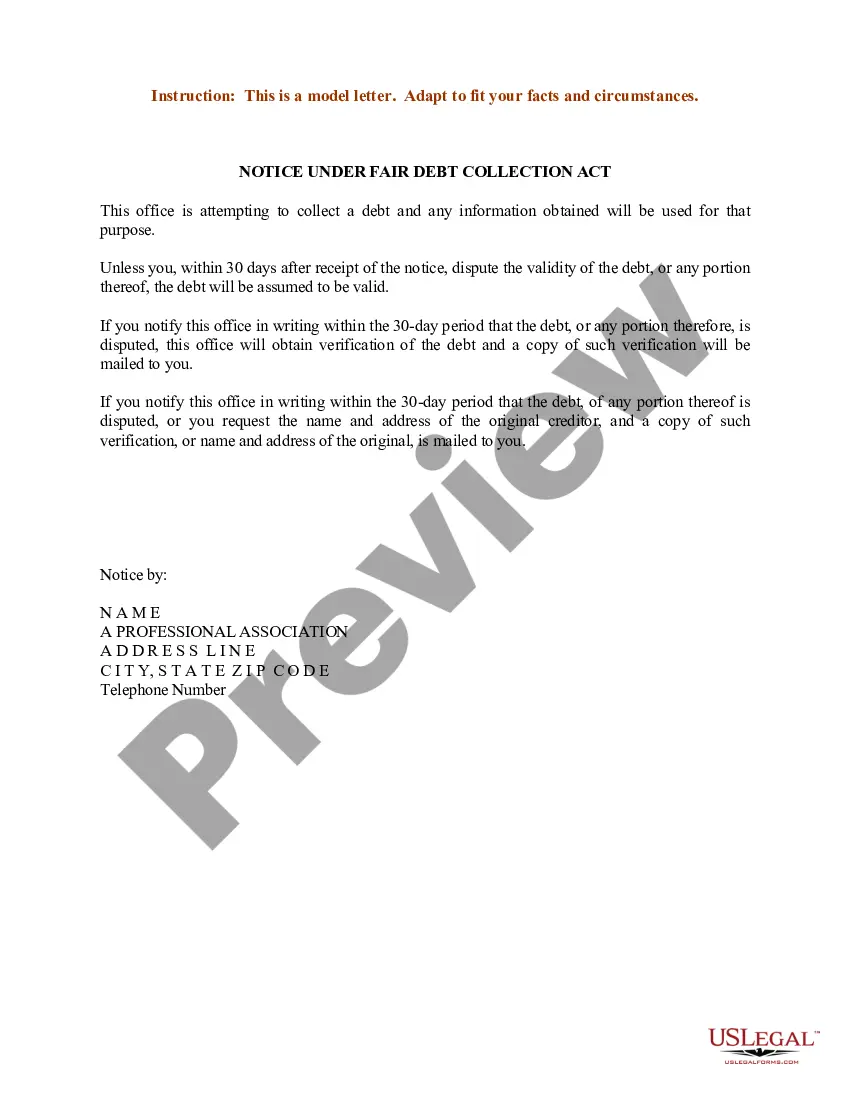

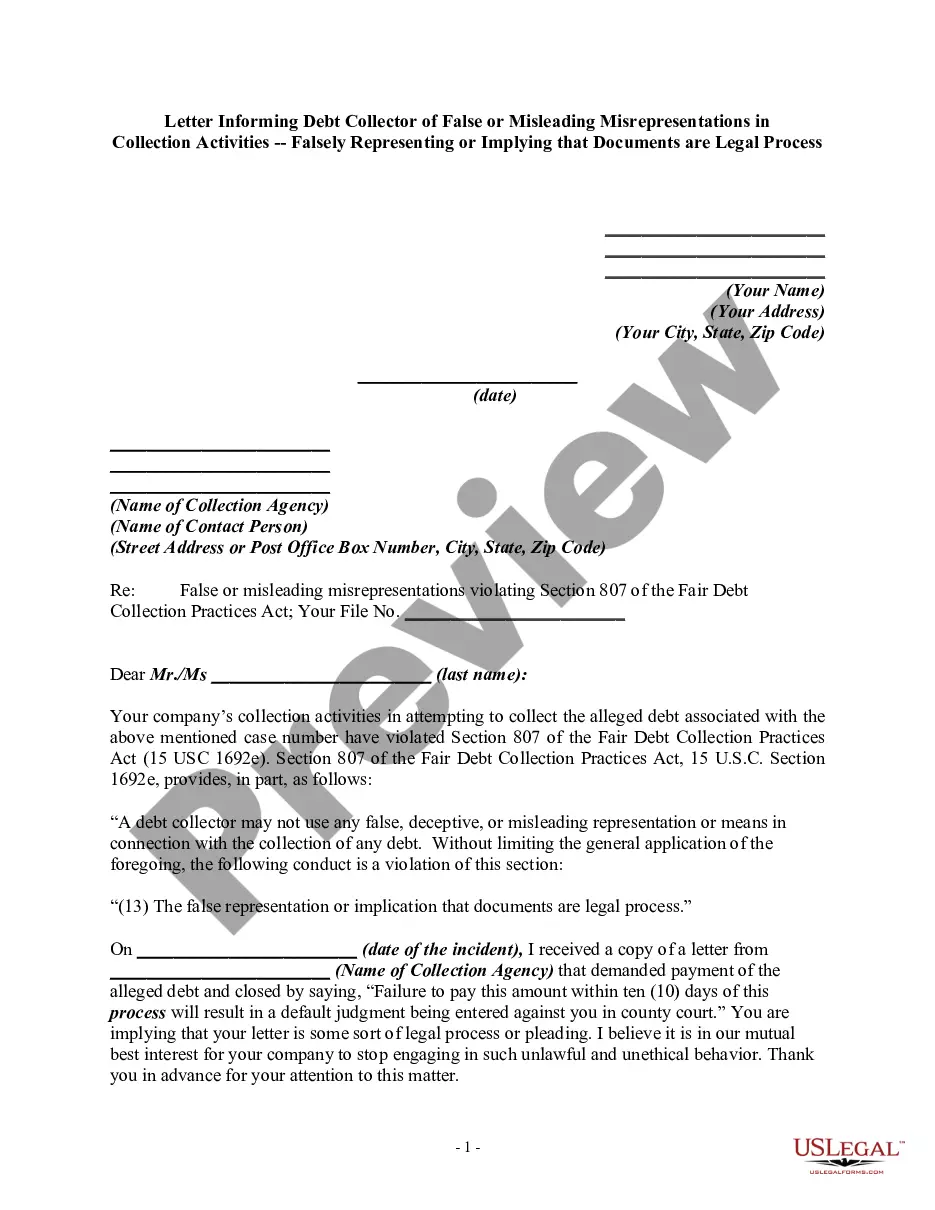

Notice to Debt Collector - Falsely Representing Documents are Not Legal Process or Do Not Require Action

What this document covers

This Notice to Debt Collector form allows consumers to officially notify debt collectors that they have violated the Fair Debt Collection Practices Act (FDCPA). This form is specifically designed to address instances where a debt collector falsely represents documents in a manner that misleads consumers into believing these documents are not legal processes or do not require action. By using this form, consumers can assert their rights under the FDCPA and encourage compliance from debt collectors.

Form components explained

- Name and contact information of the consumer.

- Name and address of the debt collector being notified.

- Description of the specific FDCPA violation.

- Context of the alleged debt and case number.

- A notice of previous actions taken regarding the violations.

- A request for the debt collector to cease misleading practices.

