Debt Agreement

What is this form?

The Debt Agreement is a legal document that outlines the terms of a loan between two parties. It serves to protect both the borrower and lender by clearly specifying the amount borrowed, repayment terms, and any interest or fees applicable. This form differs from a simple promissory note by including detailed provisions regarding repayment schedules, default conditions, and potential remedies if the borrower fails to fulfill their obligations.

Key components of this form

- Identification of the parties involved in the loan

- Loan amount and currency

- Repayment terms, including due dates and installment amounts

- Interest rate and any additional fees

- Conditions for default and remedies available to the lender

- Signatures of both parties to affirm agreement

When to use this document

This Debt Agreement should be used whenever a loan is made between two parties, whether for personal or business purposes. It is particularly useful when the lender wishes to formalize the terms of the loan to avoid potential disputes. This form can also be helpful in circumstances where the lender wants to ensure full legal recourse in case of non-payment or default.

Who this form is for

This Debt Agreement is ideal for:

- Individuals lending money to friends or family

- Small business owners providing loans to clients or partners

- Investors seeking formal terms in monetary transactions

- Anyone needing a clear and enforceable agreement regarding repayment obligations

Instructions for completing this form

- Identify the parties involved by entering their full names and addresses.

- Clearly state the loan amount and the currency in which it is provided.

- Specify the repayment schedule, including due dates and payment amounts.

- Enter the agreed-upon interest rate and any additional fees.

- Review the conditions for default and remedies, ensuring they are clearly outlined.

- Both parties should sign and date the agreement to finalize it.

Notarization guidance

In most cases, this form does not require notarization. However, some jurisdictions or signing circumstances might. US Legal Forms offers online notarization powered by Notarize, accessible 24/7 for a quick, remote process.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to specify payment dates or amounts clearly.

- Not including interest rates or fees, leading to confusion later.

- Neglecting to have both parties sign and date the document.

- Overlooking local law requirements for loan agreements.

Benefits of using this form online

- Convenience of instant access to downloadable templates.

- Editability allows for customization to fit specific arrangements.

- Reliability from forms drafted by licensed professionals.

Key takeaways

- A debt agreement is crucial for documenting loan terms between parties.

- Clear identification of the parties and terms helps avoid future disputes.

- Having this form signed solidifies the legal standing of the agreement.

Looking for another form?

Form popularity

FAQ

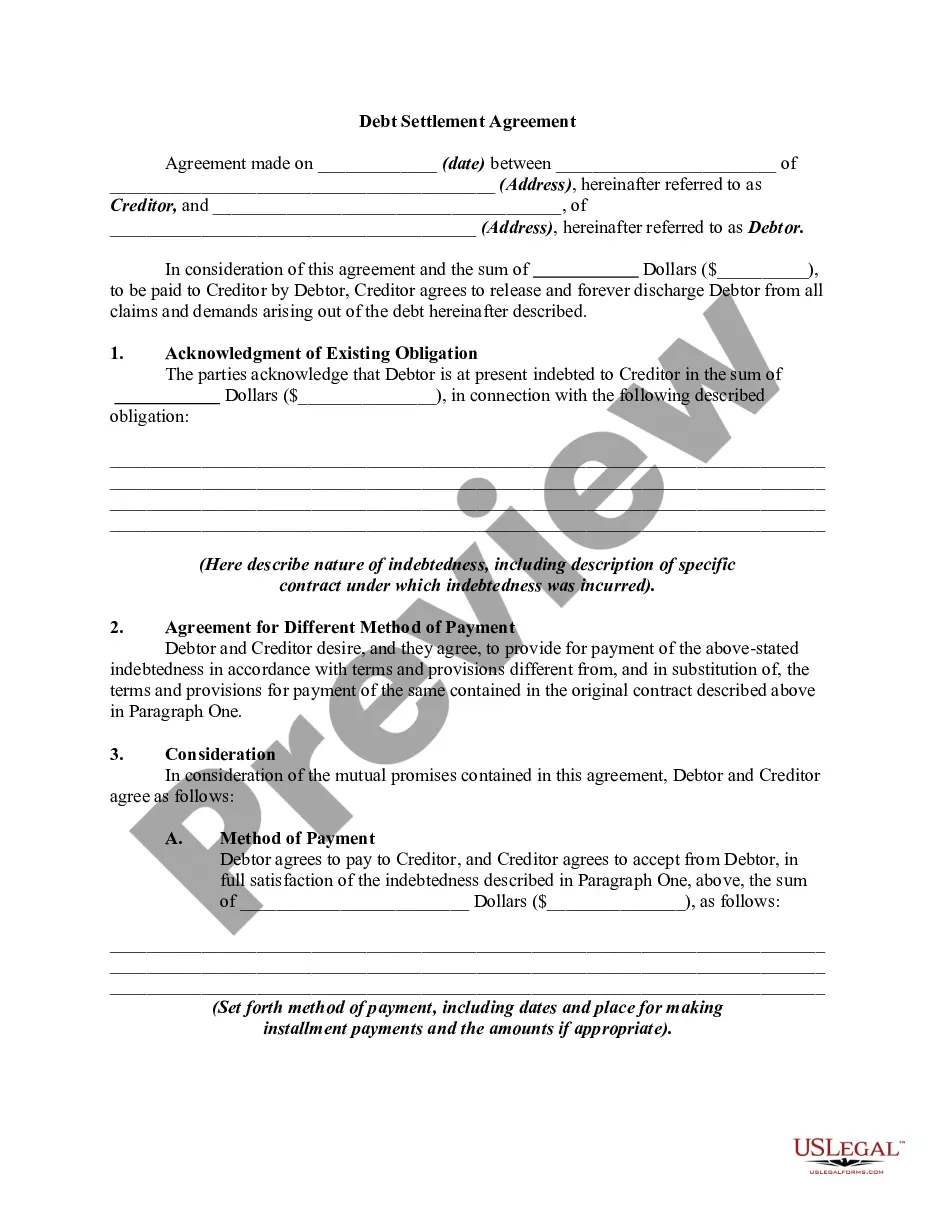

The creditor and/or debt collectors name. The date the letter was drafted. Your name. Your account number.

Your debt settlement proposal letter must be formal and clearly state your intentions, as well as what you expect from your creditors. You should also include all the key information your creditor will need to locate your account on their system, which includes: Your full name used on the account. Your full address.

Your debt settlement proposal letter must be formal and clearly state your intentions, as well as what you expect from your creditors. You should also include all the key information your creditor will need to locate your account on their system, which includes: Your full name used on the account. Your full address.

Offer a specific dollar amount that is roughly 30% of your outstanding account balance. The lender will probably counter with a higher percentage or dollar amount. If anything above 50% is suggested, consider trying to settle with a different creditor or simply put the money in savings to help pay future monthly bills.

Original creditor and collection agent's company name. Date the letter was written. Your name. Your account number. Outstanding balance owed on the account (optional) Amount agreed to as settlement. Terms and amounts of payments to be made (if not a lump-sum)

When writing a debt settlement letter, it's important to be explicit and detailed. Treat the letter as a contract between you and your creditor. Include your personal information and account number for easy identification. You'll need to outline the amount you can pay and what you expect in return.

Verify that it's your debt. Understand your rights. Consider the kind of debt you owe. Consider hardship programs. Offer a lump sum. Mention bankruptcy. Speak calmly and logically. Be mindful of the statute of limitations.

Offer a specific dollar amount that is roughly 30% of your outstanding account balance. The lender will probably counter with a higher percentage or dollar amount. If anything above 50% is suggested, consider trying to settle with a different creditor or simply put the money in savings to help pay future monthly bills.