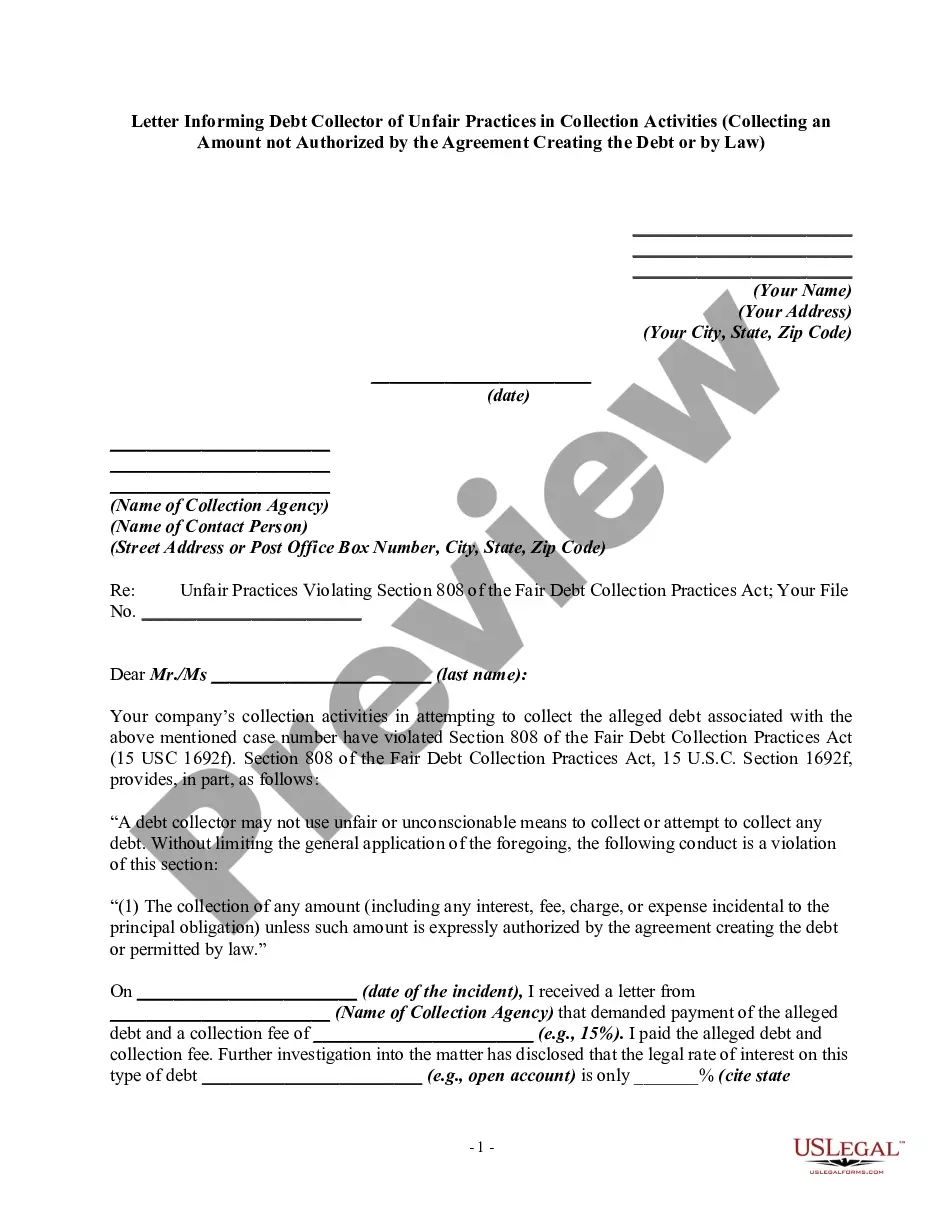

Notice to Debt Collector - Collecting an Amount Not Authorized by Agreement or by Law

Understanding this form

This Notice to Debt Collector is a legal document designed to inform a debt collector that they have violated the Fair Debt Collection Practices Act (FDCPA). It specifically addresses unlawful attempts to collect amounts not authorized by the original debt agreement or by law. This form serves as an important step in asserting your rights as a consumer and prompts the debt collector to comply with legal standards, helping to protect against abusive collection practices.

