General Form of Inter Vivos Irrevocable Trust Agreement

Understanding this form

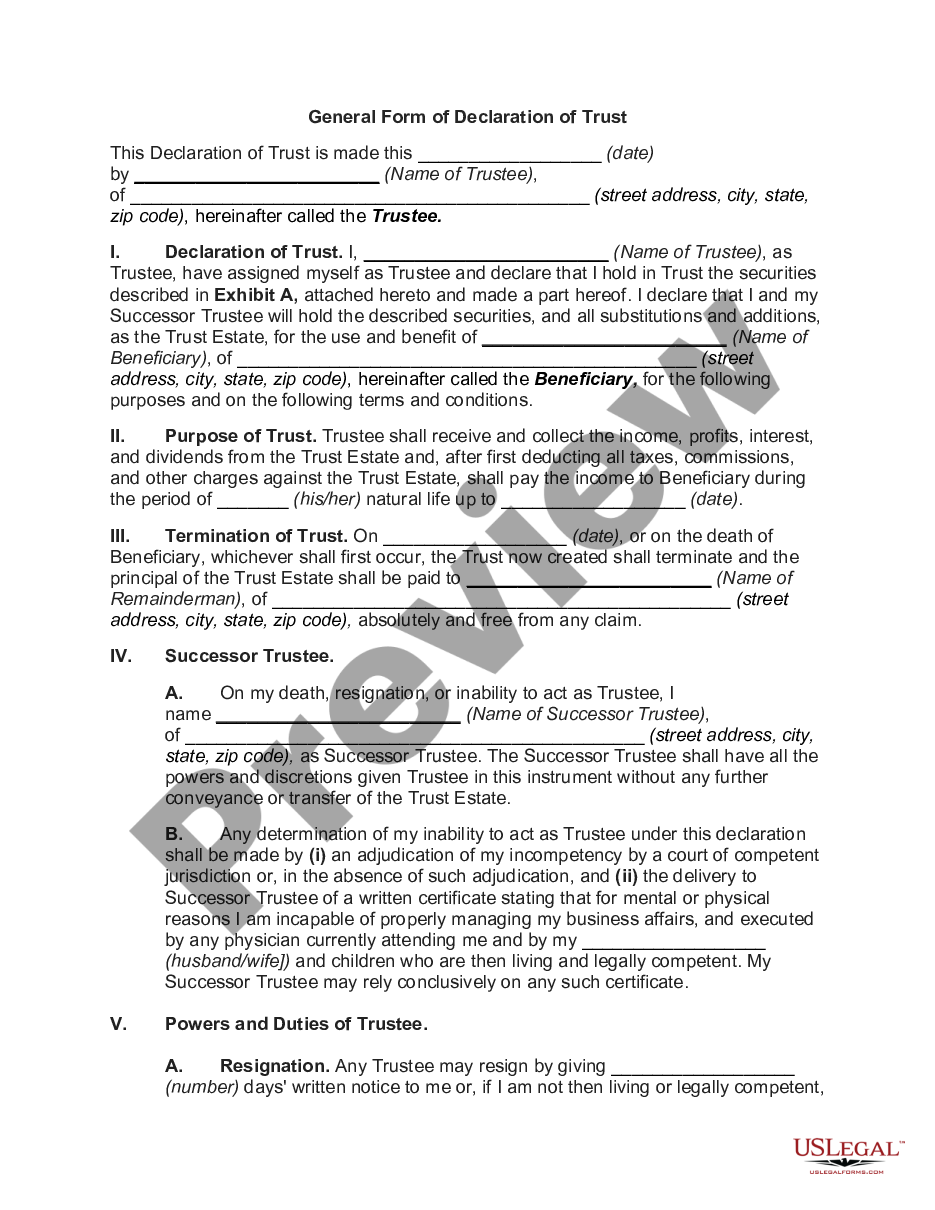

The General Form of Inter Vivos Irrevocable Trust Agreement is a legal document that establishes a trust during the grantor's lifetime, wherein the trust cannot be modified or revoked once executed. This type of trust is used to manage and distribute assets to beneficiaries, thus providing financial support while also allowing for tax benefits and asset protection. Unlike a revocable living trust, this irrevocable trust ensures that the assets are no longer considered part of the grantor's estate.

