Montana Bankruptcy Guide and Forms Package for Chapters 7 or 13

About this form

The Montana Bankruptcy Guide and Forms Package for Chapters 7 or 13 is a comprehensive set of legal documents designed for individuals seeking to file for bankruptcy in Montana. This package includes essential forms, detailed instructions, and resources to help you understand the bankruptcy process. It clarifies the differences between Chapter 7, which offers liquidation of assets, and Chapter 13, which allows for a voluntary repayment plan. This structured support makes the process more manageable, especially for those unfamiliar with legal documentation and procedures.

What’s included in this form

- Chapter 7 Liquidation Forms: Documentation for assets and debts management.

- Chapter 13 Repayment Plan: Framework to create a repayment plan for creditors.

- Means Test Calculation: Tools to assess eligibility for Chapter 7 based on income.

- Exempt Property Listings: Instructions to claim and protect certain assets during bankruptcy.

- Detailed Instructions: Step-by-step guidance throughout the filing process.

When to use this document

This form package is necessary when individuals in Montana face overwhelming debt and are considering bankruptcy as a solution. It is particularly useful for those needing to assess their eligibility for Chapter 7 or Chapter 13 bankruptcy or for those who wish to understand the steps involved in either type of filing. If you recognize that you cannot afford to pay off your debts or if your situation has become unmanageable, this package provides the necessary framework to take action.

Who this form is for

- Individuals considering bankruptcy as a solution for their financial issues.

- Married couples seeking to file for bankruptcy together.

- Sole proprietors looking to manage business debts in bankruptcy.

- Those who wish to understand the differences between Chapter 7 and Chapter 13 bankruptcy before making a decision.

Instructions for completing this form

- Determine your eligibility by reviewing the requirements for Chapter 7 and Chapter 13.

- Complete the necessary bankruptcy forms including the Means Test Calculation if applicable.

- Document your exempt property on Schedule C to protect certain assets.

- Gather supporting financial documentation to substantiate your income and debt levels.

- Submit your completed forms along with any required fees to the appropriate bankruptcy court.

Does this document require notarization?

This form does not typically require notarization unless specified by local law. However, it is recommended to consult with a legal professional if you have any concerns about specific requirements in your case.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to disclose all debts and assets accurately.

- Not submitting the Means Test Calculation form when required.

- Ignoring exemptions which could help retain valuable property.

- Missing deadlines for filings and payments.

Why complete this form online

- Convenience of downloading and completing forms at your own pace.

- Reliable access to the latest legal forms drafted by licensed attorneys.

- Immediate updates to guidelines and instructions to ensure compliance with state laws.

Legal use & context

- Filing for bankruptcy can have long-term effects on your creditworthiness and financial standing.

