Deferred Compensation Agreement - Long Form

Understanding this form

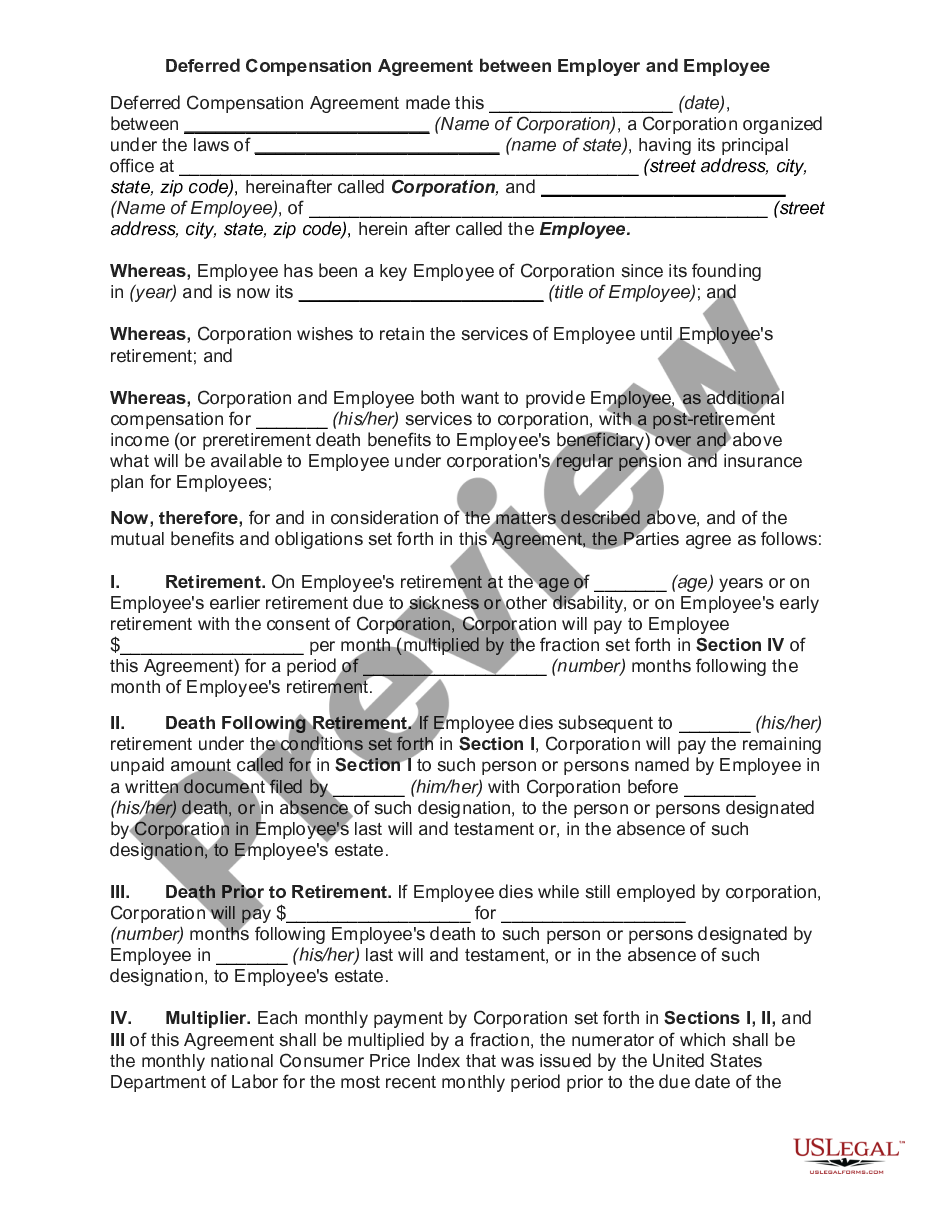

The Deferred Compensation Agreement - Long Form is a legal contract between an employer and an employee (or independent contractor) that sets the terms for compensation to be paid at a future date, typically after retirement or upon termination of employment. This agreement allows for certain income to be deferred, helping employees to manage taxation more effectively. Unlike traditional compensation agreements, this form defines multiple facets of deferred payments, conditions under which payments are made, and obligations of the parties involved.

Form components explained

- Introduction: Identifies the parties (employer and employee) and outlines the intent of the agreement.

- Multiplier Clause: Details how monthly payments will be adjusted according to the National Consumer Price Index.

- Termination Conditions: Specifies circumstances under which the obligation to make payments may cease.

- Noncompetition Clause: Prohibits the employee from engaging with competitive businesses to maintain eligibility for payments.

- Encumbrances: Restricts the ability of the employee to transfer or assign rights to receive deferred payments.

