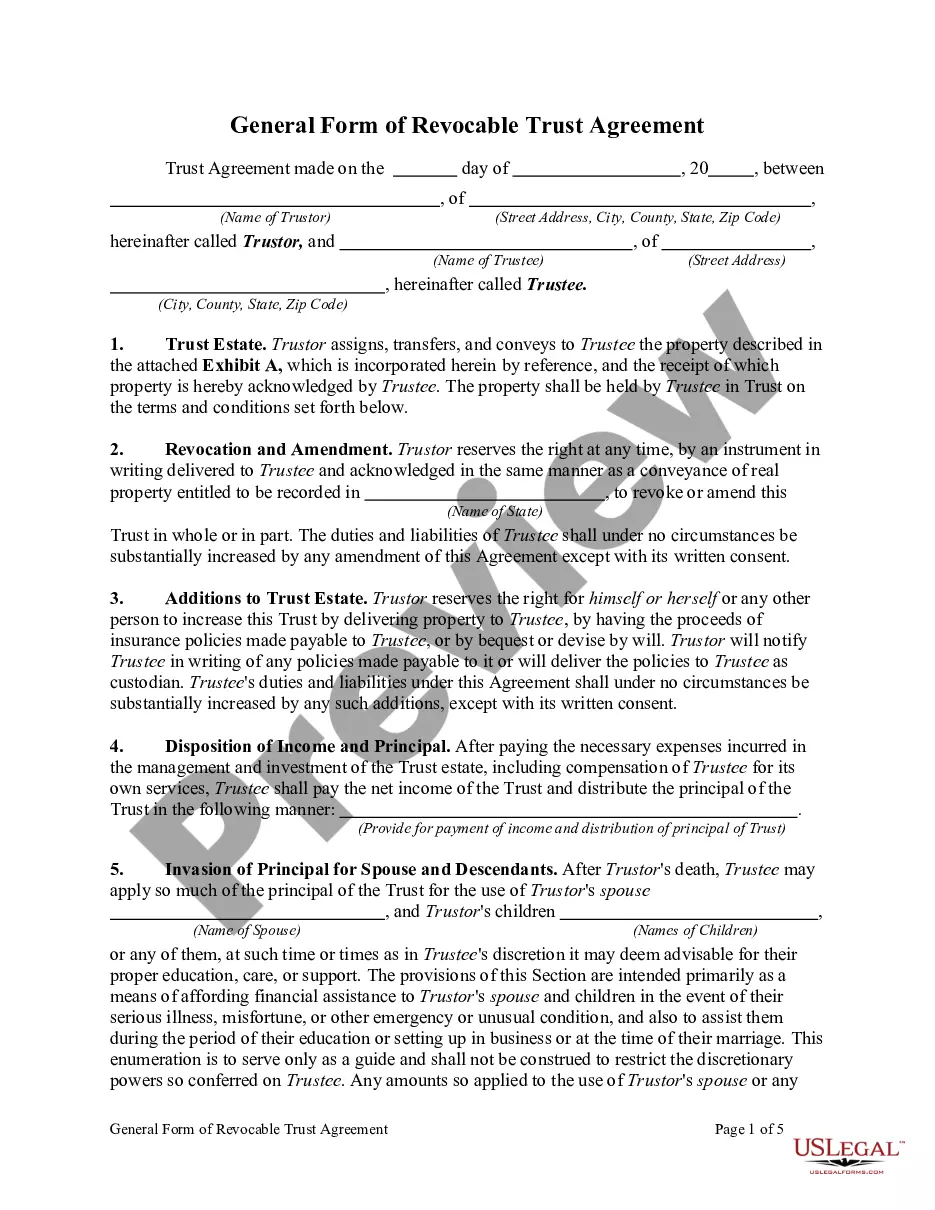

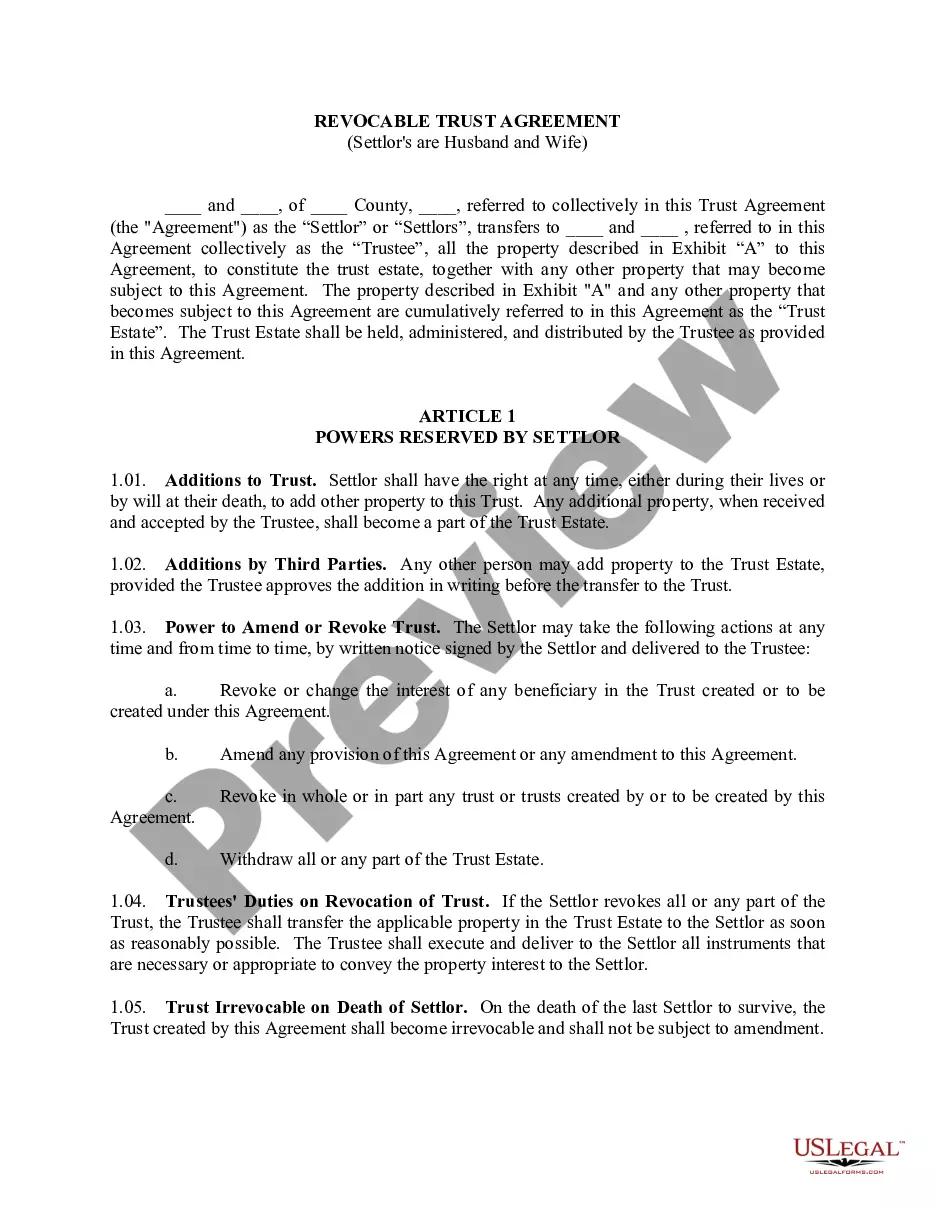

Revocable Trust Agreement Regarding Coin Collection

What is this form?

The Revocable Trust Agreement Regarding Coin Collection is a legal document that establishes a trust to manage a collection of coins. This type of trust allows the person who creates it, known as the Grantor, to retain control over the assets during their lifetime while specifying how the collection will be managed and distributed after their death. Unlike other trust agreements, this one focuses specifically on the administration and protection of a coin collection, making it a unique tool for estate planning and asset management.

Form components explained

- Identification of the Trustor and Trustee, along with their addresses.

- Purpose and powers of the Trustee to manage the coin collection.

