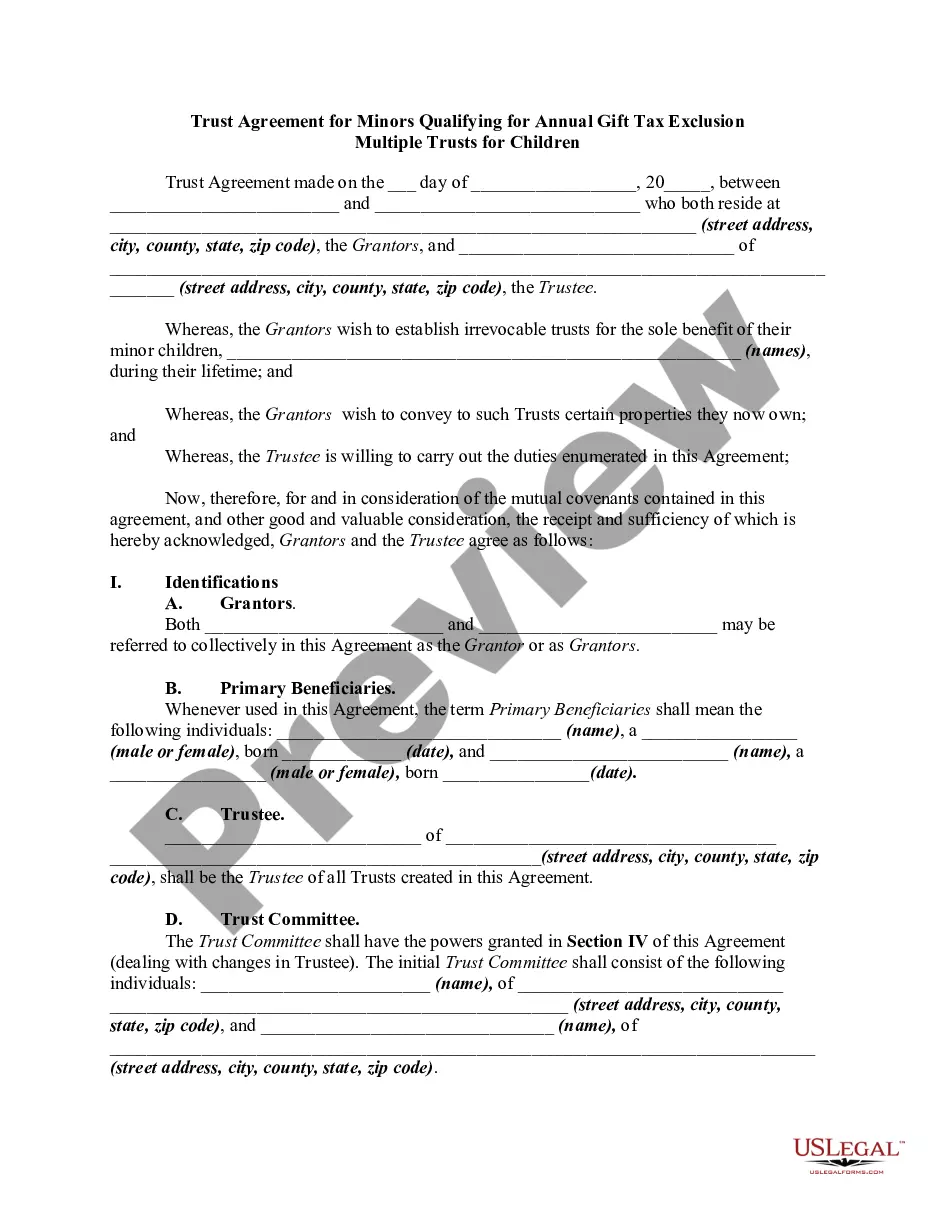

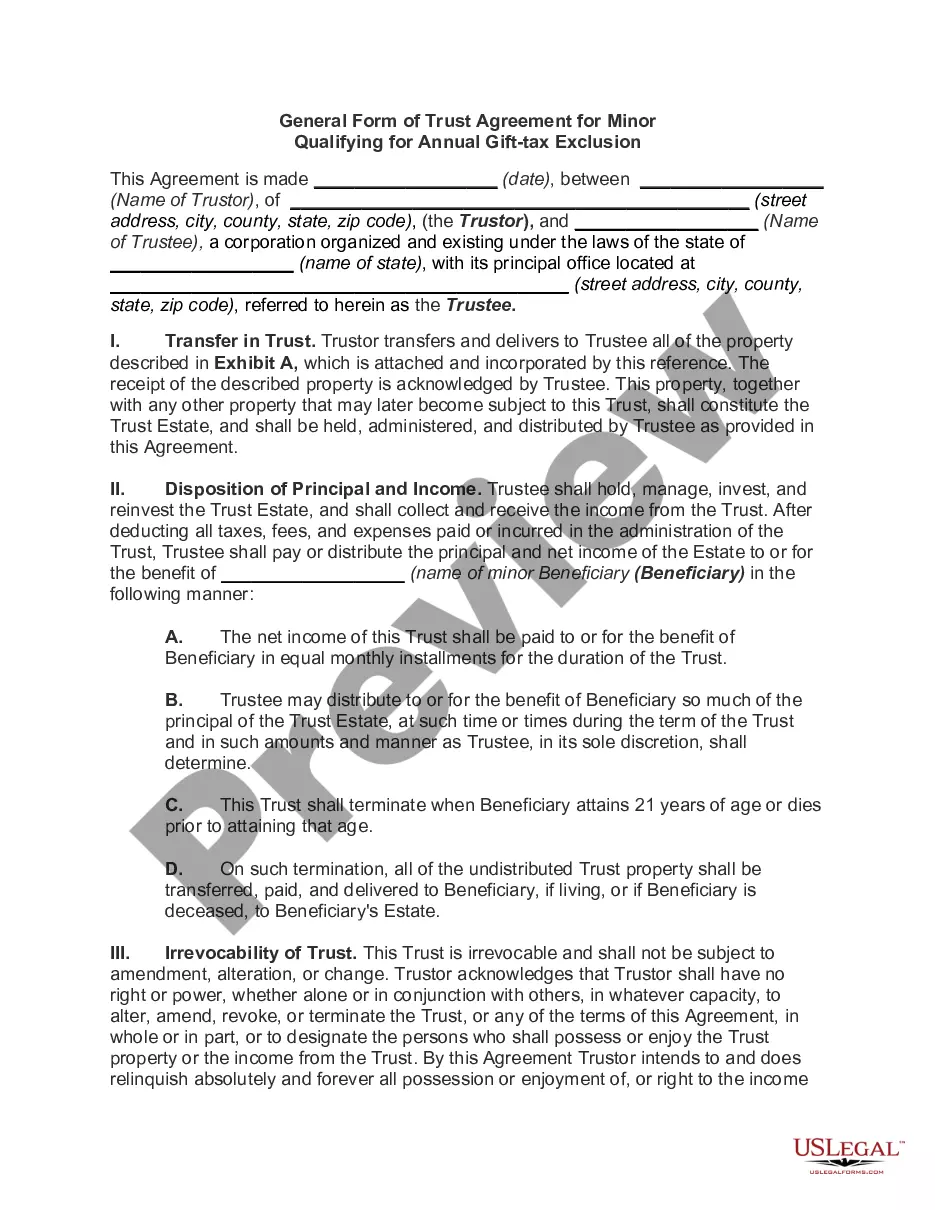

