Loan Commitment Agreement

Understanding this form

A loan commitment agreement is a formal document between a lender and a borrower that outlines the specific terms and conditions under which a loan will be granted. It serves as a promise from the lender to provide financing to the borrower, detailing essential elements like loan amount, interest rate, repayment schedule, and other critical terms. This agreement is distinct from a formal loan agreement, as it primarily confirms the lender's intention to fund the loan based on mutual acceptance of its terms.

Key components of this form

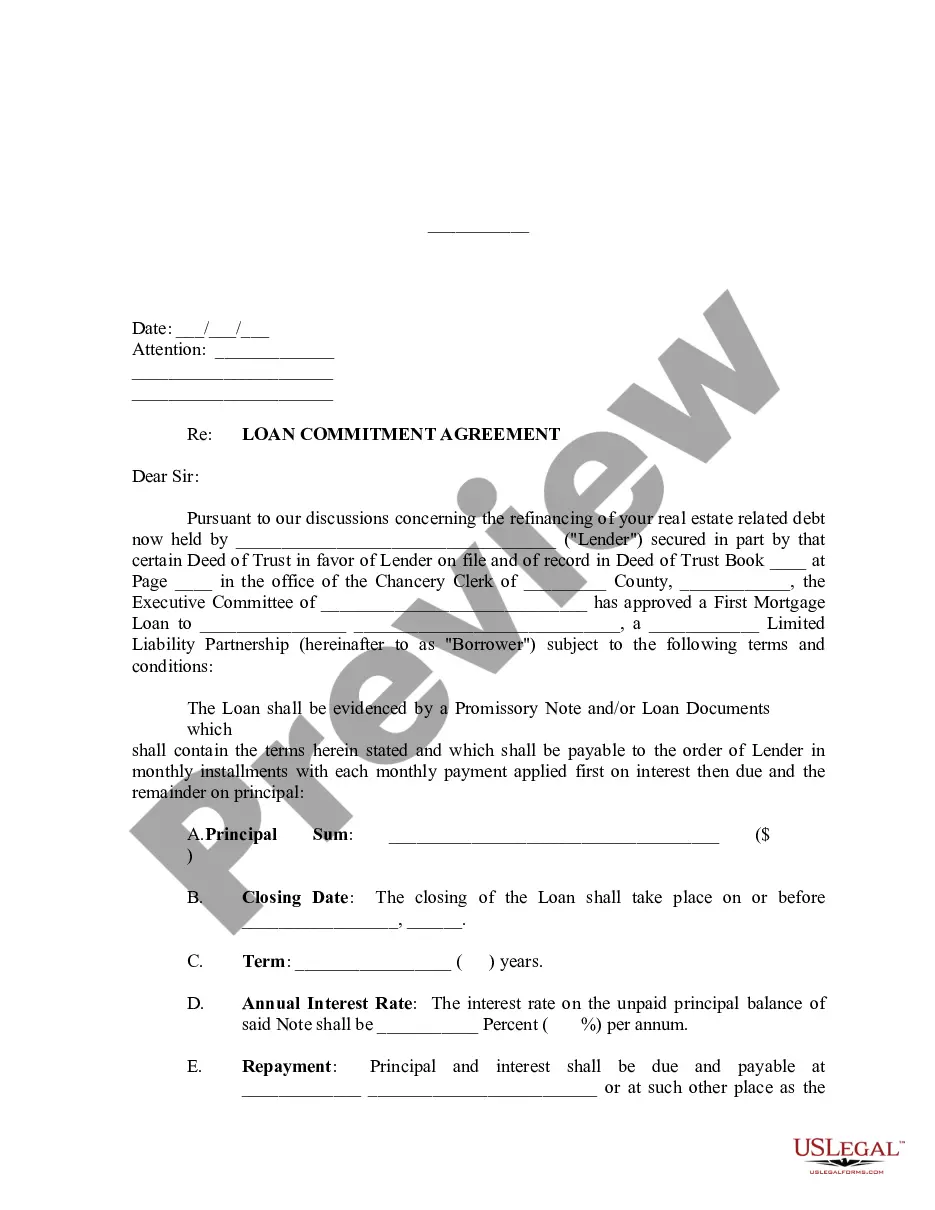

- Principal sum: The total amount of the loan being requested.

- Closing date: The date by which the loan must be finalized.

- Annual interest rate: The percentage of interest applied to the principal sum.

- Repayment structure: Details of how and when payments will be made.

- Escrow requirements: Information on taxes and insurance payments managed by the lender.

- Conditions for loan acceleration: Situations where the lender can demand immediate repayment.

When to use this form

You should use a loan commitment agreement when youâre applying for a loan to finance real estate, whether for purchasing property or refinancing existing debt. This form is particularly valuable for both commercial and residential properties, ensuring that both the lender and borrower have a clear understanding of their obligations and expectations before finalizing the loan transaction.

Who needs this form

This form is suitable for:

- Individuals looking to secure a mortgage for a home purchase.

- Business entities needing financing for commercial real estate.

- Property owners seeking to refinance existing loans.

- Borrowers who want to clarify lending terms with their financial institution.

Completing this form step by step

To complete your loan commitment agreement, follow these steps:

- Identify the parties involved by entering the names of the lender and borrower.

- Fill in the principal amount of the loan being requested.

- Specify the closing date and term length for the loan.

- Enter the annual interest rate and repayment details, including monthly installment amounts.

- Review and sign the agreement to signify acceptance of the terms.

Is notarization required?

This form does not typically require notarization unless specified by local law. However, it is advisable to verify state regulations regarding notarization to ensure compliance.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to specify the correct loan amount or interest rate.

- Neglecting to include the closing date, which can delay the loan process.

- Omitting crucial information about repayment terms and conditions.

- Not having all parties sign the agreement, resulting in legal issues.

Why complete this form online

- Convenience of access: Downloadable forms provide flexibility in completing documents at your own pace.

- Preparation assistance: Online forms are designed to offer guidance, minimizing errors.

- Legal assurance: Each form is drafted or reviewed by licensed attorneys, ensuring compliance with legal standards.

Main things to remember

- A loan commitment agreement outlines crucial loan terms between a lender and borrower.

- Individuals and businesses seeking financing for real estate should consider using this form.

- Ensuring all terms are clearly stated and signed by all parties is vital for legal enforceability.

- Review any state-specific regulations that might impact the terms of this agreement.

Looking for another form?

Form popularity

FAQ

You can certainly be denied for a mortgage loan after being pre-approved for it.The pre-approval process goes deeper. This is when the lender actually pulls your credit score, verifies your income, etc. But neither of these things guarantees you will get the loan.

Although the average time it takes for a lender to completely close a mortgage is 53 days, it could be as little as 15 days. The actual timing of the mortgage commitment letter arriving in escrow depends on many factors and must arrive before the house can close.

A letter of commitment is a formal binding agreement between a lender and a borrower. It outlines the terms and conditions. of the loan and the nature of the prospective loan. It serves as the agreement that initiates an official loan borrowing process.

A loan commitment is an agreement by a commercial bank or other financial institution to lend a business or individual a specified sum of money. Loan commitments are useful for consumers looking to buy a home or businesses planning to make a major purchase.

Lenders often include conditions that would allow them to step away from the loan, but simultaneously obligate the borrower to move forward with the loan as long as all the terms listed in the letter are met. This means that while the lender can still back out, some letters prevent borrowers from declining the loan.

The letter will also feature your lender's information, your loan number, and the date your commitment letter will expire. You'll also find the terms of you loan listed in the letter. These may include the amount of money you'll pay each month and the number of monthly payments you'll make until the loan is paid off.