What’s included in this form

- Your name and address for identification.

- Debt collector's name and address to ensure proper delivery.

- Notice stating the specific violation of Section 808 of the FDCPA.

- Details of the unauthorized amount being collected.

- References to prior complaints filed with authorities.

- A request for the debt collector to cease the unlawful collection activities.

Common use cases

You should use this form if you have received communication from a debt collector regarding an amount that you believe exceeds what is legally owed or authorized by your agreement. This form becomes essential after you notice any violations of the Fair Debt Collection Practices Act, particularly if the debt collector continues to pursue the inflated amount despite your objection.

Who should use this form

This form is intended for consumers who:

- Have been contacted by debt collectors regarding amounts not authorized by their original debt agreement.

- Wish to formally notify debt collectors of their violations of the FDCPA.

- Are seeking to establish a legal document trail to support further action if necessary.

How to complete this form

- Enter your name and address at the top of the letter.

- Fill in the debt collector's name and address for proper identification.

- Clearly state the violation of Section 808 of the FDCPA and provide details about the unauthorized collection.

- Include references to any prior complaints made to authorities, if applicable.

- Sign and date the letter, then send it using certified mail to ensure delivery confirmation.

Is notarization required?

In most cases, this form does not require notarization. However, some jurisdictions or signing circumstances might. US Legal Forms offers online notarization powered by Notarize, accessible 24/7 for a quick, remote process.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to include specific details of the violation in the notice.

- Not sending the notice via certified mail, which can affect proof of delivery.

- Neglecting to keep copies of all correspondence for future reference.

- Using informal language instead of a professional tone.

Why complete this form online

- Convenient access to legally vetted templates drafted by licensed attorneys.

- Easy editing options to tailor the form to your specific situation.

- Instant availability, allowing you to prepare your notice without delays.

Legal use & context

This form is enforceable under the Fair Debt Collection Practices Act. It provides legal grounds for consumers to challenge unlawful debt collection practices. If the debt collector continues to violate the law after receiving this notice, it strengthens your case for potential civil action.

Looking for another form?

Form popularity

FAQ

You have the right to force the debt collector to prove you owe the money. Debt validation is your federal right granted under the Fair Debt Collection Practices Act (FDCPA). To request debt validation, you must send a written request to the debt collector within 30 days of being contacted by the collection agency.

Debt collectors cannot harass or abuse you. They cannot swear, threaten to illegally harm you or your property, threaten you with illegal actions, or falsely threaten you with actions they do not intend to take. They also cannot make repeated calls over a short period to annoy or harass you.

Write a letter disputing the debt. You have 30 days after receiving a collection notice to dispute a debt in writing. Dispute the debt on your credit report. Lodge a complaint. Respond to a lawsuit. Hire an attorney.

It's a violation of the collection practices act for a debt collector to refuse to send a validation notice or fail to respond to your verification letter. If you encounter such behavior, you can file a complaint with the Consumer Financial Protection Bureau.

The federal Fair Debt Collection Practices Act (FDCPA) (15 U.S.C. § 1692 and following) makes certain collection tactics that collection agencies use illegal, like: contacting third parties about your debt. engaging in conduct meant to harass, oppress, or abuse you, and. lying to you or misleading you.

If you pay the collection agency directly, the debt is removed from your credit report in six years from the date of payment. If you don't pay, it purges six years from the last activity date, but you may be at risk for wage garnishment.

If the collector completely fails to respond to the validation letter, again they have 30 days to do so, then legally they must cease collection efforts, and remove negative items placed by them on your credit report.

In other words, you only have the right to request verification of your debt from companies or law firms collecting the debt or which have purchased the debt from the original creditor. A collector's duty to verify a debt only kicks in if you send a specific, written request for verification.

By law, debt collectors may not: call you before 8 a.m. or after 9 p.m.threaten to seize, garnish, attach or sell your property or your wages unless they are permitted by law to do it and intend to do so. give false credit information about you to anyone, including a credit reporting company.