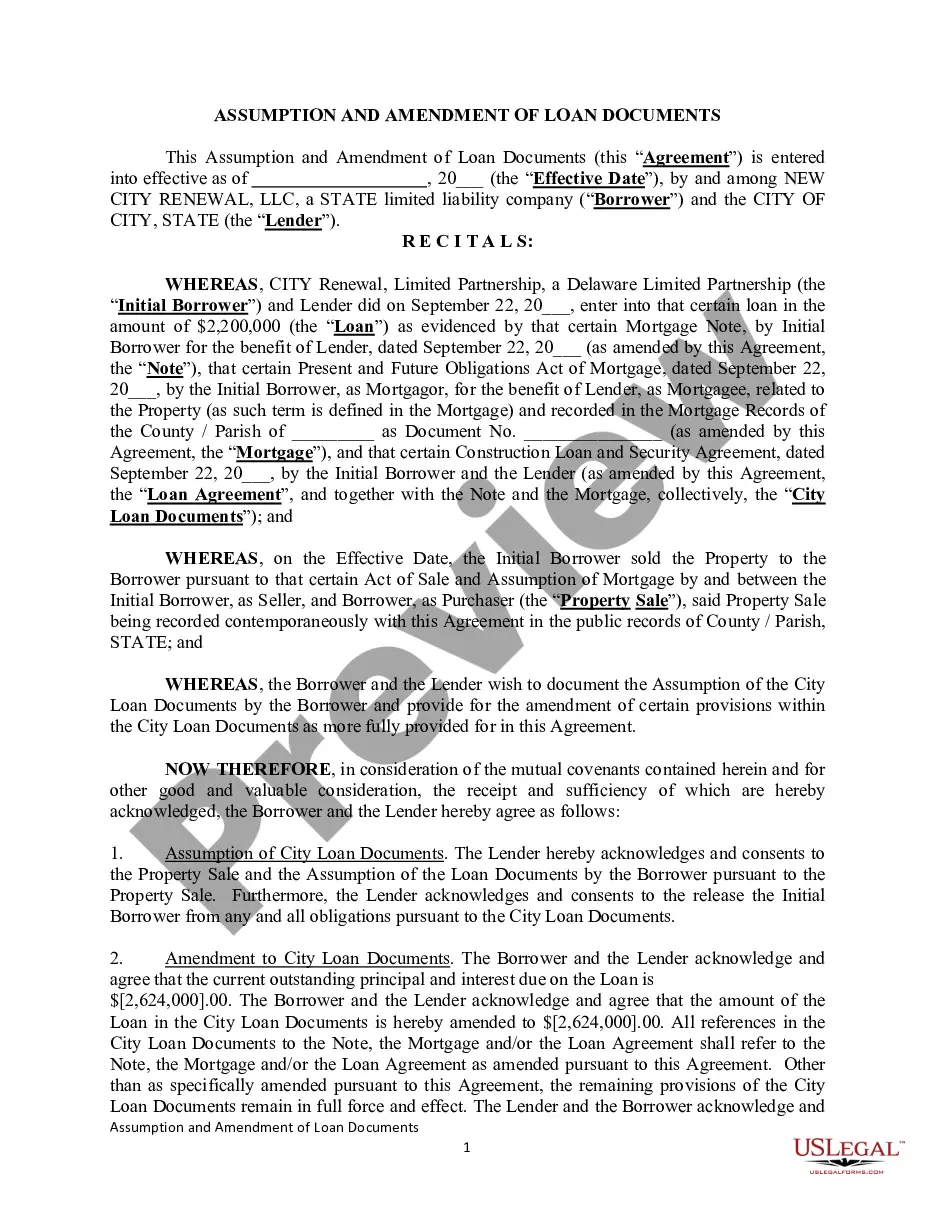

Assumption Agreement of Loan Payments

About this form

The Assumption Agreement of Loan Payments is a legal document that outlines an arrangement where a buyer (Grantee) takes over the responsibility of a loan from the seller (Grantor). This agreement specifies the terms under which the Grantee assumes a lien on the property, making it distinct from other types of loan agreements. Through this agreement, the Grantee agrees to handle the debt payments secured by the property, providing clarity about who is liable for the loan going forward.

Key components of this form

- The date of the agreement and identification of the parties (Grantee and Grantor).

- Description of the property subject to the lien.

- Details regarding the existing loan, including the amount and payment terms.

- The Grantee's agreement to assume the loan and indemnify the Grantor.

- Conditions related to lender approval, if applicable.

- Notarization section for authenticity.

When this form is needed

This form is used when a property owner wishes to transfer ownership of real estate to another person who will also assume the mortgage or loan repayment responsibilities. It is commonly utilized in real estate transactions where the buyer agrees to take over the existing financing terms instead of obtaining a new loan. Situations such as family transfers or financial restructurings may also require this form.

Who this form is for

This form is suitable for:

- Property owners looking to transfer their property while conveying the existing loan.

- Buyers interested in acquiring real estate and assuming the loan attached to it.

- Individuals involved in family property transfers where debt assumption is necessary.

- Real estate professionals who facilitate transactions involving existing loans.

How to prepare this document

- Identify the parties involved as the Grantor and Grantee.

- Specify the property being transferred, including location details.

- Detail the existing loan amount and monthly payment obligations.

- Indicate whether the lender's consent is needed for this assumption.

- Sign the form in the presence of a notary public to validate the agreement.

Notarization requirements for this form

Yes, this form must be notarized to be legally valid. The notarization process confirms the identities of the signatories and ensures that the agreement is executed authentically. US Legal Forms offers an integrated online notarization service that is available 24/7, providing a secure way to notarize documents through a video call, ensuring no need for travel.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to provide complete information about the loan terms.

- Not obtaining the required lender consent when applicable.

- Leaving sections blank that should be filled out, such as property description.

- Neglecting to notarize the agreement where required.

Why complete this form online

- Convenient access and immediate downloads without needing to visit an attorney's office.

- Editability allows users to personalize the agreement according to specific terms.

- Reliability of documents created by licensed legal professionals ensures compliance with legal standards.

Looking for another form?

Form popularity

FAQ

1) Find Out If the Loan is Assumable You can check the loan documents to see whether assumptions are permitted. The loan document will typically state whether or not the loan is assumable under the "assumption clause." The terms may also appear under the "due on sale clause" if loan assumption isn't permitted.

A fee that the buyer of a property with an assumable mortgage pays to the lender for the ability to take over the mortgage.

Cost. This is determined by the loan program and (in some cases) where the property's located. The average assumption fees range from $562 to $1,062. Additional 3rd party fees may apply.

An assumable mortgage allows a buyer to take over the seller's mortgage. Once the assumption is complete, you take over the payments on a monthly basis, and the person you assume the loan from is released from further liability. If you assume someone's mortgage, you're agreeing to take on their debt.

An assumable mortgage allows a buyer to take over the seller's mortgage. Once the assumption is complete, you take over the payments on a monthly basis, and the person you assume the loan from is released from further liability. If you assume someone's mortgage, you're agreeing to take on their debt.

The seller may also be required to sign the assumption agreement and the terms may release the seller from responsibility. The lender usually requires a credit history from the buyer before approving the assumption and the payment of assumption fee(s).

The primary borrower and all co-borrowers sign the mortgage or trust deed. State law dictates whether a mortgage or a trust deed is recorded, but some states permit either document to be used, says Private Money Lending.

Keep in mind that the average loan assumption takes anywhere from 45-90 days to complete. The more issues there are with underwriting, the longer you'll have to wait to finalize your agreement.