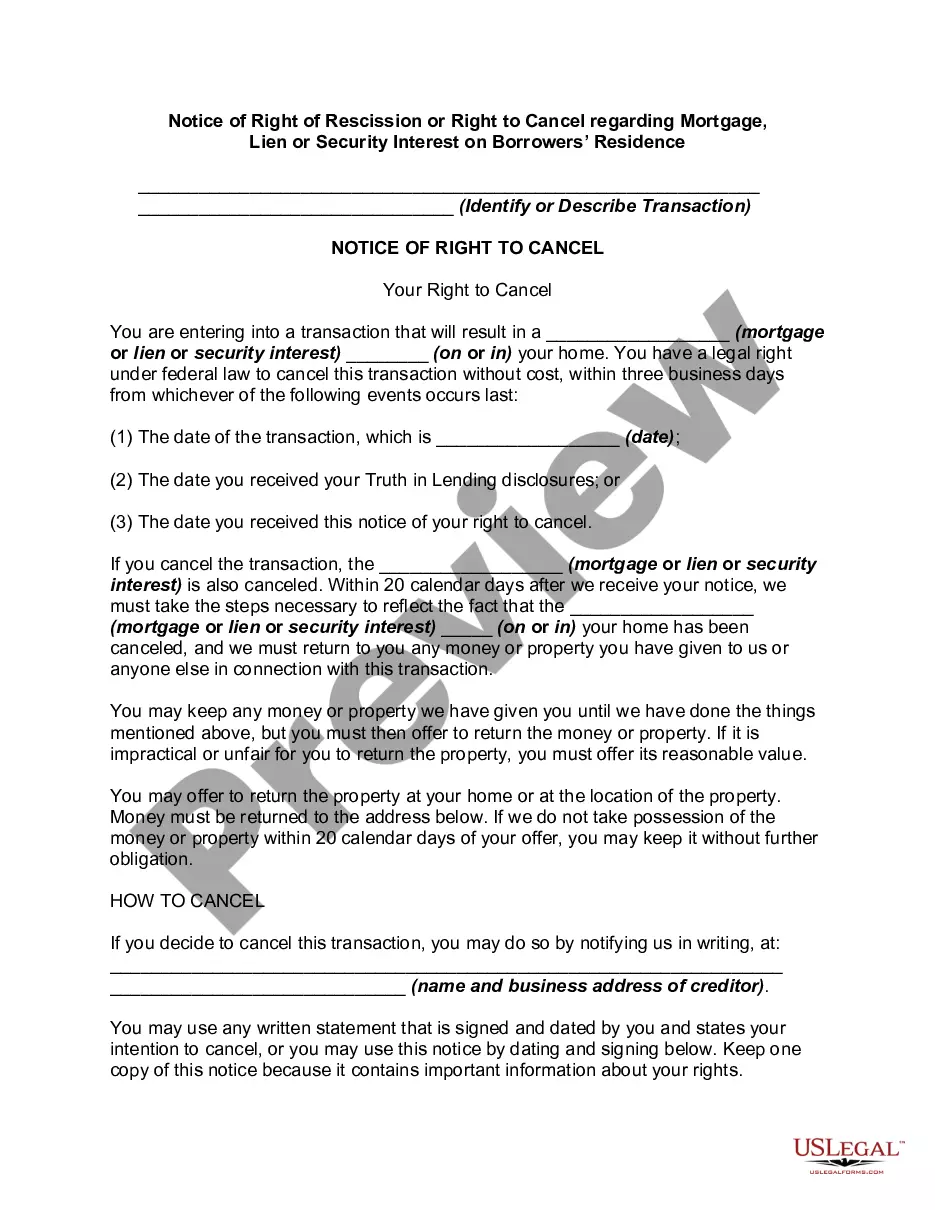

Right to rescind when security interest in principal dwelling is involved

About this form

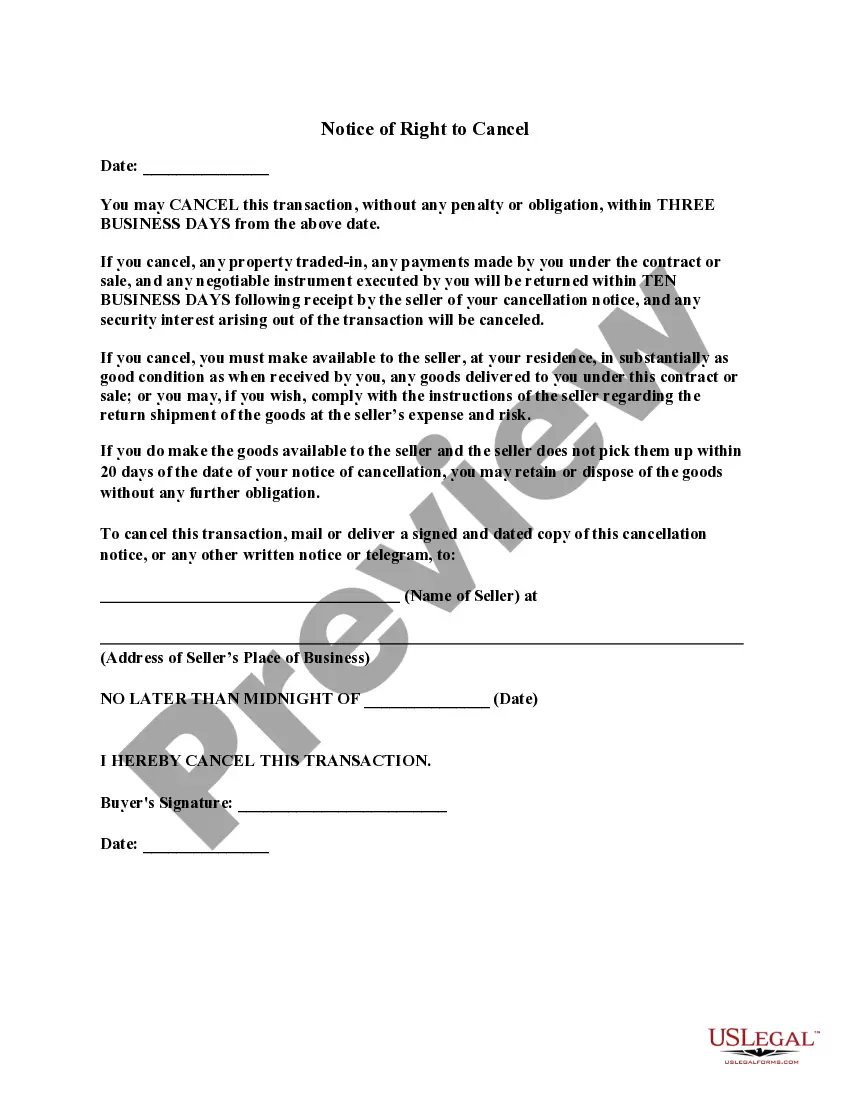

This form, known as the right to rescind when security interest in principal dwelling is involved, is designed for homeowners who enter into transactions that may result in a lien, mortgage, or other security interest on their principal dwelling. Under federal law, this form allows you to cancel the transaction within three business days without penalty, preserving your right to reverse the financial commitment made during the signing of certain agreements.

Key parts of this document

- Identifying information for the mortgage or transaction.

- Notification of your right to cancel the transaction.

- Timeline for rescission within three business days.

- Instructions for notifying the creditor of your intention to cancel.

- Signature fields for customer acknowledgment and creditor receipt.

When this form is needed

This form should be used when you enter into a mortgage agreement or a similar transaction on your primary residence. If you change your mind about the transaction after signing, this form allows you to exercise your right to rescind and avoid any financial obligation created by the agreement.

Who this form is for

- Homeowners involved in mortgage transactions.

- Individuals who have received a notice of transaction involving their principal dwelling.

- Borrowers who want to ensure they understand their rights under the Truth in Lending Act.

Steps to complete this form

- Identify the total dollar amount of the mortgage transaction.

- Provide the address of the property involved.

- Enter the date of the transaction.

- Fill in the name and address of the creditor.

- Sign and date the notice of cancellation.

Notarization requirements for this form

Notarization is generally not required for this form. However, certain states or situations might demand it. You can complete notarization online through US Legal Forms, powered by Notarize, using a verified video call available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to submit the cancellation notice by the deadline.

- Not keeping a copy of the cancellation notice for personal records.

- Overlooking any specific state requirements that may apply.

Why use this form online

- Convenient access to legal forms from anywhere.

- Easy to fill out the form with editable fields.

- Instant downloads ensure you have the form when you need it.

Legal use & context

