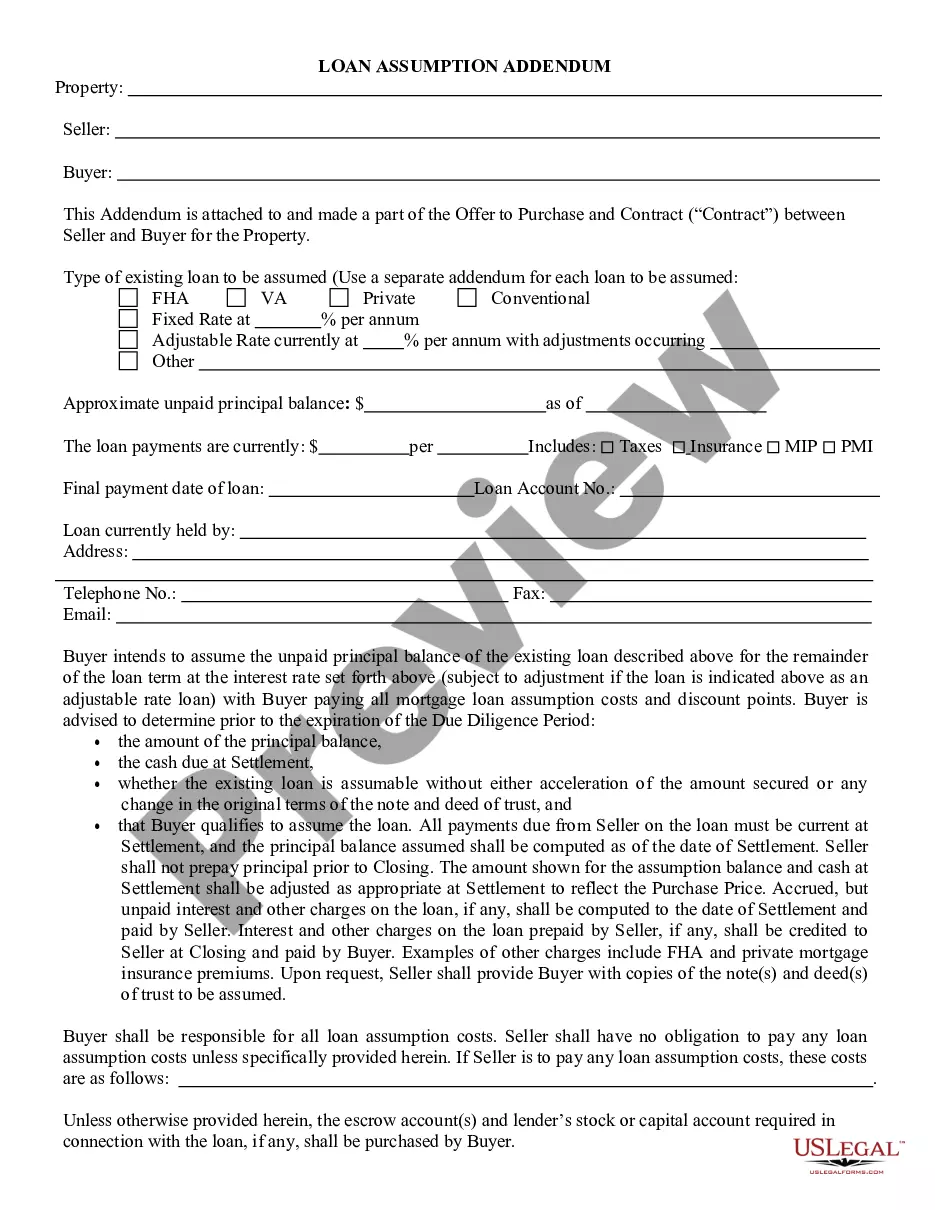

Loan Assumption Agreement

What is this form?

The Loan Assumption Agreement is a legal document that allows a grantee to assume the obligations of a loan secured by a property from a grantor. This form serves to formalize the transfer of responsibility for the loan and lien on the property, ensuring both parties are aware of their commitments. It distinguishes itself from other property transfer documents by explicitly involving the assumption of existing financial obligations associated with the property.

What’s included in this form

- Identification of the grantor (seller) and grantee (buyer).

- Details of the property being transferred, including location and description.

- Information about the lien and underlying loan, including amounts and payment obligations.

- Terms of the loan assumption, clarifying the grantee's responsibilities.

- Notarization requirement to validate the agreement.

Situations where this form applies

This form is essential when a property owner intends to transfer their property while allowing the buyer to take over the existing loan. It is particularly useful in real estate transactions where the buyer may not qualify for new financing but is willing to assume the existing mortgage. Additionally, it may be used when the buyer prefers to maintain the same loan terms that the grantor had initially agreed upon.

Who this form is for

- Property sellers looking to transfer their property and the associated loan obligations.

- Buyers interested in assuming an existing mortgage rather than obtaining new financing.

- Real estate agents involved in transactions where loan assumptions are being made.

- Attorneys handling property transfer agreements.

How to complete this form

- Identify the parties involved: enter the names of the grantor and grantee.

- Provide the property's details, including its location and description.

- Specify the loan information, including the amount owed and monthly payment details.

- Determine if lender consent is required for the loan assumption.

- Sign the agreement in the presence of a notary public, ensuring all signatures are properly executed.

Notarization guidance

This form must be notarized to be legally valid. US Legal Forms provides secure online notarization powered by Notarize, allowing you to complete the process through a verified video call.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to include all necessary signatures, especially from a notary.

- Not verifying whether lender consent is required for the assumption.

- Inaccurate or incomplete property descriptions.

Benefits of using this form online

- Convenience of downloading the form anytime and anywhere.

- Editability allows users to customize the agreement to fit their needs.

- Access to reliable legal templates drafted by licensed attorneys, ensuring compliance.

Main things to remember

- The Loan Assumption Agreement allows a buyer to take over an existing loan on a property.

- Both grantor and grantee must be informed and agree to the loan's terms.

- Notarization is required for the agreement to be valid.

Looking for another form?

Form popularity

FAQ

A fee that the buyer of a property with an assumable mortgage pays to the lender for the ability to take over the mortgage.

An assumable mortgage allows a buyer to take over the seller's mortgage. Once the assumption is complete, you take over the payments on a monthly basis, and the person you assume the loan from is released from further liability. If you assume someone's mortgage, you're agreeing to take on their debt.

Keep in mind that the average loan assumption takes anywhere from 45-90 days to complete. The more issues there are with underwriting, the longer you'll have to wait to finalize your agreement. Do yourself a favor and get the necessary criteria organized in advance.

If the assumable interest rate is lower than current market rates, the buyer saves money straight away. There are also fewer closing costs associated with assuming a mortgage.The seller may also benefit from using the assumable mortgage as a marketing strategy to attract buyers.

An assignment and assumption agreement is used after a contract is signed, in order to transfer one of the contracting party's rights and obligations to a third party who was not originally a party to the contract.The assignee must agree to accept, or "assume," those contractual rights and duties.

An assumable mortgage is a type of financing arrangement whereby an outstanding mortgage and its terms are transferred from the current owner to a buyer. By assuming the previous owner's remaining debt, the buyer can avoid having to obtain their own mortgage.

An assumable mortgage allows a buyer to take over the seller's mortgage. Once the assumption is complete, you take over the payments on a monthly basis, and the person you assume the loan from is released from further liability. If you assume someone's mortgage, you're agreeing to take on their debt.

The seller may also be required to sign the assumption agreement and the terms may release the seller from responsibility. The lender usually requires a credit history from the buyer before approving the assumption and the payment of assumption fee(s).