Royalty Payments

About this form

The Royalty Payments form is a lease rider that allows you to add specific provisions to an existing Oil and Gas Lease. It is designed for situations where you want to address particular concerns or limitations regarding royalty payments to the lessor. This form helps ensure clarity and protection for both parties involved in the lease transaction, differentiating itself from standard lease agreements by allowing tailored modifications focused on royalty payments and obligations.

Key components of this form

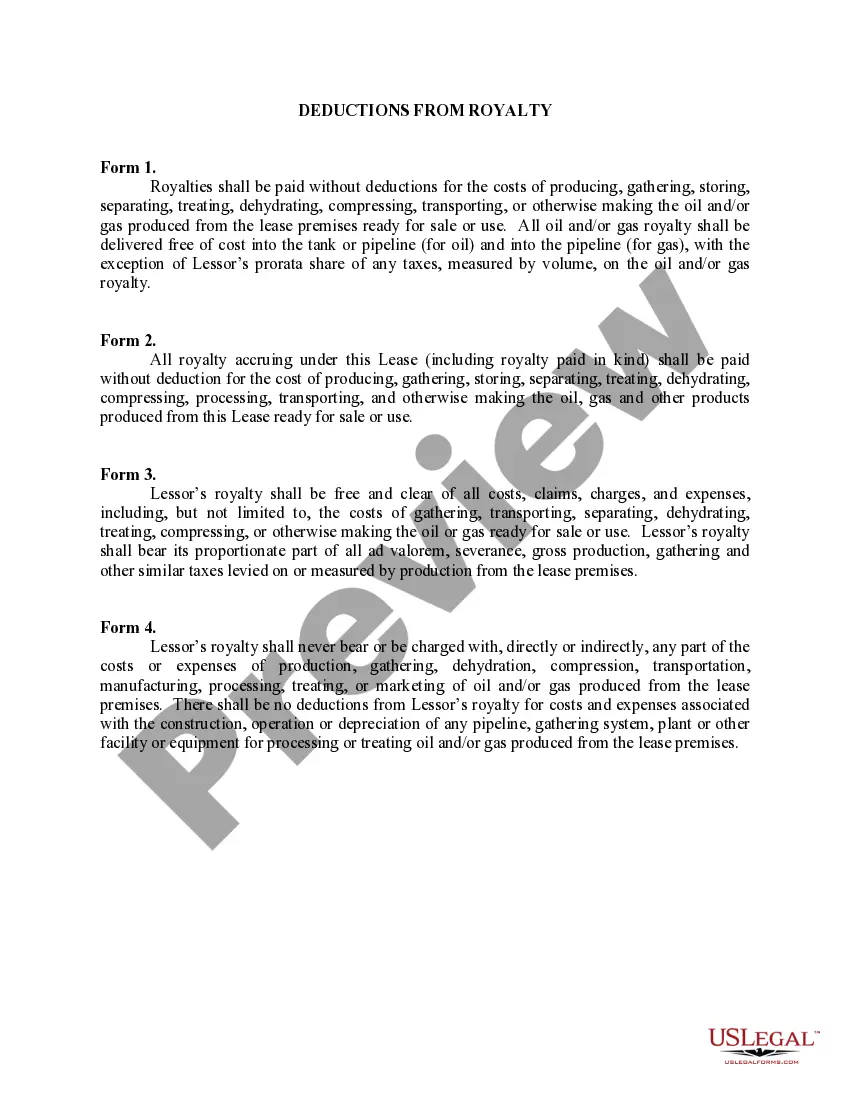

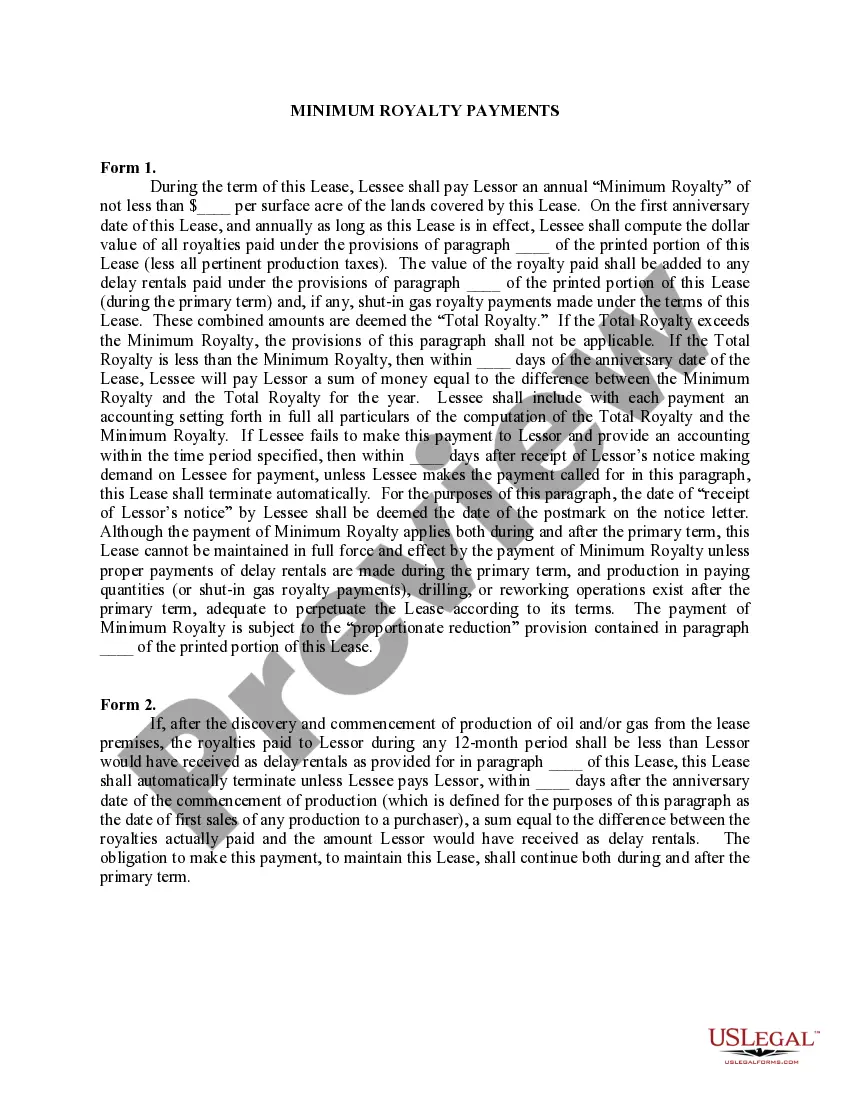

- Timelines for payment of royalties following the sale of production.

- Requirements for division orders reflecting the landowner's interest.

- Conditions under which failure to pay results in lease termination.

- Interest on unpaid royalties and obligations of the lessee regarding attorney fees.

- Details concerning the process for handling royalty disputes.

- Statement requirements accompanying payments to detail the production revenue breakdown.

When to use this document

Use this form when entering into a lease agreement for oil and gas extraction where you wish to customize the terms related to royalty payments. It is particularly useful if you have specific conditions or limitations you would like to impose on the lessee regarding the timing and manner of payments. This form is also appropriate in scenarios where you anticipate potential disputes over royalties and want to establish clear guidelines upfront.

Who this form is for

- Lessors who are leasing land for oil and gas production.

- Landowners seeking to outline specific conditions for royalty payments.

- Lessee entities looking to clarify their obligations regarding royalty distributions.

- Parties involved in oil and gas transactions who wish to document unique arrangements beyond standard contracts.

How to prepare this document

- Identify the lessor and lessee, including their legal names and contact information.

- Specify the terms regarding the timing of royalty payments after the first sale of oil or gas.

- Include information on division orders to reflect the lessor's interest in production.

- Detail the conditions for interest on overdue royalties and late payment terms.

- Provide statements that accompany payments to clearly describe the production details and payments made.

Is notarization required?

Notarization is generally not required for this form. However, certain states or situations might demand it. You can complete notarization online through US Legal Forms, powered by Notarize, using a verified video call available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to specify payment timelines clearly, leading to potential disputes.

