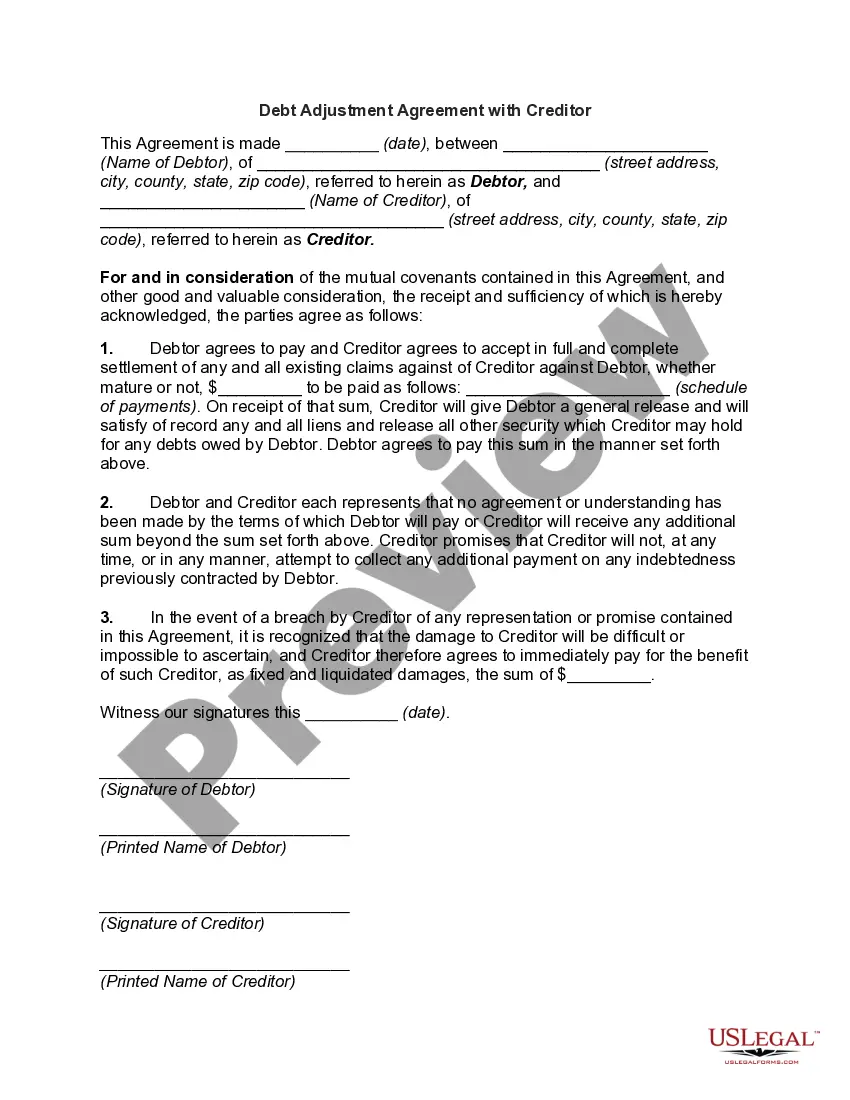

Debt Adjustment Agreement with Creditor

What this document covers

The Debt Adjustment Agreement with Creditor is a legal document that facilitates debt relief by allowing an individual or organization to repay debts over an extended period with reduced payments. This form outlines a mutual agreement between the debtor and creditor to settle outstanding debts, primarily focusing on manageable changes to repayment terms, unlike traditional loan agreements that may require immediate full payments.

Main sections of this form

- Date of the agreement.

- Names and addresses of both the debtor and the creditor.

- Terms of the debt adjustment and schedule of payments.

- Conditions for the release of liens and claims against the debtor.

- Clauses for the obligations of both parties regarding future payments and agreements.

- Signature lines for both the debtor and the creditor.

Common use cases

This form is applicable when a debtor is facing financial difficulties and needs to negotiate more favorable terms with a creditor. Situations may include the need to extend payment periods due to job loss, medical emergencies, or other unforeseen financial burdens. It is also useful for individuals or businesses looking to consolidate debts under new agreement terms that are manageable and feasible for them.

Who can use this document

- Individuals facing financial hardships struggling to meet current debt obligations.

- Businesses seeking to restructure existing debt to improve cash flow.

- Organizations that have multiple creditors and need to create uniform repayment terms.

- Creditors willing to negotiate and accept payment adjustments to support debtors in good faith.

How to prepare this document

- Start by filling in the date of the agreement.

- Enter the full names and addresses of the debtor and creditor.

- Specify the adjustment terms, including the amount to be settled and the payment schedule.

- Clearly state any conditions for the release of liens or claims.

- Both parties should sign and print their names at the bottom of the agreement.

Does this document require notarization?

In most cases, this form does not require notarization. However, some jurisdictions or signing circumstances might. US Legal Forms offers online notarization powered by Notarize, accessible 24/7 for a quick, remote process.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to include complete addresses for both debtor and creditor.

- Not specifying a clear payment schedule or amounts.

- Omitting signatures from either party, which invalidates the agreement.

- Neglecting to review local laws that may influence the terms of the agreement.

Why complete this form online

- The form is easily accessible, allowing for prompt completion without legal fees.

- It can be customized to meet your specific needs and circumstances.

- Reliable templates ensure compliance with legal standards.

- Convenient download options make it easy to print and sign the agreement.

Looking for another form?

Form popularity

FAQ

If you've been sued by your original creditor for a debt, and you're interested in settling, follow these three steps: Respond to the lawsuit. Send a debt settlement offer. Get the agreement in writing.

Most obligations settle between 30%-50% of the original value. If the debt collection agency is unwilling to accept any settlement, you may negotiate a payment plan with them. Payment plans can keep you out of court, and you won't need to fork over a large amount of cash at once.

Start by offering cents on every dollar you owe, say around 20 to 25 cents, then 50 cents on every dollar, then 75. The debt collector may still demand to collect the full amount that you owe, but in some cases they may also be willing to take a slightly lower amount that you propose.

Debt settlement is an agreement between a lender and a borrower for a large, one-time payment toward an existing balance in return for the forgiveness of the remaining debt. It is often used when a borrower cannot pay for unsecured debt like credit card debt.

Debt settlement involves offering a lump-sum payment to a creditor in exchange for a portion of your debt being forgiven. You can attempt to settle debts on your own or hire a debt settlement company to assist you. Typical debt settlement offers range from 10% to 50% of the amount you owe.

The creditor pays the collector a percentage, typically between 25% to 50% of the amount collected. Debt collection agencies collect various delinquent debts?credit cards, medical, automobile loans, personal loans, business, student loans, and even unpaid utility and cell phone bills.

It's better to pay off a debt in full (if you can) than settle. Summary: Ultimately, it's better to pay off a debt in full than settle. This will look better on your credit report and help you avoid a lawsuit. If you can't afford to pay off your debt fully, debt settlement is still a good option.

Debt settlement companies charge a fee, generally 15-25% of the debt the company is settling. The American Fair Credit Council found that consumers enrolled in debt settlement ended up paying about 50% of what they initially owed on their debt, but they also paid fees that cut into their savings.