- Severability Clause: Ensures that if one part of the agreement is invalid, the rest remains enforceable.

- Modification Clause: Outlines how changes to the agreement must be made and documented.

When to use this form

This form is commonly used when an employer wishes to provide additional compensation to an employee or contractor that will be disbursed in the future. It is ideal in scenarios where an employee is nearing retirement and seeks to maximize financial benefits while managing tax implications. Additionally, it can be utilized when a business wants to incentivize long-term commitment by retaining key personnel through financial promises established in this agreement.

Intended users of this form

This form is suitable for:

- Employers looking to attract and retain talent through deferred compensation plans.

- Employees or independent contractors seeking to secure future payments after retirement or other employment termination.

- Human resource managers and legal advisors who are involved in structuring compensation packages.

Completing this form step by step

- Identify the parties involved, including full names and titles.

- Clearly define the compensation amount or structure as per the agreement.

- Incorporate the multiplier clause to adjust future payments based on the National Consumer Price Index.

- Specify the conditions under which payments will be terminated.

- Ensure that all parties sign the agreement, indicating acceptance of the terms.

Does this document require notarization?

In most cases, this form does not require notarization. However, some jurisdictions or signing circumstances might. US Legal Forms offers online notarization powered by Notarize, accessible 24/7 for a quick, remote process.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to specify conditions that would terminate the agreement.

- Neglecting to adjust payments according to inflation or the Consumer Price Index.

- Not including signatures from all parties involved, which may invalidate the agreement.

- Ignoring the legal implications of the noncompetition clause.

- Overlooking the need for clear definitions of terms used in the agreement.

Why use this form online

- Convenient access to templates from anywhere with an internet connection.

- Ability to edit and customize terms to fit specific needs easily.

- Secure storage and retrieval of completed documents.

- Compliance with legal standards as forms are drafted by licensed attorneys.

- Quick downloads that save time compared to traditional methods.

Legal use & context

- This agreement serves as a binding contract detailing deferred payment arrangements.

- It is essential to ensure that the obligations set within the agreement are enforceable under relevant laws.

- Employees and employers must consider the tax implications tied to deferred compensation to avoid future legal complications.

Summary of main points

- A Deferred Compensation Agreement allows payments to be made after services have been rendered, often for tax-planning benefits.

- It is important to clearly define terms such as payment amounts, timing, and conditions for termination.

- The agreement must be signed by both parties to ensure its legal enforceability.

Looking for another form?

Form popularity

FAQ

Reeves suggested limiting deferred compensation to no more than 10 percent of overall assets, including other retirement accounts, taxable investments and even emergency cash funds. Typically, employees must choose how much to defer and when they would like to receive the payout.

To set up a NQDC plan, you'll have to: Put the plan in writing: Think of it as a contract with your employee. Be sure to include the deferred amount and when your business will pay it. Decide on the timing: You'll need to choose the events that trigger when your business will pay an employee's deferred income.

Generally speaking, the tax treatment of deferred compensation is simple: Employees pay taxes on the money when they receive it, not necessarily when they earn it.The year you receive your deferred money, you'll be taxed on $200,000 in income10 years' worth of $20,000 deferrals.

What Is Deferred Compensation? Deferred compensation is a portion of an employee's compensation that is set aside to be paid at a later date. In most cases, taxes on this income are deferred until it is paid out. Forms of deferred compensation include retirement plans, pension plans, and stock-option plans.

To enroll, your employer must participate in the plan (employers can visit our Employer Resource Center or call us at (800) 696-3907 to learn more). For more information, visit the CalPERS 457 Plan website, call the Plan Information Line at (800) 260-0659, or view the additional resources below.

Distributions to employees from nonqualified deferred compensation plans are considered wages subject to income tax upon distribution. Since nonqualified distributions are subject to income taxes, these amounts should be included in amounts reported on Form W-2 in Box 1, Wages, Tips, and Other Compensation.

B: Uncollected Medicare tax on tips reported to your employer (but not Additional Medicare Tax) BB: Designated Roth contributions under a section 403(b) plan. C: Taxable cost of group-term life insurance over $50,000. D : Contributions to your 401(k) plan. DD: Cost of employer-sponsored health coverage.

When you defer income, federal income tax is also delayed, but you do pay Social Security and Medicare taxes. A deferred comp plan is most beneficial when you're able to reduce both your present and future tax rates by deferring your income. Unfortunately, it's challenging to project future tax rates.

Box 11 Shows the total amount distributed to you from your employer's non-qualified (taxable) deferred compensation plan. Box 12 Various Form W-2 Codes on Box 12 that reflect different types of compensation or benefits. A Uncollected Social Security or RRTA tax on tips.