Trust Agreement for Minor Qualifying for Annual Gift-Tax Exclusion; Beneficiary has Option to Continue Trust Past Age 21; Income Must be Paid to Beneficiary After Age 21

What this document covers

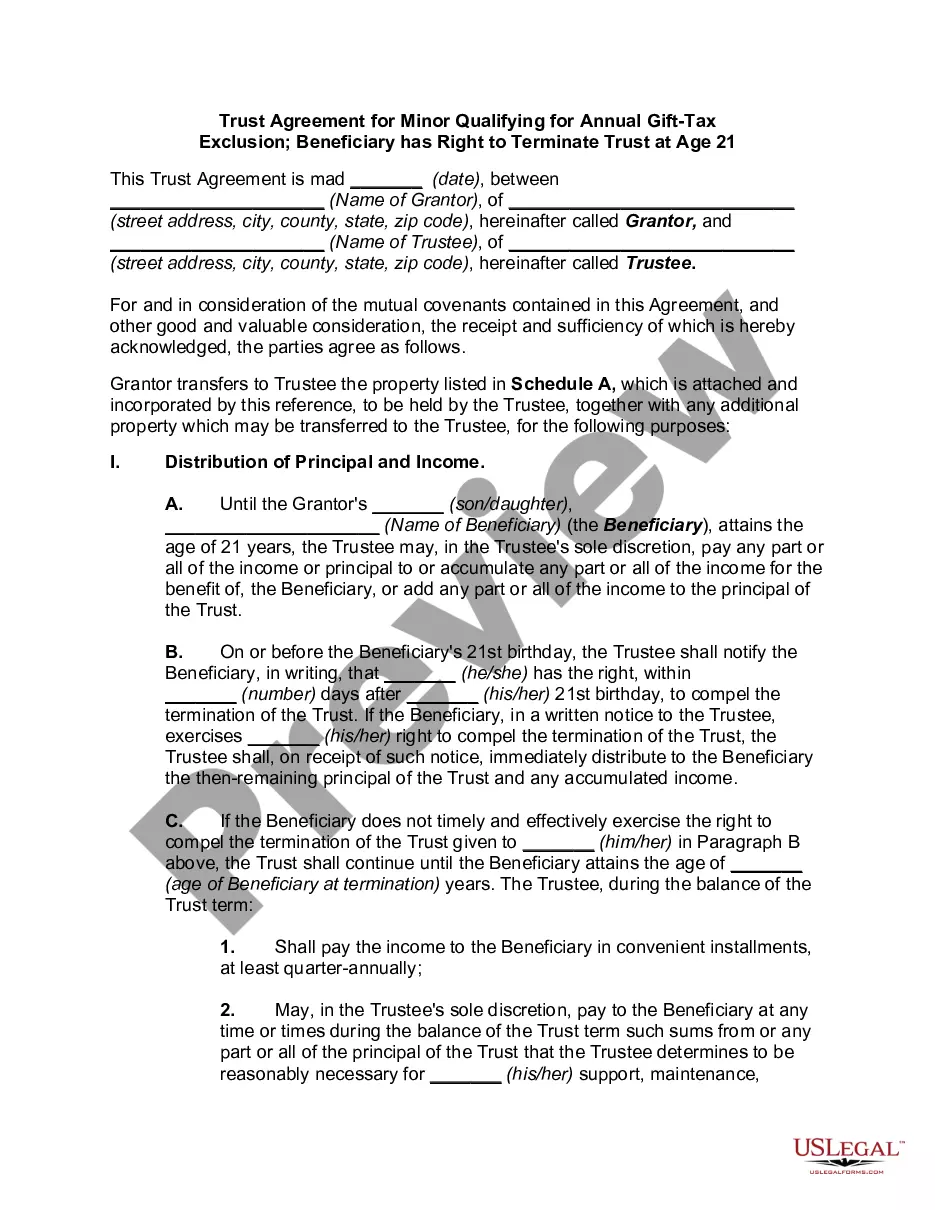

The Trust Agreement for a Minor qualifying for the Annual Gift-Tax Exclusion is a legal document designed to create a trust for a child under the age of 21. This trust allows gifts made to a minor to qualify for annual gift tax exclusions while ensuring proper management of the assets until the child reaches maturity. Unlike other trust agreements, this form provides a structured approach for managing the trustâs income and principal, offering the minor access to the funds at age 21, while also allowing the option to extend the trust.

