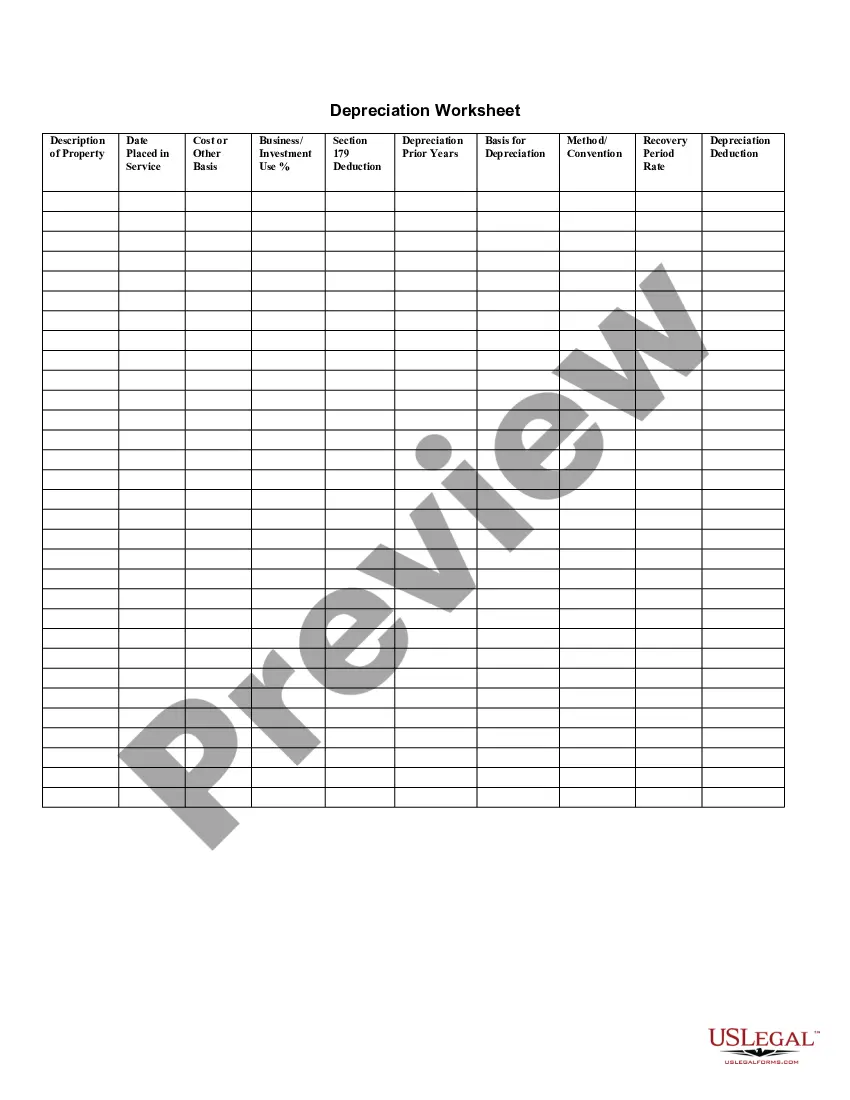

Depreciation Schedule

Understanding this form

The depreciation schedule is a legal form that outlines how a business calculates and tracks the depreciation of its assets over time. This form serves to document the decrease in value of assets, facilitating accurate financial reporting and tax compliance. Unlike simpler forms, the depreciation schedule is designed for meticulous record-keeping of asset value adjustments, ensuring that businesses maintain transparency in their financial affairs.

Form components explained

- Basis: Initial value of the asset before depreciation.

- Depreciation Value: Estimated decrease in asset value over a specified period.

When to use this document

This form is essential for businesses that need to report their asset values accurately for accounting and taxation purposes. It should be used when a business acquires new fixed assets or when an existing asset's value needs reevaluation. Moreover, during tax season, having an up-to-date depreciation schedule helps ensure that all allowable deductions are claimed.

Who should use this form

- Small business owners tracking their asset depreciation.

- Accountants preparing financial statements for clients.

- Tax professionals assisting clients with tax deductions related to depreciation.

- Financial analysts evaluating the worth of a businessâs assets.

How to complete this form

- Identify the assets that require depreciation tracking.

- Determine the purchase price or basis of each asset.

- Calculate the depreciation value for each asset based on applicable methods.

- Document the details on the schedule, ensuring all sections are filled out accurately.

- Review the completed form for any errors before submission or filing.

Notarization guidance

This form does not typically require notarization unless specified by local law. It is advisable to check specific state regulations to confirm.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to include all assets that need depreciation.

- Incorrectly calculating the depreciation value.

- Not updating the schedule after asset improvements or disposals.

- Overlooking state-specific regulations affecting depreciation.

Advantages of online completion

- Convenient access to templates that can be completed digitally.

- Easy editing features allow for quick updates and revisions.

- Formatted by licensed attorneys to ensure compliance and accuracy.

Looking for another form?

Form popularity

FAQ

Claim your deduction for depreciation and amortization. Make the election under section 179 to expense certain property. Provide information on the business/investment use of automobiles and other listed property.

Depreciation of rental property is generally reported on Schedule E of a standard 1040, although there are situations in which you would use other forms. For example, Form 4562 may be used if you claim depreciation on a property in the year that you put it into service as a rental property.

You are only obligated to file Form 4562 if you're deducting a depreciable asset on your tax return. A depreciable asset is anything you buy for your business that you plan on using for more than one financial year.You'll need to file Form 4562 for every year that you continue to depreciate your asset.

There is no such thing as deferred depreciation. Depreciation as an expense must be taken in the year that it occurs. Depreciation occurs each year, as defined by the IRS guidelines, whether you choose to claim it as an expense or not.

Determine the cost of the asset. Subtract the estimated salvage value of the asset from the cost of the asset to get the total depreciable amount. Determine the useful life of the asset. Divide the sum of step (2) by the number arrived at in step (3) to get the annual depreciation.

You are only obligated to file Form 4562 if you're deducting a depreciable asset on your tax return. A depreciable asset is anything you buy for your business that you plan on using for more than one financial year.You'll need to file Form 4562 for every year that you continue to depreciate your asset.

The straight-line method is the simplest and most commonly used way to calculate depreciation under generally accepted accounting principles. Subtract the salvage value from the asset's purchase price, then divide that figure by the projected useful life of the asset.

Make sure your asset is eligible. To qualify for a Section 179 deduction, your asset must be: Tangible. Start using the asset. Section 179 rules require you to start using the asset in your business to take the deduction. Claim the deduction. You claim the Section 179 deduction on Part I of Form 4562.

Use Form 4562 to: Claim your deduction for depreciation and amortization. Make the election under section 179 to expense certain property. Provide information on the business/investment use of automobiles and other listed property.