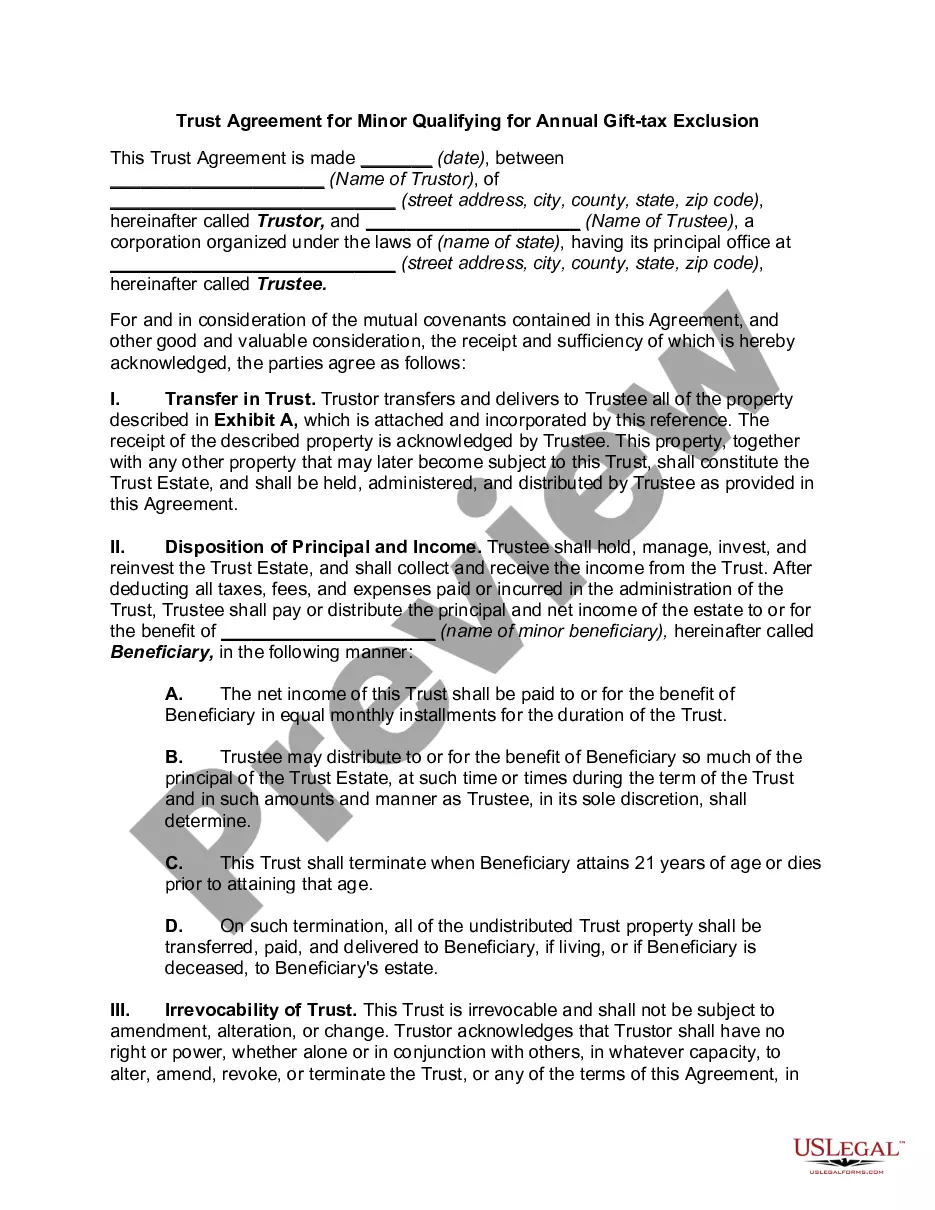

Multiple Trusts for Children -- Trust Agreement for Minor Qualifying for Annual Gift-Tax Exclusion

