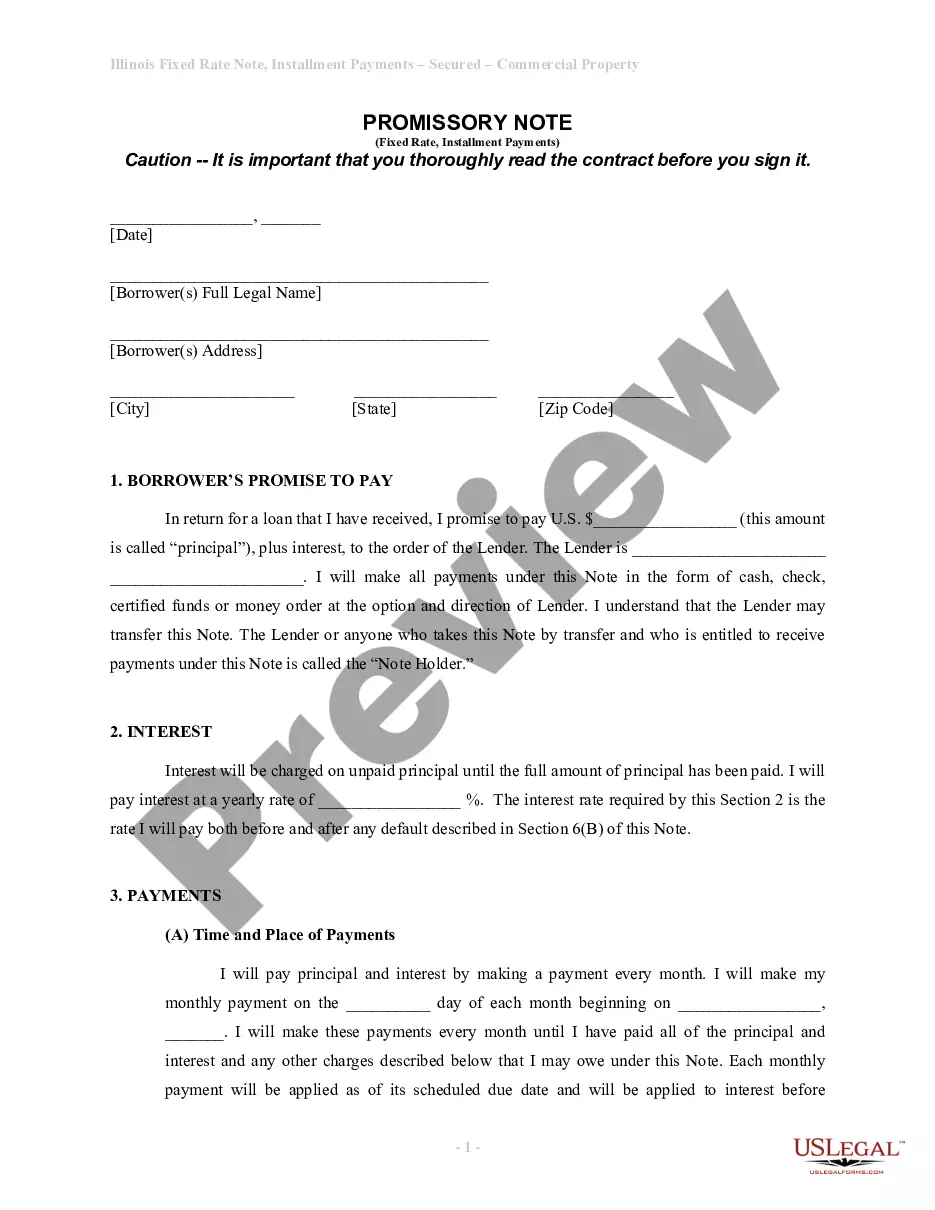

Illinois Installments Fixed Rate Promissory Note Secured by Personal Property

What is this form?

