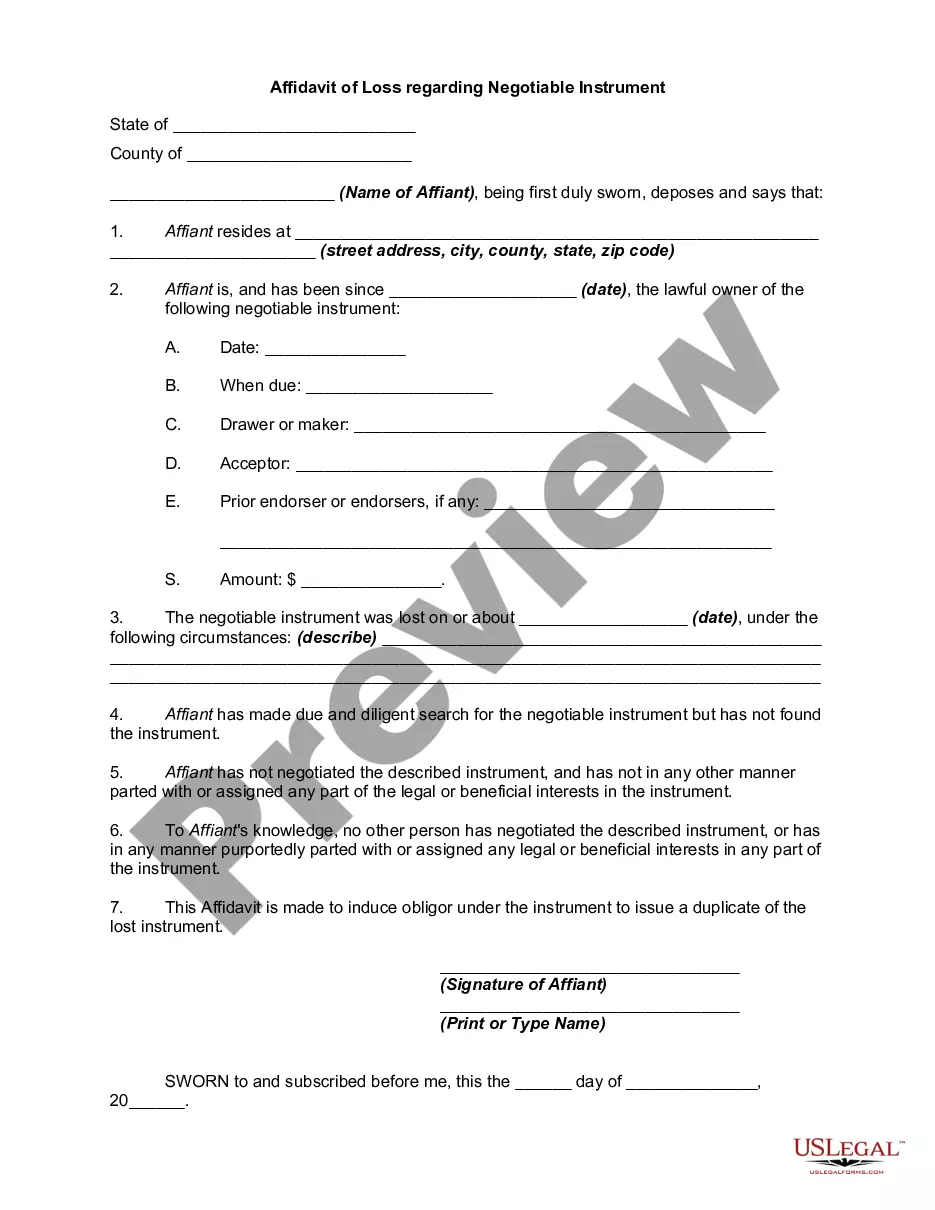

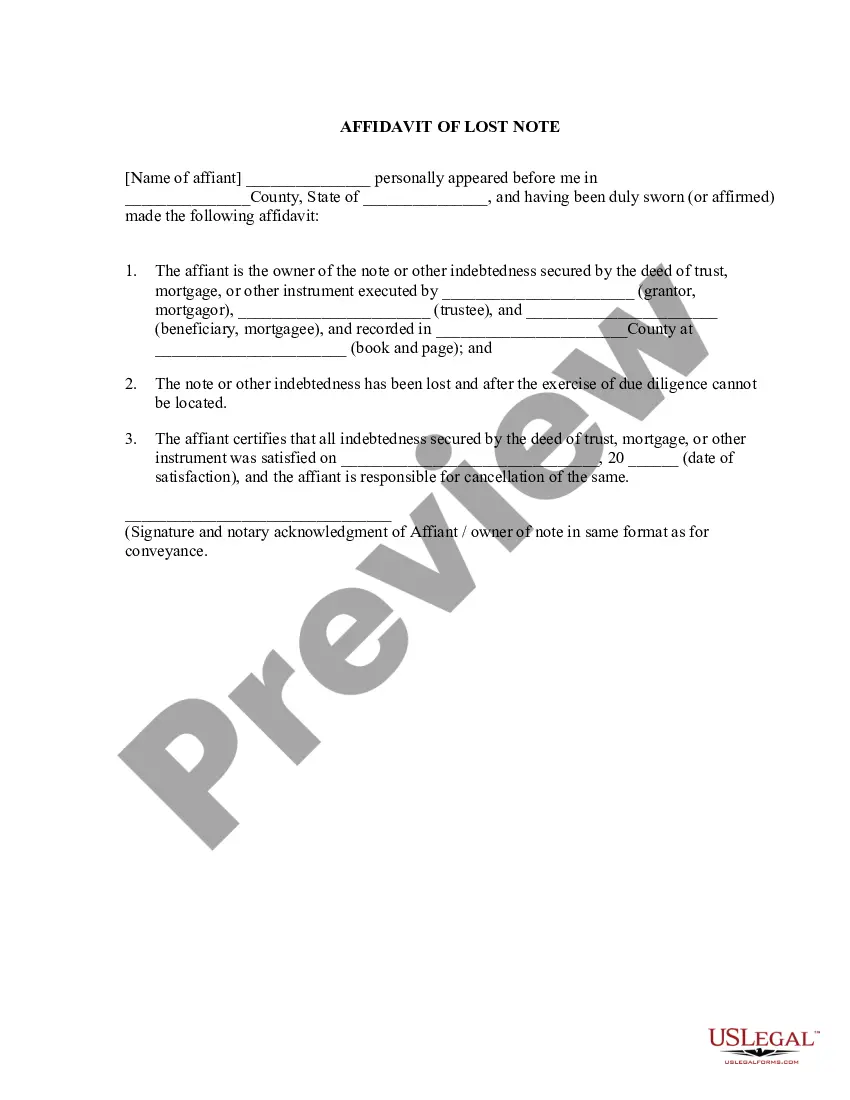

Affidavit of Lost Promissory Note

What this document covers

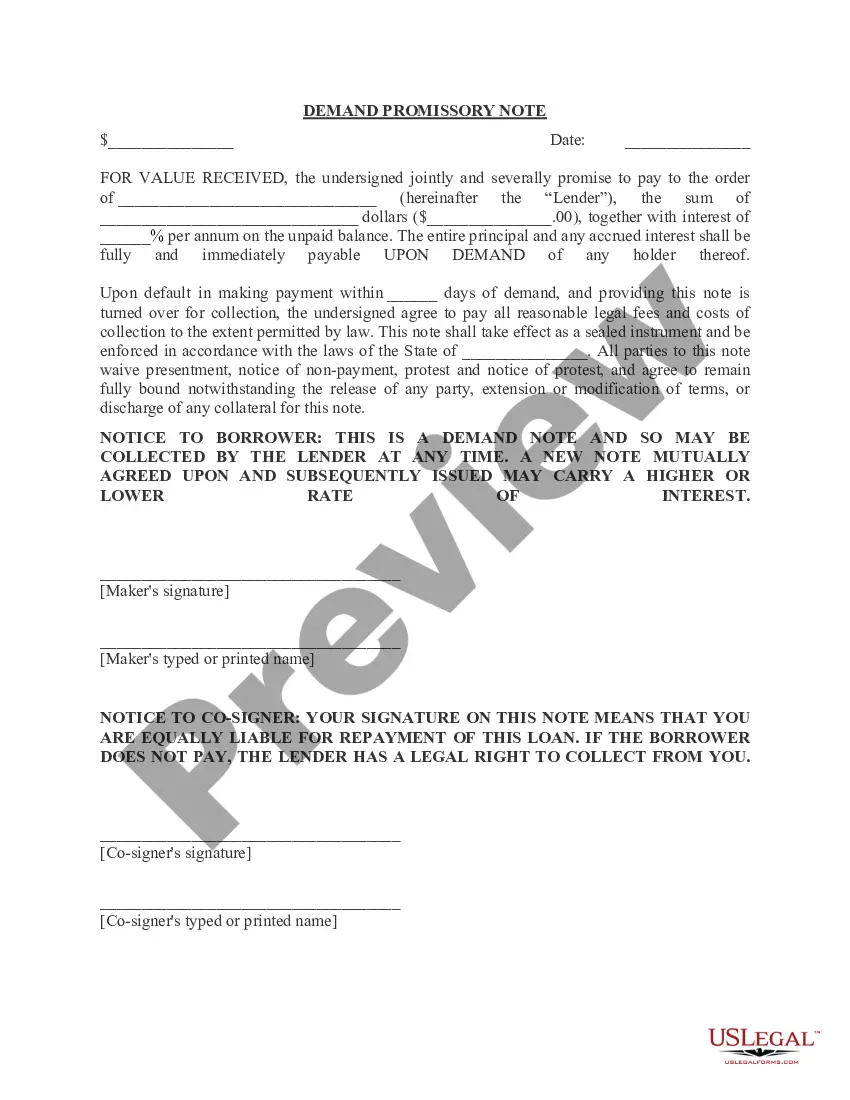

The Affidavit of Lost Promissory Note is a legal document executed when the original promissory note has been lost. This affidavit affirms the details of the original note, including the amount owed and the payment terms, ensuring clarity and legal standing in the absence of the original document. This form distinguishes itself from other affidavits by focusing specifically on lost promissory notes, which are critical in resolving any disputes regarding the ownership and payment obligations associated with the note.

Key components of this form

- The Affiant's name and capacity (e.g., lender, beneficiary).

- Detailed description of the lost promissory note, including its date, amount, and interest rate.

- The name of the debtor(s) responsible for the note.

- Verification of details related to the lost note and indemnification clause.

- The current balance due on the note, specifying principal and interest amounts.

- Signature of the Affiant and acknowledgment by a notary public.

Situations where this form applies

This form is necessary when the original promissory note is lost, and the holder needs to establish the terms of the loan. Use this affidavit if you need to prevent double payment or collection and to clarify the rights associated with your claim to the funds specified in the original note. It is also essential in circumstances where the lender may need to pursue legal action or when refinancing the loan requires proof of the original loan terms.

Who can use this document

- Individuals or entities who have lost a promissory note.

- Lenders seeking to formalize their claim after the loss of a note.

- Debtors needing proof of repayment terms to resolve disputes.

- Legal representatives handling cases involving lost financial documents.