Understanding this form

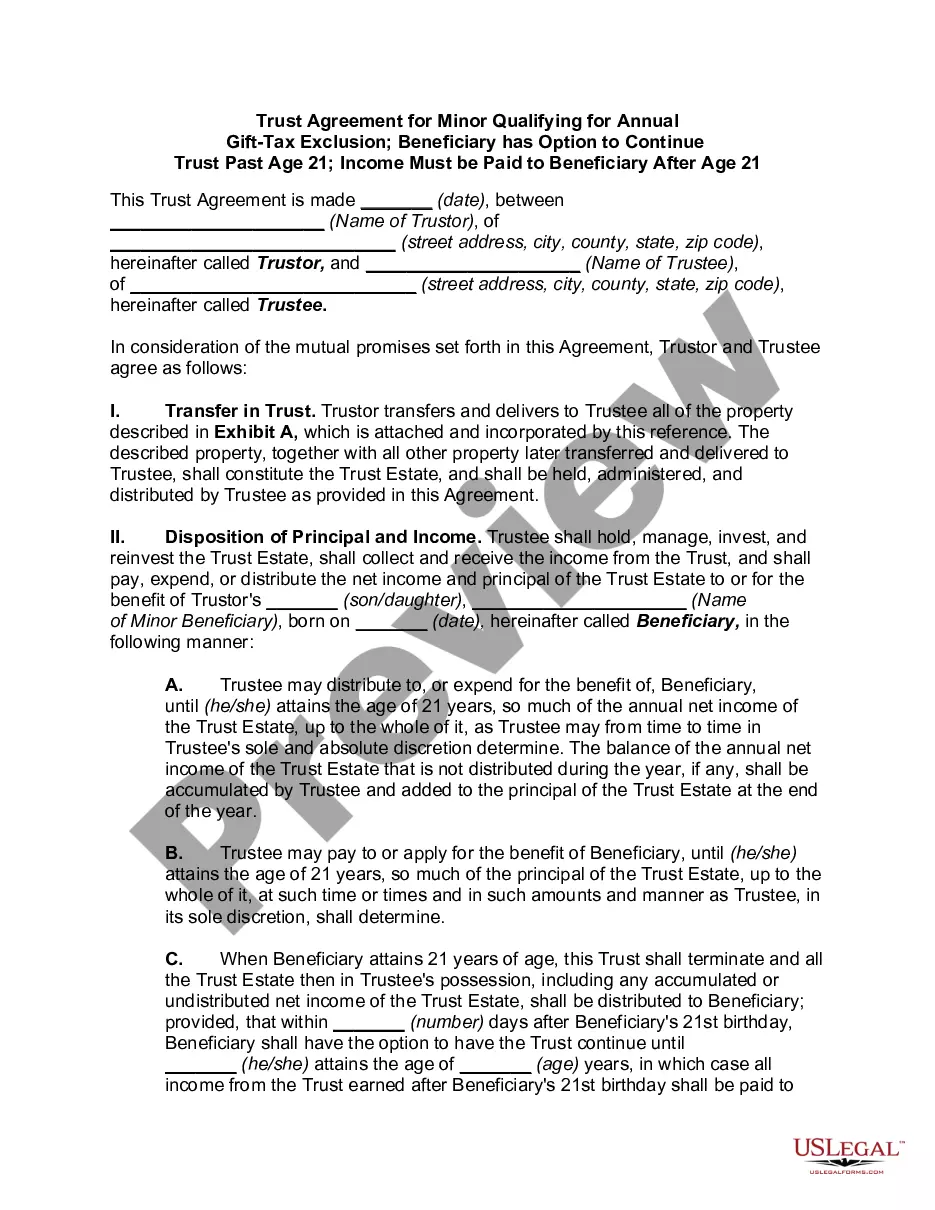

The Multiple Trusts for Children -- Trust Agreement for Minor Qualifying for Annual Gift-Tax Exclusion is a legal document that establishes one or more irrevocable trusts for the benefit of minor children. This trust is designed to facilitate the gifting process while minimizing federal gift, income, and estate taxes. It essentially allows parents or guardians (grantors) to manage and protect the assets meant for their children until they reach adulthood, specifically allowing gifts to qualify for the annual gift tax exclusion under section 2503(c) of the Internal Revenue Code.