The Illinois Installments Fixed Rate Promissory Note Secured by Personal Property is a legal document that formalizes a loan agreement where the borrower promises to repay a specified principal amount along with interest, secured by personal property. This note differs from unsecured promissory notes as it requires collateral, providing additional security for the lender in case of default.

Main sections of this form

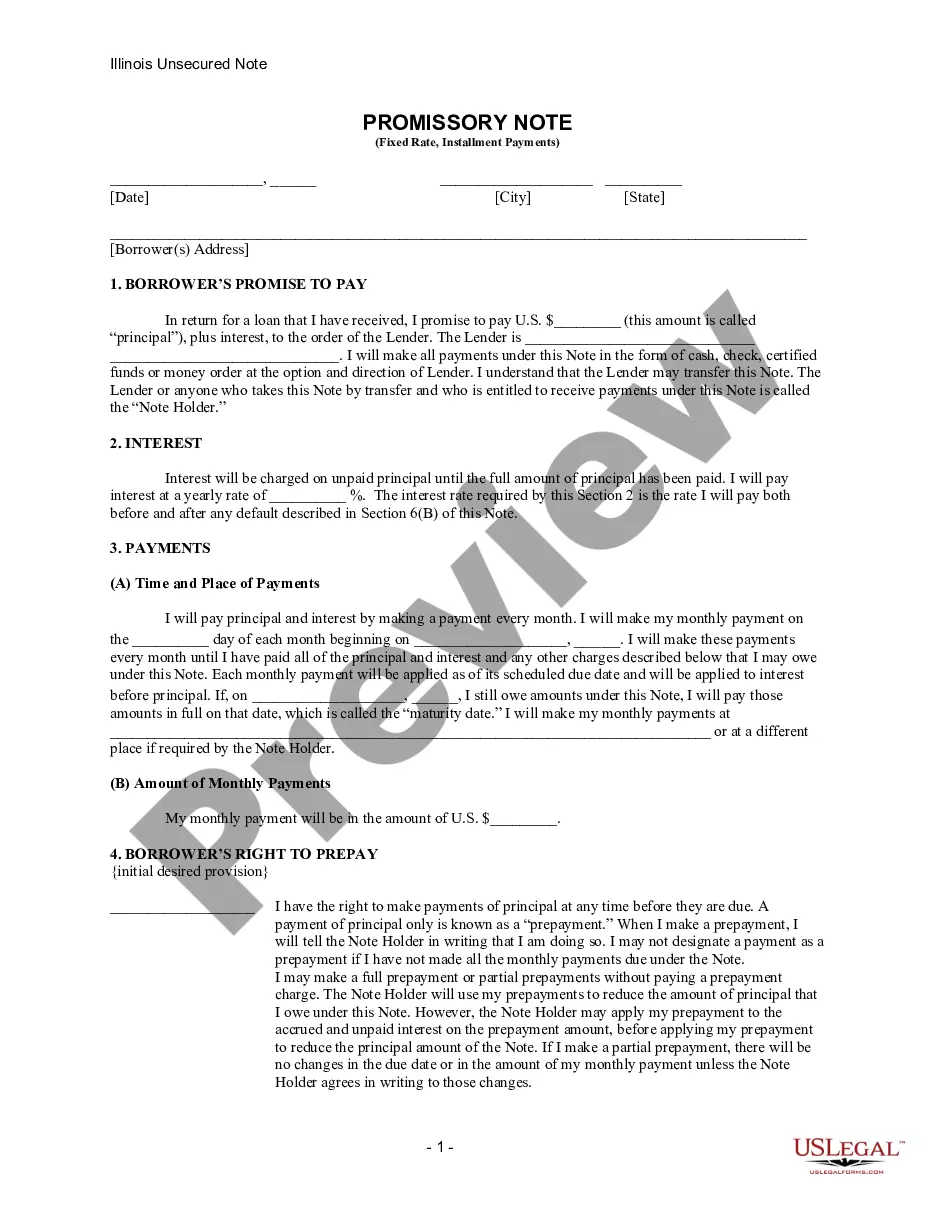

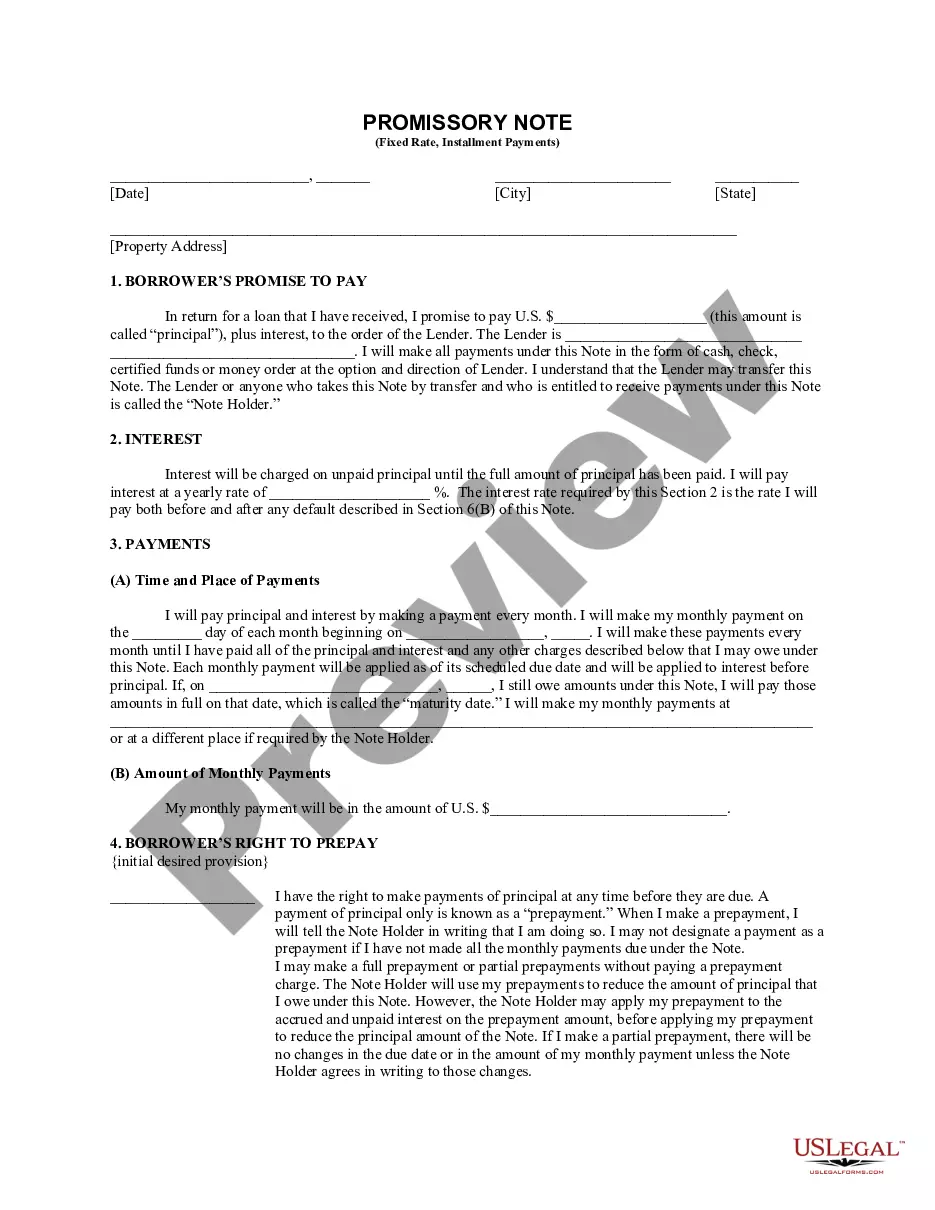

- Borrower's promise to pay: Details the borrower's commitment to repay the loan amount plus interest.

- Interest rate: Specifies the annual interest rate applicable to the loan.