How to complete this form

- Identify and enter the names and details of the Affiant and the debtor(s).

- Specify the original note's date, amount, interest rate, and payment schedule.

- Indicate where the original note was recorded and provide reference details.

- Enter the current balance due, specifying both principal and interest.

- Sign the form in the presence of a notary public, who will acknowledge your signature.

Does this document require notarization?

This document requires notarization to meet legal standards. US Legal Forms provides secure online notarization powered by Notarize, allowing you to complete the process through a verified video call, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to include all required details about the original promissory note.

- Not having the form signed and notarized properly, which can invalidate the affidavit.

- Incorrectly stating the balance due on the note.

- Omitting the statement of indemnification, which protects against double collection.

Benefits of completing this form online

- Convenient download and immediate access to essential legal documents.

- Editability to tailor the affidavit to your specific situation.

- Reliability of our legal form templates, drafted by licensed attorneys.

Main things to remember

- The Affidavit of Lost Promissory Note is essential for legal protection when the original note is missing.

- Accurate completion and notarization are vital for the affidavit's validity.

- This form helps clarify repayment obligations and protect against fraudulent claims.

Looking for another form?

Form popularity

FAQ

Before a promissory note can be canceled, the lender must agree to the terms of canceling it. A well-drafted and detailed promissory note can help the parties involved avoid future disputes, misunderstandings, and confusion. When canceling the promissory note, the process is referred to as a release of the note.