- Rules for adding to the collection and revoking/amending the trust.

- Instructions for the administration of the trust during and after the Trustorâs life.

- Distribution guidelines for beneficiaries upon the Trustor's death.

Common use cases

This form is useful when an individual wants to manage their coin collection as part of their estate planning. It addresses not only the handling of the collection while the Grantor is living but also the specific distribution terms after their passing. Use this form if you wish to ensure that your coins are preserved and passed on as you intend.

Who can use this document

- Individuals with a valuable coin collection who want to plan for its future management.

- Anyone looking to create a revocable trust for asset protection and estate planning.

- Collectors who wish to specify how their collection should be divided among heirs.

Steps to complete this form

- Identify the Trustor and provide their contact information at the beginning of the form.

- Name the Trust and specify that it is a Revocable Trust regarding the coin collection.

- List the specific coins included in the collection in Exhibit A.

- Designate a Successor Trustee in case the original Trustee can no longer serve.

- Sign and date the agreement in the presence of a notary public if mandated.

Is notarization required?

This form does not typically require notarization unless specified by local law. However, having it notarized can add an extra layer of security and validation to the trust agreement.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to name a Successor Trustee, which could lead to complications in management.

- Not properly describing the coin collection, which might create ambiguity in distribution.

- Neglecting to have the form notarized when required by state law.

Benefits of completing this form online

- Convenience of downloading and completing the form at your own pace.

- Editability allows for quick updates if the collection changes.

- Access to legal forms drafted by licensed attorneys ensures accuracy and compliance.

Legal use & context

- The Revocable Trust Agreement is a valid legal instrument for managing and distributing assets.

- Assets held in a revocable trust generally avoid probate, facilitating easier transfer to beneficiaries.

- It allows the Trustor to adjust terms as needed during their lifetime, reflecting changing circumstances.

Key takeaways

- The Revocable Trust Agreement allows for effective management and distribution of a coin collection.

- It provides flexibility, enabling the Trustor to amend or revoke the trust during their lifetime.

- Proper completion and adherence to state-specific rules are essential for legal enforceability.

Looking for another form?

Form popularity

FAQ

A Revocable Living Trust Defined Assets can include real estate, valuable possessions, bank accounts and investments. As with all living trusts, you create it during your lifetime.

Houses and other real estate (even if they're mortgaged) stock, bond, and other security accounts held by brokerages (but think about naming a TOD beneficiary instead) small business interests (stock in a closely held corporation, partnership interests, or limited liability company shares)

When Should You Put a Bank Account into a Trust?More specifically, you can hold up to $166,250 of real or personal property outside a trust and avoid full probate in California. However, if you have more than $166,250 in a bank account, you should consider transferring it into your trust.

Paperwork. Setting up a living trust isn't difficult or expensive, but it requires some paperwork. Record Keeping. After a revocable living trust is created, little day-to-day record keeping is required. Transfer Taxes. Difficulty Refinancing Trust Property. No Cutoff of Creditors' Claims.

The process of funding your living trust by transferring your assets to the trustee is an important part of what helps your loved ones avoid probate court in the event of your death or incapacity. Qualified retirement accounts such as 401(k)s, 403(b)s, IRAs, and annuities, should not be put in a living trust.

To transfer assets such as investments, bank accounts, or stock to your real living trust, you will need to contact the institution and complete a form. You will likely need to provide a certificate of trust as well. You may want to keep your personal checking and savings account out of the trust for ease of use.

If you have created a revocable trust and have appointed someone else as trustee, you will have to request the cash withdrawal from the person you appointed as the trustee. However, the trustee has a fiduciary duty to administer the trust for your benefit while you are alive.

The process of funding your living trust by transferring your assets to the trustee is an important part of what helps your loved ones avoid probate court in the event of your death or incapacity. Qualified retirement accounts such as 401(k)s, 403(b)s, IRAs, and annuities, should not be put in a living trust.

Its primary purpose is to avoid probate court, since revocable living trusts do not reduce estate taxes. With a revocable trust, your assets will not be protected from creditors looking to sue.With this kind of trust, assets are more protected from creditors.