- Payment schedule: Outlines the frequency of payments and the maturity date of the loan.

- Prepayment options: Allows the borrower to make extra payments without penalties under certain conditions.

- Late payment penalties: Defines the fees incurred for late payments.

- Secured agreement: States that the loan is secured by personal property, as detailed in a separate agreement.

Situations where this form applies

This form is used when an individual or business needs to obtain a loan and wishes to secure that loan with personal property, such as vehicles or equipment. It is especially useful when traditional unsecured loans are unavailable or when the lender requires additional security to mitigate risk.

Who needs this form

- Individuals seeking personal loans that require collateral.

- Businesses that need financing and are willing to offer personal property as security.

- Lenders who want to formalize a loan arrangement with collateral protection.

- Guarantors or endorsers involved in secured loans.

How to complete this form

- Identify the parties: Clearly state the names and addresses of the borrower and lender.

- Specify the loan amount: Enter the principal amount to be borrowed.

- Set the interest rate: Input the applicable annual interest rate.

- Outline payment details: Indicate the monthly payment amount and the payment due date.

- Include security details: Describe the personal property used as collateral and attach the separate security agreement.

- Sign and date: Ensure that all parties sign the document in the designated areas to make it legally binding.

Is notarization required?

This form does not typically require notarization unless specified by local law. However, having the document notarized can add an extra layer of authenticity and protection for both parties in the agreement.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to specify the collateral properly.

- Leaving important fields such as interest rate or payment amount blank.

- Not providing correct contact information for the lender.

- Overlooking the need for both parties to sign the document.

- Ignoring local laws regarding payment penalties or maximum interest rates.

Advantages of online completion

- Convenient access to legal templates drafted by licensed attorneys.

- Easy to download and customize according to individual needs.

- Secure and reliable documents available at your fingertips.

- Time-saving process compared to traditional legal consultation.

Legal use & context

- This promissory note legally binds the borrower to repay the loan under the specified terms.

- It provides the lender with collateral, which can be reclaimed if the borrower defaults.

- Failure to comply with the note may lead to legal consequences, including potential loss of the secured property.

Key takeaways

- The Illinois Installments Fixed Rate Promissory Note is essential for secured lending agreements.

- Proper completion of the form ensures legal enforceability and clarity of terms.

- Both borrowers and lenders should understand their rights and obligations under the agreement.

Looking for another form?

Form popularity

FAQ

No. California promissory notes do not need to be notarized or witnessed for validity.

Promissory notes are legally binding whether the note is secured by collateral or based only on the promise of repayment. If you lend money to someone who defaults on a promissory note and does not repay, you can legally possess any property that individual promised as collateral.

Writing the Promissory Note Terms You don't have to write a promissory note from scratch. You can use a template or create a promissory note online.

Although a promissory note is usually written on a computer and printed out or a pre-made form is filled out, a handwritten promissory note signed by both parties is legal and will stand up in court.

Promissory notes are a valuable legal tool that any individual can use to legally bind another individual to an agreement for purchasing goods or borrowing money. A well-executed promissory note has the full effect of law behind it and is legally binding on both parties.

Write the date of the writing of the promissory note at the top of the page. Write the amount of the note. Describe the note terms. Write the interest rate. State if the note is secured or unsecured. Include the names of both the lender and the borrower on the note, indicating which person is which.

A promissory note is a contract, a binding agreement that someone will pay your business a sum of money. However under some circumstances if the note has been altered, it wasn't correctly written, or if you don't have the right to claim the debt then, the contract becomes null and void.

Promissory notes are typically recorded as public documents and accessible shortly after the closing. The trustee maintains the original deed until the loan is satisfied. When the loan is paid off, the trustee automatically records a deed of reconveyance at the county recorder's office for safekeeping.

Promissory notes are legally binding whether the note is secured by collateral or based only on the promise of repayment. If you lend money to someone who defaults on a promissory note and does not repay, you can legally possess any property that individual promised as collateral.