What’s included in this form

- Transfer in Trust: Defines how the trustor conveys property to the trustee.

- Disposition of Principal and Income: Outlines how income and principal will be managed and distributed.

- Powers of Trustee: Details the authority granted to the trustee concerning the trust assets.

- Duration of Powers of Trustee: States that the trusteeâs powers persist until all assets are distributed.

- Spendthrift Provision: Protects the trust assets from creditors of the beneficiaries.

When to use this form

This form is suitable when you want to create a trust that will manage and distribute your assets while you are alive. It is particularly useful for individuals looking to benefit specific beneficiaries, such as family members or charitable organizations, from their assets. You may also use this form to secure tax advantages or to protect your assets from potential creditors.

Who can use this document

- Individuals wishing to establish an irrevocable trust during their lifetime.

- Those looking to manage and protect assets for future beneficiaries.

- People wanting to provide for minors or those unable to manage their finances.

- Individuals seeking tax benefits associated with trust distributions.

Completing this form step by step

- Identify the parties involved: Specify the trustor, trustee, and beneficiaries.

- Describe the trust assets: Detail the property or assets being transferred to the trust.

- Outline the management provisions: Include instructions for how the trustee should manage the trust and its assets.

- Specify distribution terms: Indicate how and when beneficiaries will receive trust income and principal.

- Sign and date the document: Ensure all parties sign the agreement in accordance with state requirements.

Is notarization required?

This form does not typically require notarization unless specified by local law. However, to ensure the trust agreement is legally recognized and to simplify potential future use, you may choose to have it notarized.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to clearly define the trust assets, which can lead to disputes later.

- Not including detailed instructions for the trustee's management of trust assets.

- Neglecting to update beneficiaries' details as family dynamics change.

- Ignoring state-specific trust laws that may affect validity.

Benefits of completing this form online

- Immediate access to downloadable forms drafted by licensed attorneys.

- Ability to customize the trust agreement according to personal needs.

- Convenience of completing the form at your own pace.

- Secure storage of your legal documents for easy retrieval anytime.

What to keep in mind

- The General Form of Inter Vivos Irrevocable Trust Agreement is essential for establishing an irrevocable trust.

- This form helps manage and protect assets for beneficiaries while providing clear guidelines for the Trustee.

- It is vital to understand the implications of creating an irrevocable trust, including the inability to amend it once established.

Looking for another form?

Form popularity

FAQ

The step-up in basis is equal to the fair market value of the property on the date of death. In our example, if the parents had put their home in this irrevocable income only trust, and the fair market value upon their demise was $300,000, the children would receive the home with a basis equal to this $300,000 value.

Testamentary Trust: What's the Difference? explains that an inter vivos or living trust is drafted as either a revocable or irrevocable living trust and allows the individual for whom the document was established to access assets like money, investments and real estate property named in the title of the trust.

With an inter vivos trust, the assets are titled in the name of the trust by the owner and are used or spent down by him or her, while they are alive. When the trust owner passes away, the remainder beneficiaries are granted access to the assets, which are then managed by a successor trustee.

A living trust (sometimes called an inter vivos trust) is one created by the grantor during his or her lifetime, while a testamentary trust is a trust created by the grantor's will.In a testamentary trust, property must pass into the trust by way of the will and, thus, must go through the probate court process.

An inter vivos trust is a legal document created while the individual for which the trust is drawn up is still living.Once the trust owner passes away, the designated beneficiaries of the trust are granted access to the assets, which are then managed by a successor trustee.

In order to set up a living trust, you should first create a document stating your intention to create a trust, and name the people who you want to benefit from the trust. You should then create another document that states the property that you want to begin the creation of the trust with.

Plan the purpose and scope of the irrevocable trust. Choose a trustee. Prepare an irrevocable trust agreement. Obtain a taxpayer identification number for the trust from the Internal Revenue Service.

Irrevocable Trusts The trust assets will carry over the grantor's adjusted basis, rather than get a step-up at death. Assets held in an irrevocable trust that has its own tax identification number (i.e., nongrantor trust status) do not receive a new basis when the grantor dies.

As of 2019, attorney fees can range from $1,000 to $2,500 to set up a trust, depending upon the complexity of the document and where you live. You can also hire an online service provider to set up your trust. As of 2019, you can expect to pay about $300 for an online trust.