Situations where this form applies

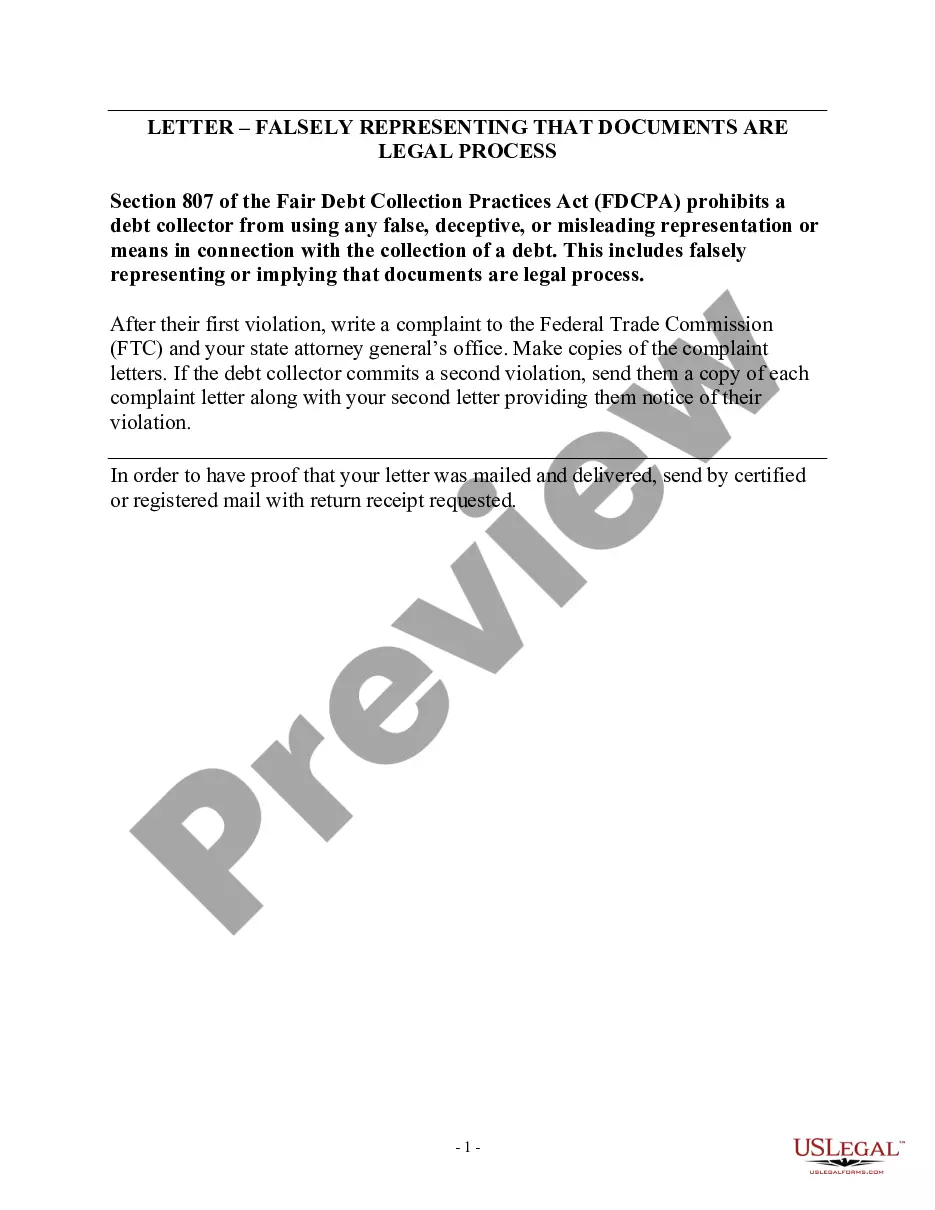

This form should be used if you have received communication from a debt collector that included misleading representations about legal documents or obligations. It is particularly relevant if you believe that the debt collector has violated Section 807 of the FDCPA, which prohibits deceptive practices in debt collection. Utilizing this form sends a clear message to the debt collector about your awareness of your rights and their obligations under federal law.

Who should use this form

This form is intended for:

- Individuals who are being contacted by debt collectors.

- Consumers who believe they have been misled regarding the nature of legal documents related to debts.

- Anyone seeking to assert their rights under the Fair Debt Collection Practices Act (FDCPA).

- Individuals considering legal action due to unfair debt collection practices.

Completing this form step by step

- Identify your name and address at the top of the letter.

- Include the name and address of the debt collector.

- Specify the case number and describe the nature of the violation in your own words.

- State your previous communications with the debt collector regarding this issue.

- Sign and date the notice before sending it to the debt collector.

- Send the notice using certified or registered mail with a return receipt requested.

Does this document require notarization?

Notarization is not commonly needed for this form. However, certain documents or local rules may make it necessary. Our notarization service, powered by Notarize, allows you to finalize it securely online anytime, day or night.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Not providing sufficient detail about the violation.

- Failing to include the case number.

- Sending the notice without using certified mail.

- Not keeping copies of the correspondence for your records.

- Assuming the debt collector will stop contacting you without following up.

Benefits of completing this form online

- Convenient access to professionally drafted legal templates.

- Editable forms to accommodate specific details and scenarios.

- Reliable formatting to ensure compliance with legal standards.

- Immediate download for quick use, helping you address issues promptly.

Legal use & context

- This form protects consumers under the FDCPA against misleading debt collection practices.

- It serves as a formal complaint that can be used to support further legal action if necessary.

- Understanding your rights can significantly impact how debt collectors approach your case.

