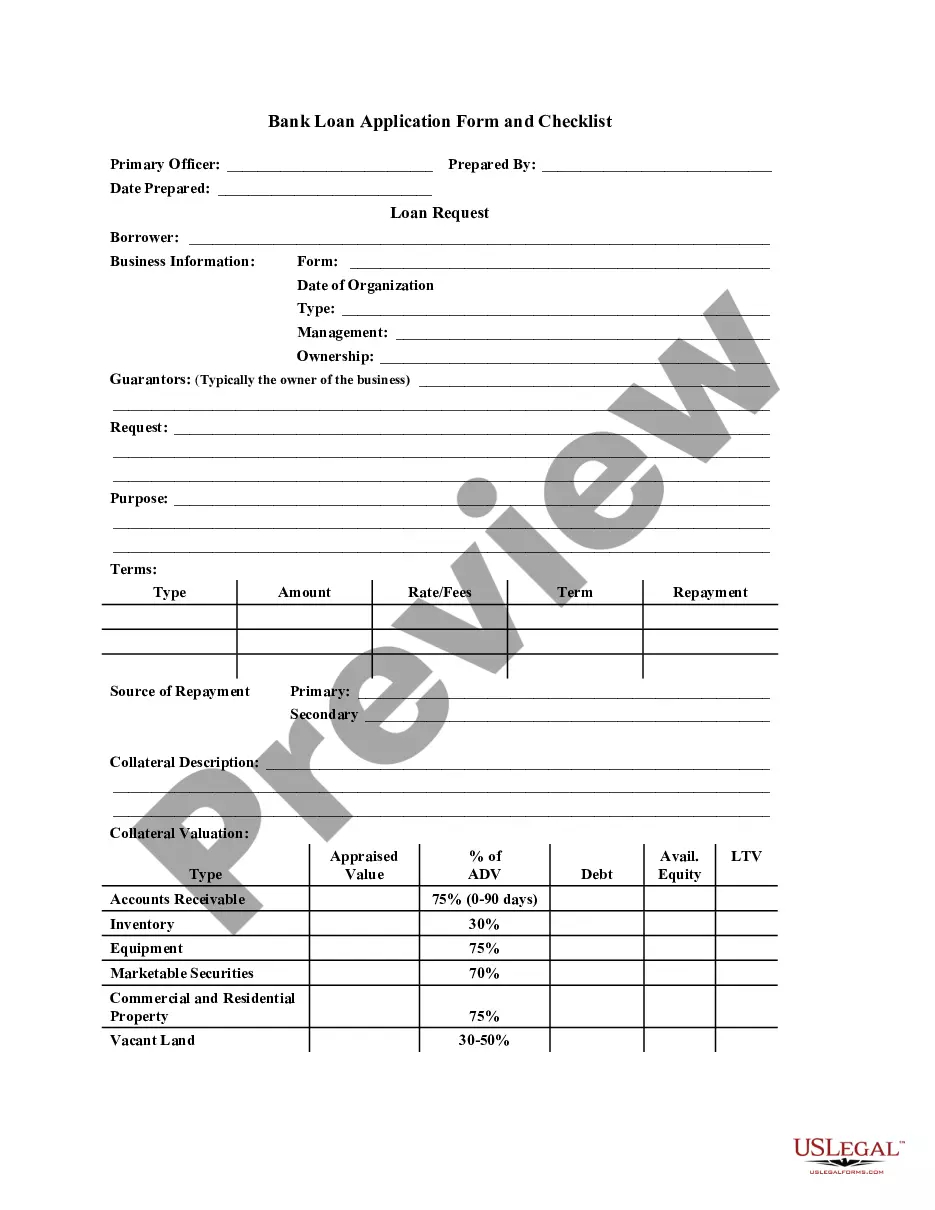

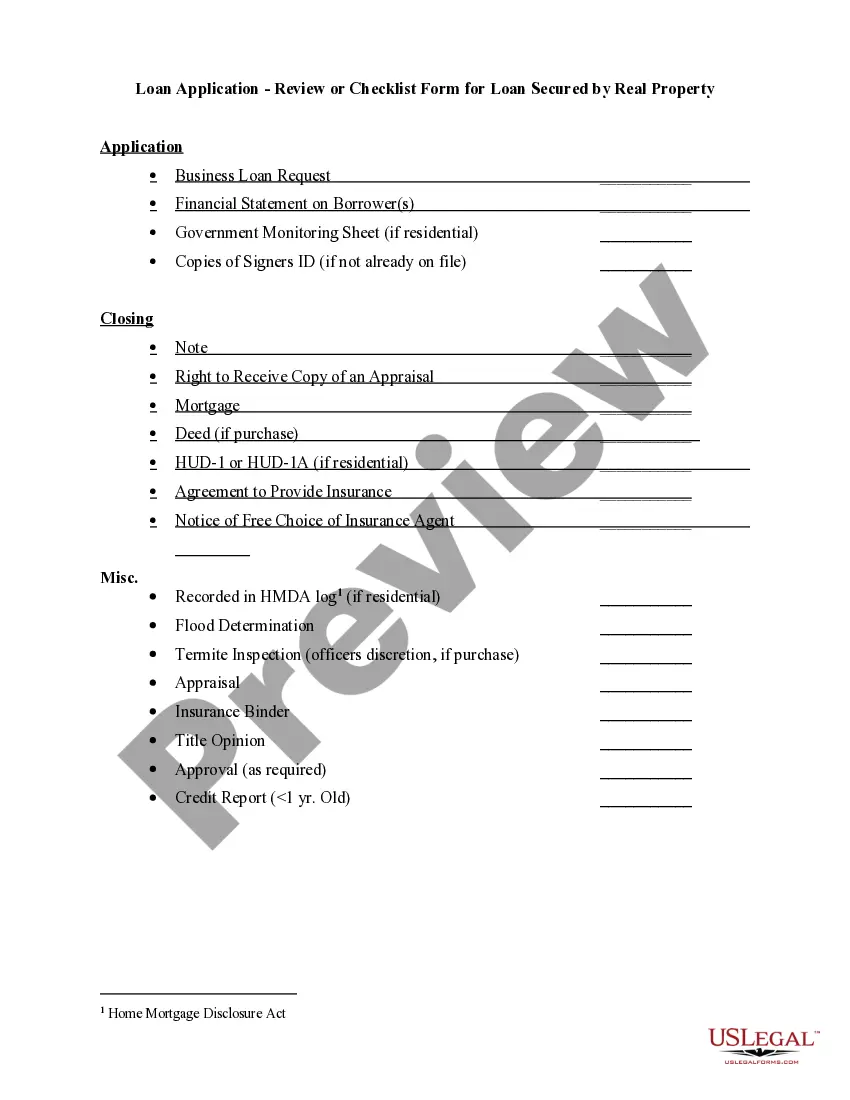

Loan Application - Review or Checklist Form for Loan Secured by Real Property

Overview of this form

The Loan Application - Review or Checklist Form for Loan Secured by Real Property is a key document used by borrowers seeking financing against real estate. This form outlines essential components needed to assess the loan request and ensures that all necessary information is provided. Unlike other loan application forms, this checklist format allows users to verify that they have included all required documentation, streamlining the application process.

Key components of this form

