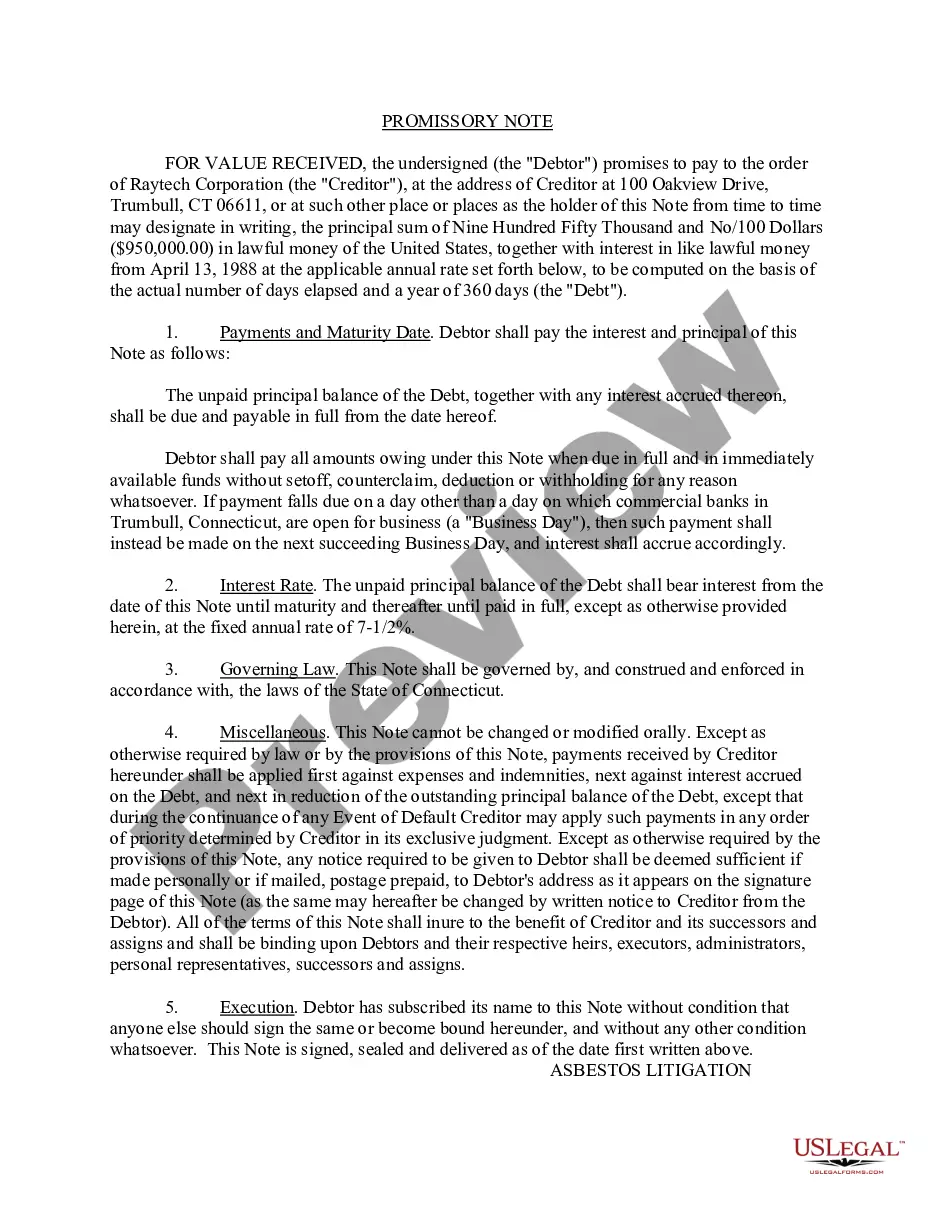

Bridge Financing Promissory Note

Overview of this form

The Bridge Financing Promissory Note is a legal document used when a company, known as the Maker, borrows funds from bridge investors on a term loan basis. Unlike other forms of notes that may require immediate repayment, this promissory note specifies a scheduled due date for repayment. It can be tailored to be either secured or unsecured, depending on the agreement with the investors. This form is particularly useful for businesses seeking temporary financial support while transitioning to longer-term financing options.