- Not including all required information in payment statements, which can result in confusion.

- Neglecting to address interest provisions for late payments, leaving the lessor unprotected.

- Using outdated terms that do not comply with current state laws or regulations.

Benefits of completing this form online

- Convenient access to legally sound forms at any time without the need for in-person meetings.

- Editability allows for easy customization to meet specific needs.

- Immediate download ensures you can start the leasing process without delay.

- Reliability from forms drafted by licensed attorneys, ensuring legal compliance.

Looking for another form?

Form popularity

FAQ

Royalties proceeds from the sale of intellectual property are considered earned income.

Royalty income is considered a form of normal taxable income by the Internal Revenue Service and must be reported on your income tax return.

It is a nominal account and at the end of the accounting year, balance of Royalty account need to be transferred to the normal Trading and Profit & Loss account. Royalty, based on the production or output, will strictly go to the Manufacturing or Production account.

Some common examples of royalties include: Performance royalties: musicians produce copyrighted music, and anyone who wants to play the song in public or for commercial use must pay royalties. Book royalties: publishers pay authors for the right to sell and distribute their books.

The average royalty percentage applied to licensed services varies between 2%-15% of the media buy, depending on the attractiveness of the property. Another (much simpler) method of dealing with licensed service deals is to charge an annual fee for the licensee's right to use intellectual property.

Since royalties count as taxable income, you must report royalties on your federal income tax return. Royalty income is listed line 17 of Form 1040. According to the Internal Revenue Service, you must generally fill out and attach Schedule E to your 1040 to report royalty income.

Account for stepped royalty agreements. It is recorded in the ledger as a debit to royalty expense and a credit to accrued royalties (assuming the royalties are to be paid at the end of the period). For example, an author might receive $1 per book for the first 10,000 sold, then $1.50 per book for any sales after that.

Thus, in the circuit court's view, royalty payments that are calculated as a percentage of sales revenue from certain inventory, and incurred only upon the sale of such inventory, are not required to be capitalized.

The royalty expense incurred by the Company is classified as a general and administrative expense on the Company's consolidated statements of operations in accordance with the accounting guidance of ASC 605-45-45, Principal Agent Considerations, and ASC 705, Cost of Sales and Services.