Mortgage Review Worksheets

What is this form?

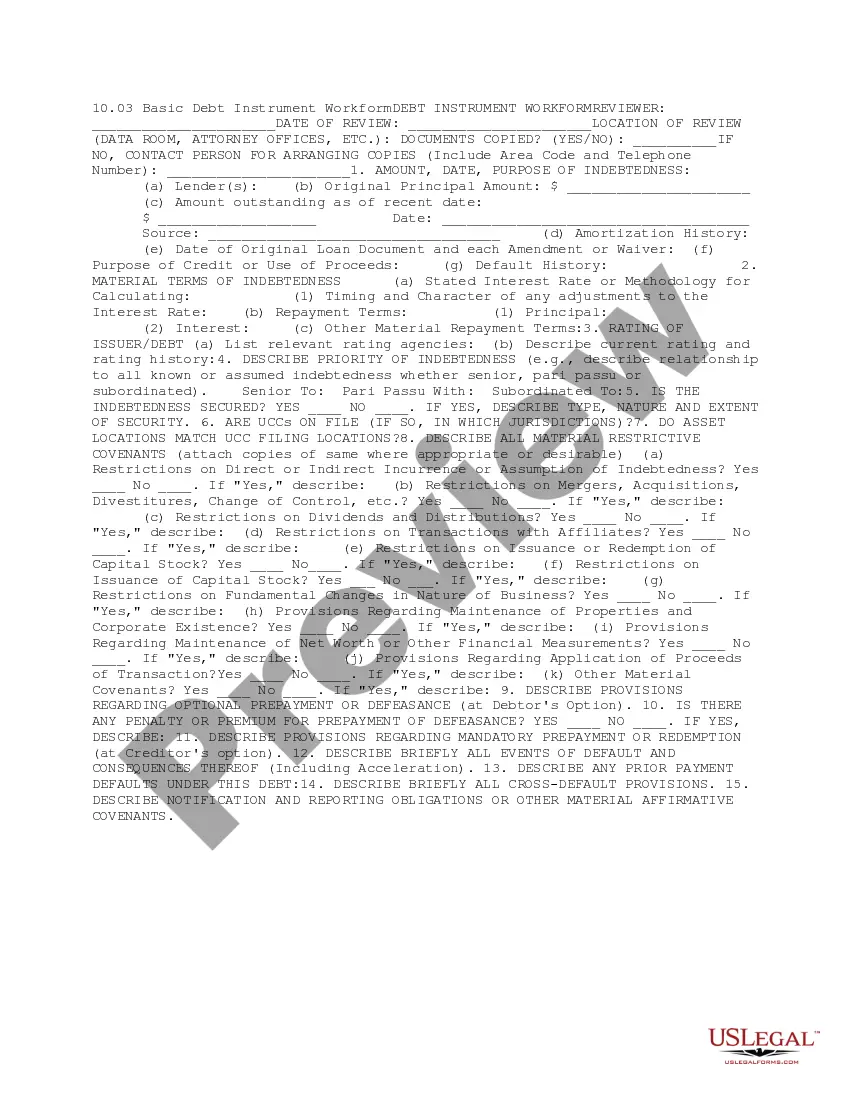

The Mortgage Review Worksheets are legal documents designed to assist in the review of mortgage-related matters. These worksheets provide a structured format to evaluate the terms, restrictions, and documentation associated with a mortgage. Unlike general mortgage agreements, these worksheets focus specifically on the review process, making them essential for detailed assessments and analyses of mortgage agreements.

Key components of this form

- Reviewer details and date of review

- Location of relevant documentation

- Description of the property and its ownership interest

- List of mortgage-related documents reviewed

- Details on mortgagor and mortgagee including names and addresses

- Information regarding restrictions and encumbrances

- Provisions related to environmental concerns, exculpation, priority, and indemnification

When this form is needed

The Mortgage Review Worksheets should be used when evaluating existing mortgage agreements. They are particularly useful in scenarios such as preparing for a refinancing, assessing the risk of a mortgage default, or when negotiating terms with a lender. Additionally, real estate professionals may use these worksheets when conducting due diligence or reviewing a mortgage for compliance with legal standards.

Who can use this document

- Homeowners looking to review their mortgage agreements.

- Real estate professionals conducting property evaluations.

- Lenders assessing the details of mortgage transactions.

- Attorneys advising clients on mortgage matters.

Completing this form step by step

- Identify and fill in the name of the reviewer and the review date.

- Specify the location of the relevant mortgage documentation.

- Provide a detailed description of the property, including its address.

- List all mortgage-related documents that were reviewed, including their names and dates.

- Detail the nature of the indebtedness secured by the mortgage.

- Note any restrictions or encumbrances related to the mortgagor and property.

Does this document require notarization?

This form does not typically require notarization to be legally valid. However, some jurisdictions or document types may still require it. US Legal Forms provides secure online notarization powered by Notarize, available 24/7 for added convenience.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to include all relevant mortgage documents.

- Neglecting to describe the character and amount of indebtedness properly.

- Omitting details regarding restrictions on property transfer.

- Not updating the date or reviewer information.

Benefits of using this form online

- Instant access to customizable templates tailored to your needs.

- Convenient downloadable format allows for easy record keeping.

- Reliability backed by licensed attorneys who draft the documents.

- Ability to make edits to the form as necessary before finalizing.

Looking for another form?

Form popularity

FAQ

To find the best mortgage lender, you need to shop around. Consider different options like your bank, local credit unions, online lenders and more. Ask each of them about rates, loan terms, down payment requirements, property insurance, closing cost and fees of all kinds, and compare these details on every offer.

One of the first things all lenders learn and use to make loan decisions are the Five C's of Credit": Character, Conditions, Capital, Capacity, and Collateral. These are the criteria your prospective lender uses to determine whether to make you a loan (and on what terms).

The four Cs of lending are capacity, capital, credit, and collateral. These primary factors are considered by lenders when determining your creditworthiness. lending process by assessing key borrower information and the associated risk to the lender of the borrower's ability to repay the mortgage.

Affordability. Lenders use a debt-to-income (DTI) ratio which tells them what percentage of your income will be going towards all of your bills. Credit health. Skin in the game. Down payment. One-time closing costs. Pre-paid costs due at closing.

For example, when it comes to actually applying for credit, the three C's of credit capital, capacity, and character are crucial.

DON'T: Make large deposits or withdrawals. Part of the mortgage application process includes providing recent bank statements. DON'T: Change jobs. DON'T: Make large purchases on credit. DON'T: Run up a home equity line of credit. DON'T: Close credit accounts. DON'T: Make payments on collection accounts.

They evaluate credit and payment history, income and assets available for a down payment and categorize their findings as the Three C's: Capacity, Credit and Collateral.

Points. Fees that have a link to your interest rate. Fees. Assorted fees such as loan origination and underwriting fees, broker fees, etc. Closing costs. The costs associated with closing your loan. Down payment. Private mortgage insurance.

The 4 C's of Underwriting- Credit, Capacity, Collateral and Capital. Guidelines and risk tolerances change, but the core criteria do not.