What’s included in this form

- Details of the parties involved: The Maker (company) and the Payee (investor).

- Principal amount and interest rate applicable to the loan.

- Maturity date specifying when the full amount is due.

- Conditions under which the loan may convert into company shares.

- Options for secured or unsecured notes and related clauses.

- Provisions for legal jurisdiction and dispute resolution.

Situations where this form applies

This form is suited for scenarios where a business needs immediate financial support before securing long-term financing. It is typically used during transitional phases, such as when preparing for a larger capital raise or during interim periods when cash flow is needed urgently. Companies facing a liquidity event or those seeking to bridge financing gaps should utilize this specific promissory note form.

Intended users of this form

- Business owners seeking temporary financing to support operations or growth.

- Investors looking to secure a loan agreement with a company for potential equity conversion.

- Legal professionals advising clients on bridge financing options.

- Startups in need of immediate funds before longer-term financing arrangements.

How to prepare this document

- Identify the parties: Enter the names of the Maker (company) and Payee (investor).

- Specify the amount: Fill in the principal loan amount to be borrowed.

- Enter the interest rate: Indicate the applicable interest rate for the loan.

- Set the maturity date: Input the due date for the repayment of the loan.

- Check security provisions: Decide if the note will be secured or unsecured and include any necessary details.

Does this form need to be notarized?

This form usually doesn’t need to be notarized. However, local laws or specific transactions may require it. Our online notarization service, powered by Notarize, lets you complete it remotely through a secure video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to specify a clear maturity date, leading to confusion over repayment timelines.

- Not accurately defining the interest rate, which could result in disputes later.

- Leaving out essential party details, such as correct names and addresses.

- Neglecting to clarify whether the note is secured or unsecured, which can affect the repayment terms.

Benefits of using this form online

- Convenience: Easily access and download the form from any location.

- Editability: Customize the template to fit specific business needs before finalizing.

- Reliability: Forms are drafted by licensed attorneys to ensure compliance with legal standards.

- Speed: Quickly fill out the document without the need for legal consultations, saving time on legal processes.

Legal use & context

- The promissory note is a binding contract that may be enforced in a court of law.

- Both the Maker and Payee have legal obligations under the terms specified in the note.

- Particular attention should be given to the conversion clauses to ensure they comply with relevant securities regulations.

Summary of main points

- The Bridge Financing Promissory Note is essential for businesses needing quick financial support.

- This form offers flexibility in terms of security and repayment structure.

- It is important to clearly define all terms to avoid legal disputes.

Looking for another form?

Form popularity

FAQ

A bridge loan is a type of short-term loan that may be used in real estate transactions when the buyer lacks the funds to finance the purchase of the new property without the prior sale of the first property.

Bridge loans typically have interest rates between 8.5% and 10.5%, making them more expensive than traditional, long-term financing options. However, the application and underwriting process for bridge loans is generally faster than for traditional loans.

Typically, the cost for bridge financing is between $1,000 and $2,000.

Melanie Bien at mortgage broker Private Finance says bridging finance has its uses, but adds that if you don't have a realistic exit strategy, such as a buyer lined up for your own property, "bridging is extremely risky and should be avoided at all costs".

A bridge loan is a temporary financing option designed to help homeowners bridge the gap between the time your existing home is sold and your new property is purchased. It enables you to use the equity in your current home to pay the down payment on your next home, while you wait for your existing home to sell.

To determine the amount of a bridge loan, take the purchase price of the new house, then subtract the value of the mortgage and the initial deposit. The leftover amount is the sum that will need to be financed until a sale is complete.

They could range from around 0.4% to 2%. Unlike a mortgage, bridge loans don't last very long. They're essentially meant to 'tide you over' for a few weeks or months. As they are short term, bridging loans usually charge monthly interest rates rather than an annual percentage rate (APR).

It is usually issued by an investment bank or venture capital firm. Equity financing (equity-for-capital swap) can also be an option for those seeking bridge financing. In all cases, bridge loans are expensive because lenders bear a significant portion of default risk loaning the funds for a short period.