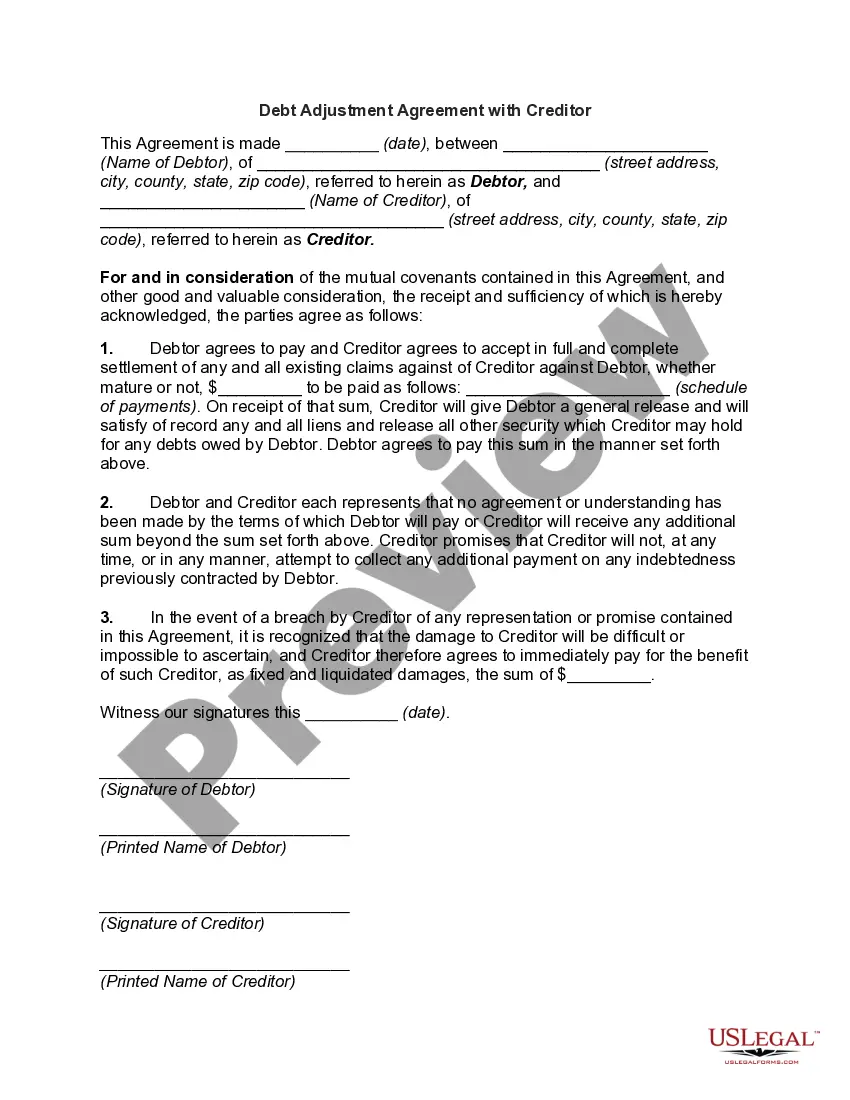

Debt Settlement Agreement

About this form

A Debt Settlement Agreement is a legal document that outlines the terms under which a debtor agrees to settle a debt for less than the full amount owed. This agreement helps both parties resolve disputes regarding the original obligation and can prevent further legal actions. Unlike standard repayment agreements, this form specifically addresses situations where the debtor is not able to pay the entire debt and seeks to reach a negotiated settlement with the creditor.

Key components of this form

- Date of the agreement.

- Identification of the creditor and debtor, including their addresses.

- Acknowledgment of the existing obligation and the amount owed.

- Details about the alternative payment method agreed upon.

- Consequences of a default on the agreement.

- Clause for the cancellation of original debts upon fulfillment of the agreement.

When to use this form

This form is used when a debtor is facing financial difficulties but wishes to settle their debts without declaring bankruptcy. It is particularly useful when there is a bona fide dispute between the creditor and debtor, and the parties have agreed upon new terms for repayment. Utilizing this agreement can help protect both parties and provide a clear path forward to resolve their financial relationship.

Who should use this form

- Individuals or businesses that owe money and cannot meet the original repayment terms.

- Creditors who are willing to settle for a lesser amount to recover a portion of the debt.

- Parties seeking to formalize an agreement to prevent future disputes regarding the settled debt.

How to prepare this document

- Identify the parties involved: fill in the names and addresses of the creditor and debtor.

- Enter the date of the agreement.

- Specify the original debt amount and provide details about the nature of the debt.

- Outline the new payment terms, including payment amounts, dates, and method.

- Sign and date the document at the specified location in the presence of a witness if necessary.

Does this document require notarization?

Notarization is generally not required for this form. However, certain states or situations might demand it. You can complete notarization online through US Legal Forms, powered by Notarize, using a verified video call available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to specify all payment details, which can lead to misunderstandings.

- Not acknowledging the original debt properly, leaving the agreement open to disputes.

- Omitting the consequences of default, which may complicate enforcement of the agreement.

Why complete this form online

- Convenient access to a legally vetted template that saves time.

- Editable format allows customization to fit individual circumstances.

- Reliable source drafted by licensed attorneys to ensure compliance with legal standards.

What to keep in mind

- A Debt Settlement Agreement is essential for negotiating repayment terms for less than the full debt.

- It formalizes the relationship and expectations between debtor and creditor.

- Proper completion helps protect both parties and clarifies their legal obligations.

Looking for another form?

Form popularity

FAQ

Offer a specific dollar amount that is roughly 30% of your outstanding account balance. The lender will probably counter with a higher percentage or dollar amount. If anything above 50% is suggested, consider trying to settle with a different creditor or simply put the money in savings to help pay future monthly bills.

The creditor and/or debt collectors name. The date the letter was drafted. Your name. Your account number.

A study by the Center for Responsible Lending showed that on average debts are settled at 48% of the outstanding balance. But that balance increases 20 percent due to late fees and other charges the creditor might impose during negotiation.

Assess your situation. Research your creditors. Start a settlement fund. Make the creditor an offer. Review a written settlement agreement. Pay the agreed-upon settlement amount.

"If you're happy with their offer, and you should be because it's less than what you actually owe them, then you should at least consider it," he says. The alternative, according to Ulzheimer, is the creditor either outsourcing the debt to a collector or even suing you.

It depends on what you can afford, but you should offer equal amounts to each creditor as a full and final settlement. For example, if the lump sum you have is 75% of your total debt, you should offer each creditor 75% of the amount you owe them.

Aim to Pay 50% or Less of Your Unsecured Debt If you decide to try to settle your unsecured debts, aim to pay 50% or less. It might take some time to get to this point, but most unsecured creditors will agree to take around 30% to 50% of the debt. So, start with a lower offerabout 15%and negotiate from there.

What percentage should I offer a full and final settlement? It depends on what you can afford, but you should offer equal amounts to each creditor as a full and final settlement. For example, if the lump sum you have is 75% of your total debt, you should offer each creditor 75% of the amount you owe them.