Main sections of this form

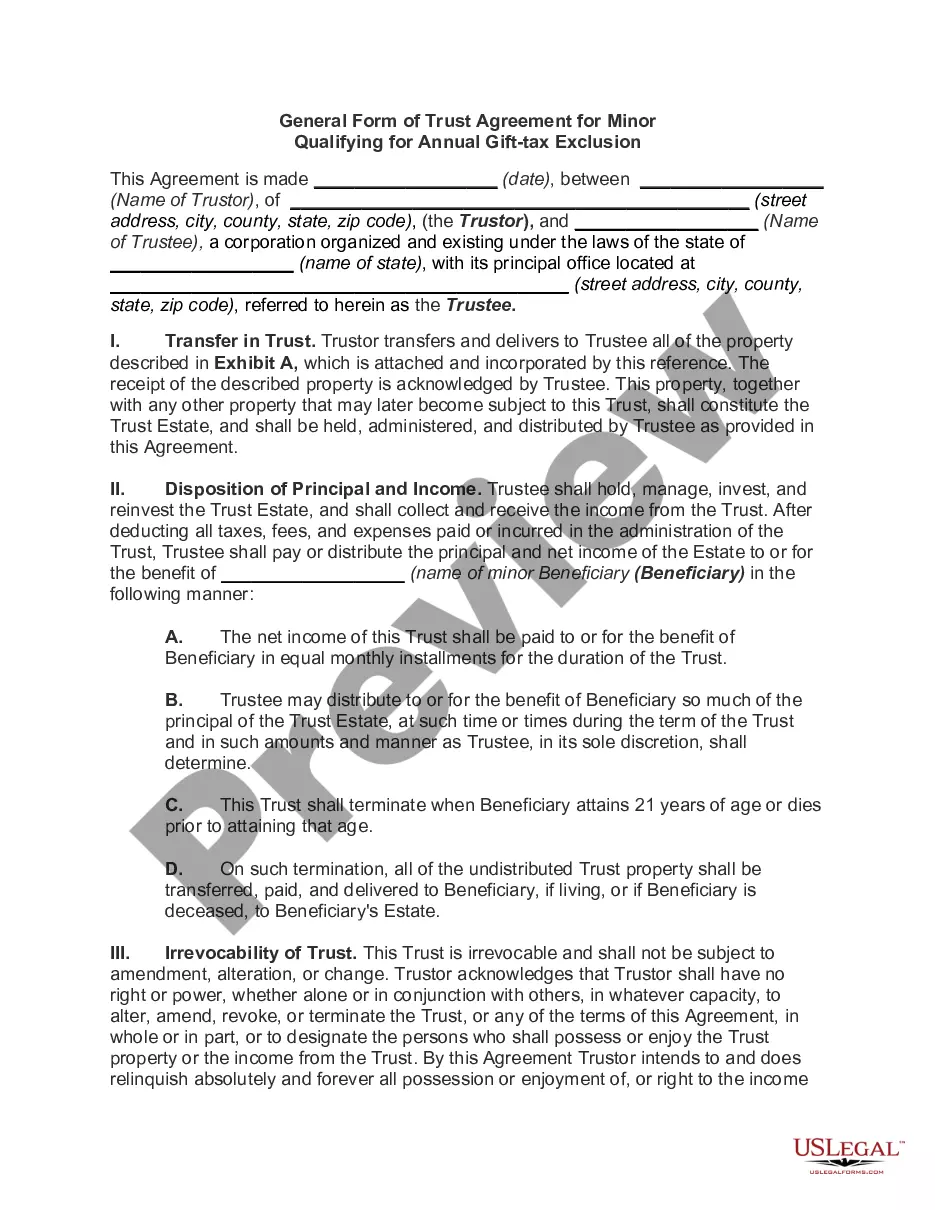

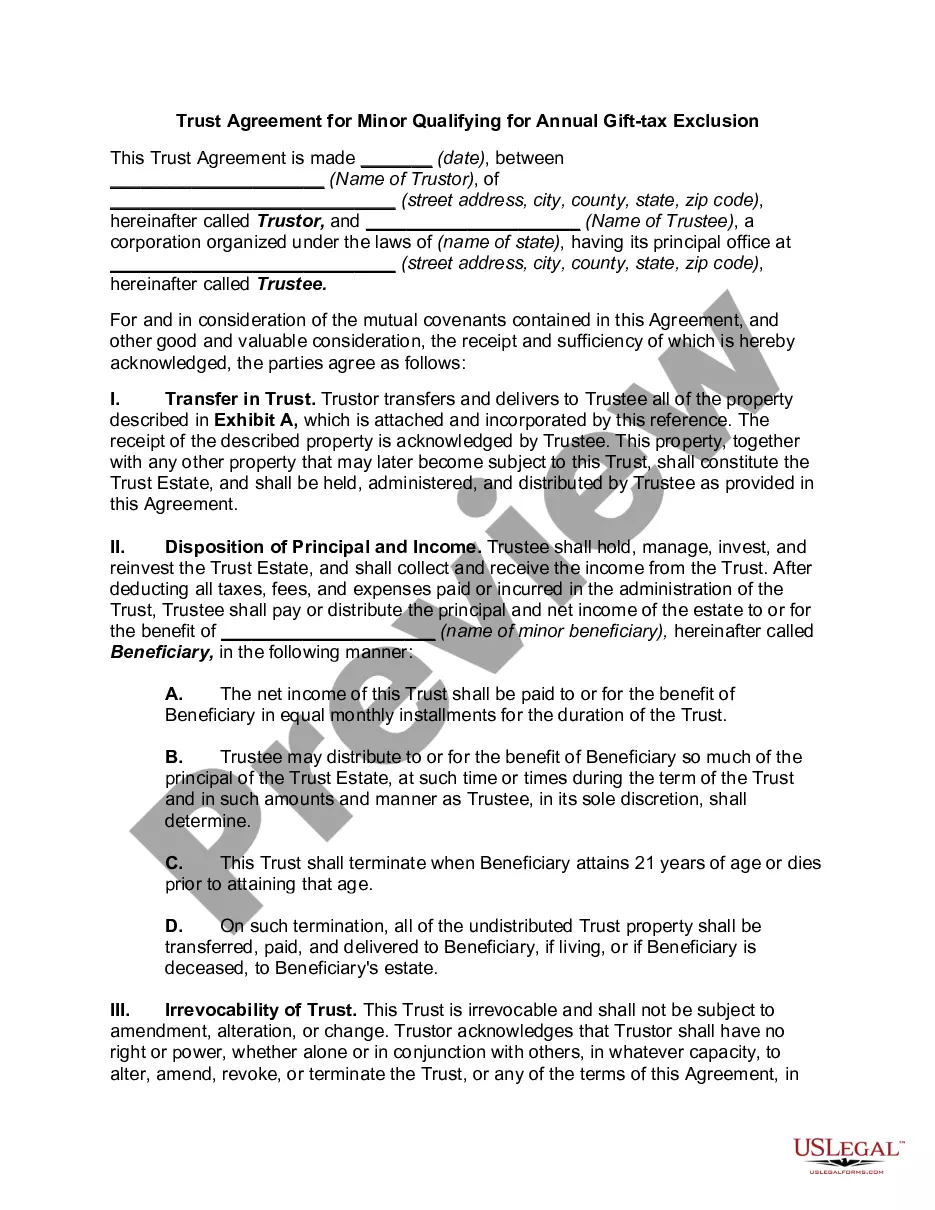

- Identification of the Trustor and Trustee, including addresses and names.