Promissory notes are a valuable legal tool that any individual can use to legally bind another individual to an agreement for purchasing goods or borrowing money. A well-executed promissory note has the full effect of law behind it and is legally binding on both parties.

The lender can provide copies of the documents signed at closing. If the loan has changed hands, contact the most current servicer for a copy of your mortgage or deed of trust documents. A lender is required under the Federal Servicer Act to provide you copies of your loan documents if you submit a written request.

The buyer of the note becomes what is called a holder because they hold your note as the owner of it. A holder has a special right to collect from you right away if you don't pay. But only the holder of an original promissory note can collect from you. A promissory note can change many hands as it is bought and sold.

What Happens When a Promissory Note Is Not Paid? Promissory notes are legally binding documents. Someone who fails to repay a loan detailed in a promissory note can lose an asset that secures the loan, such as a home, or face other actions.

Unlike a mortgage or deed of trust, the promissory note isn't recorded in the county land records. The lender holds the promissory note while the loan is outstanding. When the loan is paid off, the note is marked as "paid in full" and returned to the borrower.

A promissory note, in simplest terms, is the acknowledgment of a debt.Even if a promissory note is lost, the legal obligation to repay the loan remains. The lender has a right to re-establish the note legally as long as it has not sold or transferred the note to another party.

Search the county recorder's records. Promissory notes are typically recorded as public documents and accessible shortly after the closing. The trustee maintains the original deed until the loan is satisfied.