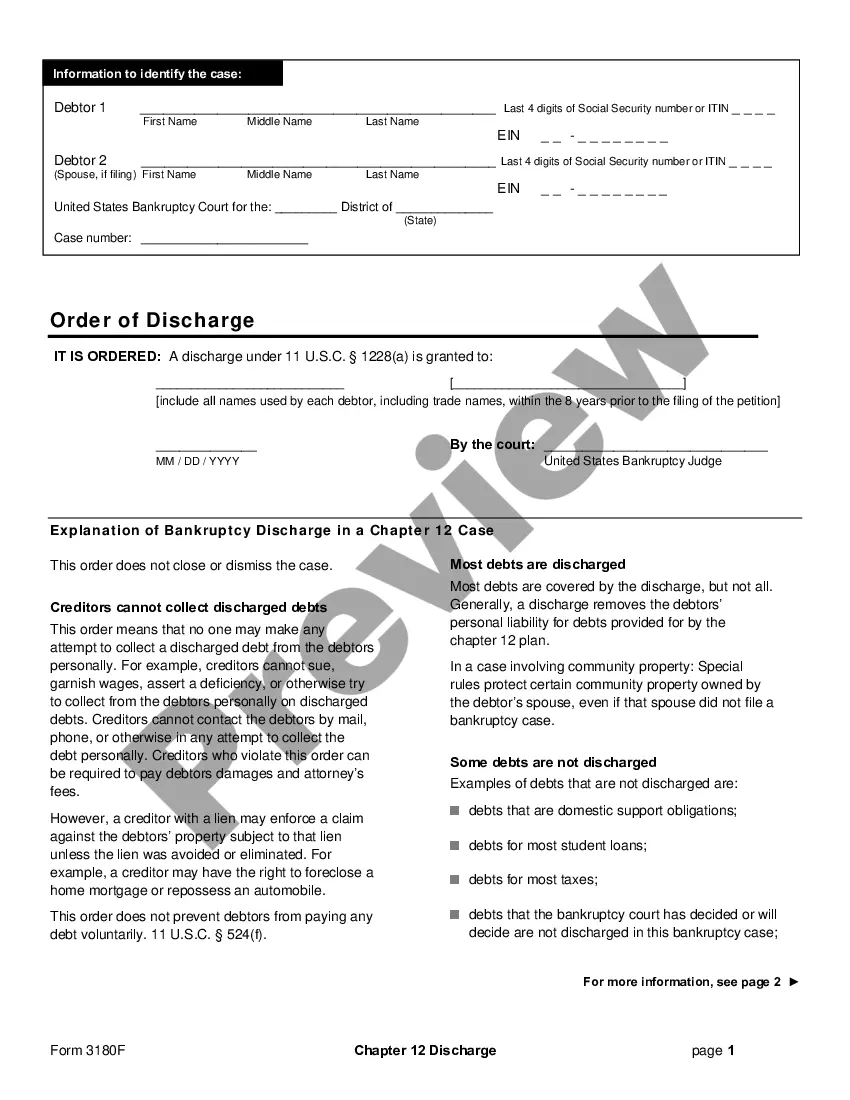

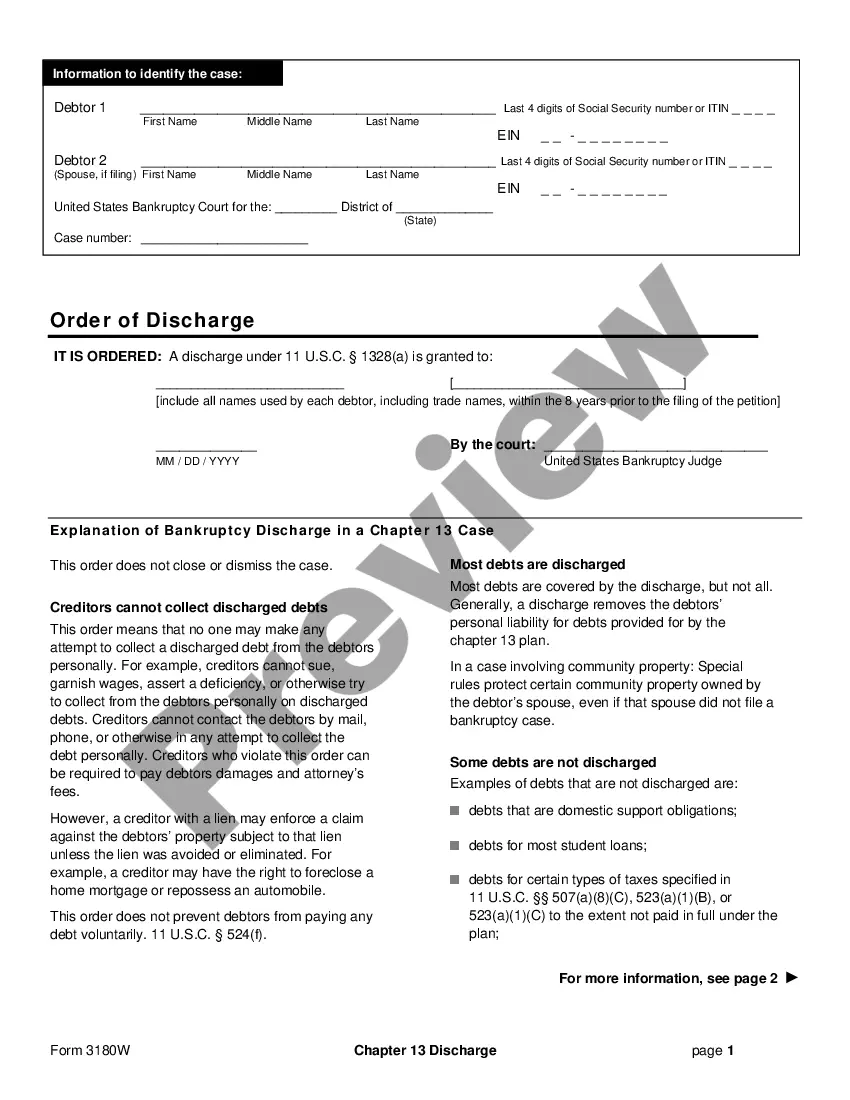

- Discharges may not include certain debts such as student loans and domestic support obligations.

- Consulting with a qualified attorney is advisable to navigate complex situations in bankruptcy.

Quick recap

- Understand the difference between Chapter 7 and Chapter 13 bankruptcies.

- Use this package to guide your bankruptcy filing process in Montana.

- Always disclose complete financial information to avoid complications.

- Consider legal advice to ensure the best approach to your financial difficulties.

Looking for another form?

Form popularity

FAQ

Stop making payments on debts that will get wiped out in bankruptcy and pay your attorney instead. borrow the fees from a friend, family member, or even your employer. retain a bankruptcy lawyer who will handle creditor calls while you pay fees over time. file on your own.

Six months of paycheck stubs. six months of bank statements. tax returns (the last two years) current investment and retirement statements. current mortgage and car loan statements. home and car valuations (printouts from online sources work)

Individuals can file bankruptcy without an attorney, which is called filing pro se.Filing personal bankruptcy under Chapter 7 or Chapter 13 takes careful preparation and understanding of legal issues.

Individuals can file bankruptcy without an attorney, which is called filing pro se. However, seeking the advice of a qualified attorney is strongly recommended because bankruptcy has long-term financial and legal outcomes.

There is no threshold amount that you need to reach to file a bankruptcy. Some chapters of bankruptcy have debt limits, but there is no such thing as a debt minimum. That being said, you certainly can and should evaluate if filing a bankruptcy makes sense in your current situation.

There is no minimum amount of debt you must have in order to file for bankruptcy relief. While the amount of your debt is an important factor to consider, there are other more important factors to take into account in determining if a bankruptcy filing is in your best interest.

There is no minimum amount of debt you must have in order to file for bankruptcy relief. While the amount of your debt is an important factor to consider, there are other more important factors to take into account in determining if a bankruptcy filing is in your best interest.

A chapter 13 bankruptcy is also called a wage earner's plan. It enables individuals with regular income to develop a plan to repay all or part of their debts. Under this chapter, debtors propose a repayment plan to make installments to creditors over three to five years.

Key Takeaways. Chapter 7 bankruptcy doesn't require a repayment plan but does require you to liquidate or sell nonexempt assets to pay back creditors.Chapter 13 bankruptcy eliminates qualified debt through a repayment plan over a three- or five-year period.