- Transfer of property into the trust, detailed in an attached exhibit.

- Disposition of trust income and principal during the minor's childhood and upon reaching age 21.

- Provisions for trustee powers, limitations, and succession.

- Spendthrift provisions to protect the trust assets from the beneficiary's debts.

- Accountability requirements for the Trustee's management of the trust estate.

When to use this form

This Trust Agreement should be used when a trustor wishes to make gifts to a minor and wants to ensure these gifts are managed wisely until the child reaches age 21. It is particularly useful for parents or guardians looking to minimize tax implications while preparing for the future financial needs of their child. Situations may include setting up funds for education, health expenses, or providing a financial safety net.

Intended users of this form

- Parents or guardians wishing to create a financial trust for their minor child.

- Individuals looking to make significant gifts to minors while qualifying for tax exclusions.

- Trustors wanting to ensure responsible management of junior family members' wealth.

- Persons seeking to plan for future financial stability for minors through structured trusts.

How to complete this form

- Identify and enter the names and addresses of the Trustor and Trustee.

- Detail the property being transferred into the trust in the attached Exhibit A.

- Specify the distribution terms for the trust income and principal to the minor.

- Complete the succession details for any successor trustees, if applicable.

- Have both the Trustor and Trustee sign and date the agreement, ensuring accurate witness acknowledgment.

Does this document require notarization?

This form does not typically require notarization unless specified by local law. It is advisable to check jurisdiction-specific requirements to ensure compliance and validity.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to accurately identify the Trustor or Trustee's information.

- Not including all necessary property in the trust.

- Overlooking specific state laws that may require additional details or forms.

- Neglecting to properly notarize the document where required.

Why use this form online

- Convenience of downloading and customizing the template at your own pace.

- Reliability of having forms reviewed by licensed attorneys.

- Access to legal forms anytime and anywhere with an Internet connection.

Legal use & context

- The trust is established to provide financial management for minor beneficiaries.

- The agreement outlines responsibilities and rights of the Trustee, ensuring proper asset management.

- Utilizing this form can minimize potential tax liabilities associated with gifted assets for the Trustor.

Main things to remember

- This Trust Agreement supports financial planning for minors while allowing tax benefits.

- It includes specific provisions for managing trust income and principal.

- Proper completion and understanding of this form can enhance the financial future of a minor beneficiary.

Looking for another form?

Form popularity

FAQ

A 2503(c) trust, or minor's trust, is a trust established to hold gifts for one child until he or she attains age 21. A gift to this type of trust qualifies for the annual federal gift tax exclusion.

The trust vs. mistrust stage is the first stage of psychologist Erik Erikson's theory of psychosocial development. This stage begins at birth and lasts until a child is around 18 months old.

If you gift more than the exclusion to a recipient, you will need to file tax forms to disclose those gifts to the IRS. You may also have to pay taxes on it. If that's the case, the tax rates range from 18% up to 40%. However, you won't have to pay any taxes as long as you haven't hit the lifetime gift tax exemption.

What is the 21-year rule? Family trusts created during someone's lifetime are deemed to dispose of their property every 21 years. Although the trust is deemed to have disposed of property for tax purposes, an actual disposition typically does not occur.

Trust can provide financial support for minors, and they provide more flexibility than other means of financial support, such as under the Uniform Transfers to Minors Act ( UTMA ), or the older, more restrictive Uniform Gifts to Minors Act ( UGMA ).

Once the child reaches a specified age set by the state, the child will have full control over the property. Gifts to the minor are exempted up to $15,000 a year from Federal taxes, but the minor will be required to pay taxes beyond this amount.

Do gifts to a Gift Trust qualify for the annual exclusion? As previously mentioned, to qualify for the annual exclusion, a gift must be a gift of a ?present interest,? which simply means that the recipient must either receive or have the right to receive the gifted property at the time of the gift.

There are several types of minor trusts, including special needs trusts, education trusts, and children's accounts. Read on to learn more about the different types of minor trusts and how they work.