- This form is legally recognized under federal law as part of the Truth in Lending Act.

- Failure to execute the rescission properly can result in the retention of financial obligations.

What to keep in mind

- You have the right to cancel certain transactions involving your home.

- This form facilitates the cancellation process without penalties.

- Always act within the specified timeline to ensure your rights are protected.

Looking for another form?

Form popularity

FAQ

Which of the following loans would not be subject to a right of rescission? The refinance of a two family primary residence through a state agency. Explanation: winning transactions originated through state agencies are not subject to right of rescission.

The right of rescission applies only to certain types of home loans: home refinancing, home equity loans, home equity lines of credit (HELOCs) and some reverse mortgages. You can't, for instance, cancel a contract on a new home purchase.

The right of rescission applies only to the addition of the security interest and not the existing obligation. The creditor shall deliver the notice required by paragraph (b) of this section but need not deliver new material disclosures. Delivery of the required notice shall begin the rescission period.

What Loans Have a Right of Rescission? The right of rescission applies only to certain types of home loans: home refinancing, home equity loans, home equity lines of credit (HELOCs) and some reverse mortgages. You can't, for instance, cancel a contract on a new home purchase.

When a consumer is acquiring or constructing a new principal dwelling, any loan subject to Reg. Z and secured by the equity in the consumer's current principal dwelling (e.g. bridge loan) is subject to the Right of Rescission regardless of the purpose of the loan.

Established by the Truth in Lending Act (TILA) under U.S. federal law, the right of rescission allows a borrower to cancel a home equity loan, home equity line of credit (HELOC), or refinance with a new lender, other than with the current mortgagee, within three days of closing.

(i) The consumer may exercise the right to rescind until midnight of the third business day following consummation, delivery of the notice required by paragraph (b) of this section, or delivery of all material disclosures, whichever occurs last.

The right of rescission doesn't apply when you're buying a home, and it only applies to a loan against your primary residence. So, for instance, you won't be able to rescind your mortgage if you're buying or refinancing a second home, vacation home, or investment property.