Main things to remember

- The form is essential for notifying debt collectors of unfair practices.

- Clear documentation can enhance your ability to challenge misleading collection tactics.

- Take prompt action to assert your consumer rights under the FDCPA.

Looking for another form?

Form popularity

FAQ

Can You Sue a Company for Sending You to Collections? Yes, the FDCPA allows for legal action against certain collectors that don't comply with the rules in the law. If you're sent to collections for a debt you don't owe or a collector otherwise ignores the FDCPA, you might be able to sue that collector.

Under the Fair Debt collection Practices Act (FDCPA), I have the right to request validation of the debt you say I owe you. I am requesting proof that I am indeed the party you are asking to pay this debt, and there is some contractual obligation that is binding on me to pay this debt.

Debt validation is your federal right granted under the Fair Debt Collection Practices Act (FDCPA). To request debt validation, you must send a written request to the debt collector within 30 days of being contacted by the collection agency.

Write a letter disputing the debt. You have 30 days after receiving a collection notice to dispute a debt in writing. Dispute the debt on your credit report. Lodge a complaint. Respond to a lawsuit. Hire an attorney.

Because the FDCPA is designed to protect debtors against third-party debt collectors, it doesn't apply to your original creditor or its employees.

Your dispute should be made in writing to ensure that the debt collector has to send you verification of the debt. If you're having trouble with debt collection, you can submit a complaint with the CFPB online or by calling (855) 411-CFPB (2372).

Your dispute should be made in writing to ensure that the debt collector has to send you verification of the debt. If you're having trouble with debt collection, you can submit a complaint with the CFPB online or by calling (855) 411-CFPB (2372).

Challenging the debt: You have a right to dispute the debt. If you challenge the debt within 30 days of first contact, the collector cannot ask for payment until the dispute is settled. After 30 days you can still challenge the debt, but the collector can seek payment while the dispute is being investigated.

Reach out to the company the collector says is the original creditor. They might help you figure out if the debt is legitimate and if this collector has the right to collect the debt. Also, get your free, annual credit report online or at 877-322-8228 and see if the debt shows up there. Dispute the debt in writing.