Key parts of this document

- Identification of grantors and trustee.

- Establishment of individual trusts for each minor beneficiary.

- Specifications for property disposition and trust management.

- Provisions for income and principal distributions to beneficiaries.

- Trusteeâs powers and responsibilities outlined in detail.

When to use this form

This form is ideal for parents or guardians wanting to set up trusts for their minor children. It is particularly useful when individuals intend to make substantial gifts to their children, ensuring these gifts qualify for annual gift tax exclusions. The trust helps in managing the gifts while safeguarding the financial interests of the children until they are mature enough to handle the assets responsibly.

Who should use this form

- Parents or guardians planning to transfer significant assets to their minor children.

- Individuals looking to take advantage of the annual gift tax exclusion.

- Anyone who wishes to ensure proper management of a child's financial inheritance until reaching adulthood.

Instructions for completing this form

- Identify the parties involved: enter the names of the grantors and the trustee.

- Specify the minor beneficiaries for whom the trusts are being established.

- List the properties or assets being transferred into the trust.

- Complete sections detailing how the trust assets will be managed and distributed.

- Sign and date the agreement in the presence of a valid witness if required.

Does this document require notarization?

This form does not typically require notarization unless specified by local law. However, it is recommended to check for any specific state regulations that may apply.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to clearly identify all beneficiaries, which can lead to disputes later.

- Not specifying the assets being placed into the trust properly.

- Overlooking state-specific requirements that may affect the trustâs validity.

- Neglecting to update the trust as circumstances change, such as the birth of additional children.

Advantages of online completion

- Accessible documents that can be downloaded and filled out at your convenience.

- Reliable templates drafted by licensed attorneys to ensure legal compliance.

- Easy customization options to fit your specific requirements.

- Immediate access to your forms without needing to visit a legal office.

Key takeaways

- The Multiple Trusts for Children form protects minor beneficiaries by managing trust assets until they reach adulthood.

- It allows gifts to qualify for annual gift tax exclusions, providing financial benefits for families.

- Properly establishing trusts can minimize future tax liabilities while ensuring responsible asset management.

Looking for another form?

Form popularity

FAQ

Gift Splitting Example Once again, let's assume that you and your spouse want to gift each of your three children money. The funds will go into three different college savings accounts, one for each of them. Under the gift-splitting rule, you can contribute up to $34,000 to each account together.

Each individual is responsible to file a Form 709. You must file a gift tax return to split gifts with your spouse (regardless of their amount) as described in Part 1?General Information, later.

Definition and Examples of Gift Splitting The gift-splitting rule allows a married couple who files a joint return to double their annual gift-tax exclusion limit. So that means couples can split gifts of up to $32,000 in 2022 without having to pay gift tax on them, under current limits.

To consent to split gifts, the donor must complete and file a federal gift tax return (Form 709), which the non-donor spouse must also sign, providing their consent to split gifts for the calendar year applicable to the gift tax return.

Gifts in trust are commonly used to pass wealth from one generation to another by establishing a trust fund. Typically, the IRS taxes the value of a gift being transferred up to the annual gift tax exclusion amount. A gift in trust is a way to avoid taxes on gifts that exceed the annual gift tax exclusion amount.

Is There Tax on Gifts to Children? Gifts made to children may be subject to tax, but typically only if they are large gifts. As of 2022, any gift under $16,000 isn't typically subject to gift tax and doesn't need to be reported to the IRS. This is due to the annual gift tax exclusion.

Exclusions and credits Gift splitting is not permitted if either spouse is a non-US domiciliary. An unlimited amount can be gifted to a spouse who is a US citizen, whereas gifts to a non-US citizen spouse are offset by an increased annual exclusion.

The term gift splitting refers to an estate planning tool that married couples can use to double their allowed annual gift tax exclusion amount. The gift tax exclusion is the amount that someone can transfer to another person as a gift without having to pay the gift tax levied by the Internal Revenue Service (IRS).