Fixed Asset Removal Form

Overview of this form

The Fixed Asset Removal Form is a business document designed for companies to formally request the removal of fixed assets from their premises. This form is essential for tracking the status of company property and ensuring accountability among employees. Unlike other asset-related forms that may simply record asset transfers, this form specifically addresses the return or removal of assets, facilitating proper record-keeping and compliance with company policies.

Key parts of this document

- Identification of the fixed asset being removed.

- Employee authorization for the deduction of property costs from wages if the asset is not returned.

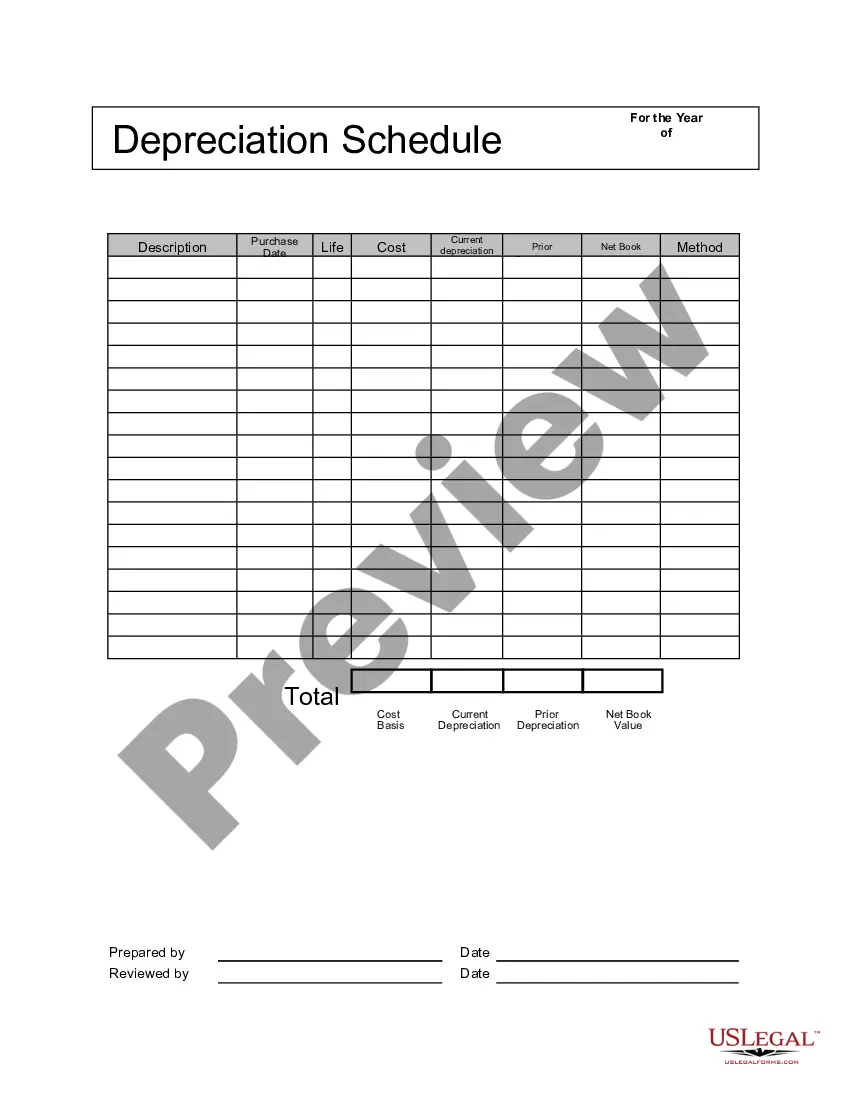

- Net book value calculation definition to determine the financial implications.

- Department manager's authorization section to approve the asset removal.

- Expiration date clause applicable to the removal process.

When to use this form

This form should be used when an employee plans to remove a fixed asset from the company's premises. It is particularly relevant in situations such as an employee leaving the company, transferring assets for legitimate business reasons, or when assets are no longer needed. By utilizing this form, companies can ensure that the removal process is documented, authorized, and compliant with internal policies.

Who can use this document

- Employees intending to remove fixed assets from their workplace.

- Department managers overseeing asset inventory and removal processes.

- Human resources personnel involved in employee transitions and asset management.

Steps to complete this form

- Identify the specific fixed asset that is being removed and provide details.

- Fill in the employee's information, including name and employment details.

- Specify the net book value for the asset as of the termination or removal date.

- Obtain the necessary authorization from the department manager.

- Submit the completed form to the designated contact in the company.

Notarization requirements for this form

Notarization is generally not required for this form. However, certain states or situations might demand it. You can complete notarization online through US Legal Forms, powered by Notarize, using a verified video call available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to provide accurate descriptions of the fixed assets.

- Not obtaining the necessary managerial authorization before submitting.

- Omitting crucial details regarding the net book value.

- Submitting the form after the stipulated expiration date.

Benefits of using this form online

- Convenient access for easy completion and submission.

- Editability allows users to correct information effortlessly.

- Reliable templates drafted by licensed attorneys ensure legal robustness.

Legal use & context

- Proper documentation helps prevent disputes over asset ownership.

- The form provides a clear trail of authorization for financial accountability.

- Using the form mitigates risks associated with unreturned company property.

Main things to remember

- The Fixed Asset Removal Form is crucial for formalizing asset removals.

- It protects both employees and the business by clearly outlining responsibilities.

- Always ensure accurate information and proper authorization before submission.

Looking for another form?

Form popularity

FAQ

When a fixed asset is eventually disposed of, the event should be recorded by debiting the accumulated depreciation account for the full amount depreciated, crediting the fixed asset account for its full recorded cost, and using a gain or loss account to record any remaining difference.

The scrap value can also be used to calculate the depreciation expense. Using our example above, if the company estimated a $3,000 residual value for the machinery at the end of 8 years, then it can calculate its depreciation expense per year to be ($75,000 - $3,000) / 8 = $9,000.

The entry to remove the asset and its contra account off the balance sheet involves decreasing (crediting) the asset's account by its cost and decreasing (crediting) the accumulated depreciation account by its account balance.

Disposal of an Asset The machine's book value or disposal value can be calculated by subtracting from original cost, its depreciated cost. For instance, the depreciation value of machine at time of sale is $4000, means its book value is $1000. The company will try to sell the machine at least at its book value.

You can scrap an asset anytime using the "Scrap Asset" button in the Asset record. You will be asked for confirmation, click on Yes and the asset will be scrapped. The "Gain/Loss Account on Asset Disposal" account mentioned in the Company is debited by the Current Value (After Depreciation) of the asset.

Derecognition of an asset occurs whenever an asset is disposed of or is not expected to provide any future benefits from either its use or disposal. As a result, the asset is removed from the financial statements. Disposal of a long-lived operating asset is effected by selling it, exchanging it, or abandoning it.

Debit cash for the amount received, debit all accumulated depreciation, debit the loss on sale of asset account, and credit the fixed asset. Gain on sale. Debit cash for the amount received, debit all accumulated depreciation, credit the fixed asset, and credit the gain on sale of asset account.

Write off an asset when it is determined that it is no longer useful. The journal entry is as follows: Credit (asset to be written off), Debit (accumulated depreciation), and Debit (loss on disposal).

Another way to write-off the asset is providing for a reduction in carrying value of the asset. This amount is usually charged to expense as it is considered as the cost of doing business. The term writes off refers to the value of the asset, the amount is written off and not the asset itself.