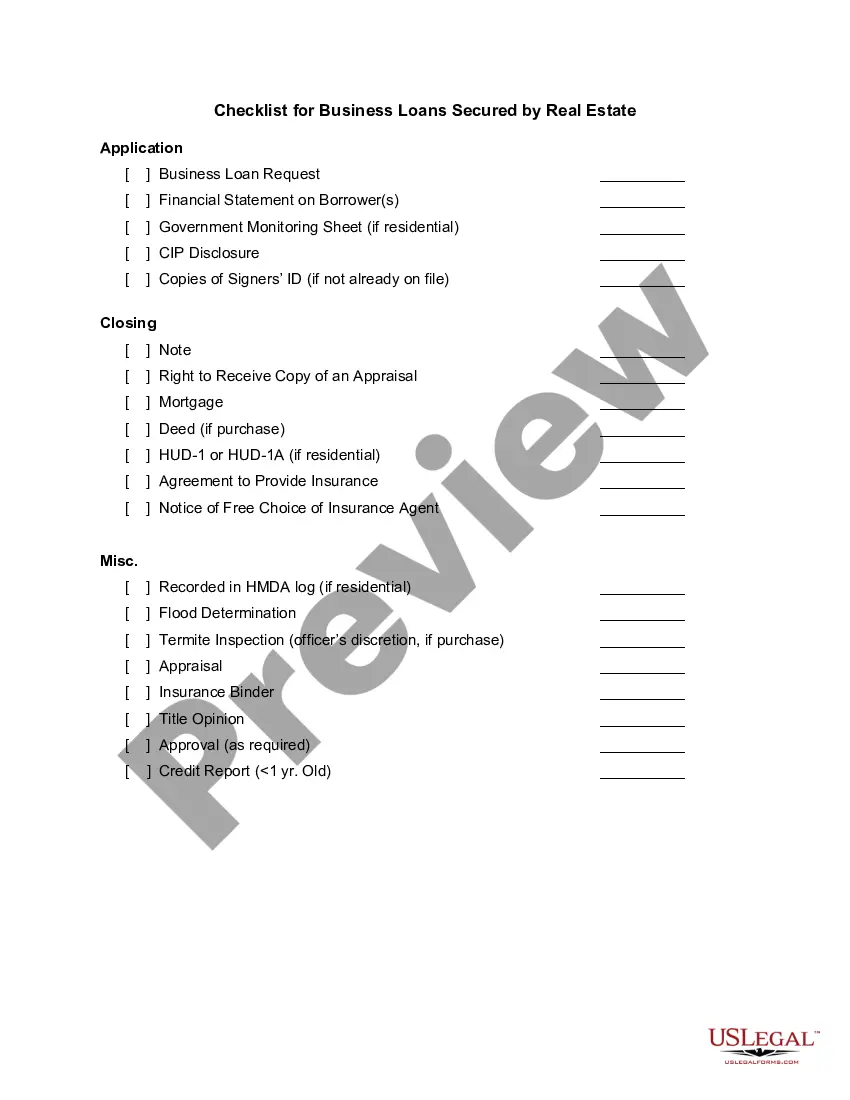

- Application Business Loan Request

- Financial Statement on Borrower(s)

- Government Monitoring Sheet (if residential)

- Copies of Signers' ID (if not already on file)

- Closing section for signatures and dates

When to use this form

This form is useful when applying for a loan secured by real property. It is appropriate for individuals or businesses looking to obtain financing for purchasing, refinancing, or developing real estate. Use this form to prepare your application thoroughly, ensuring all necessary documents are included to facilitate the approval process.

Who should use this form

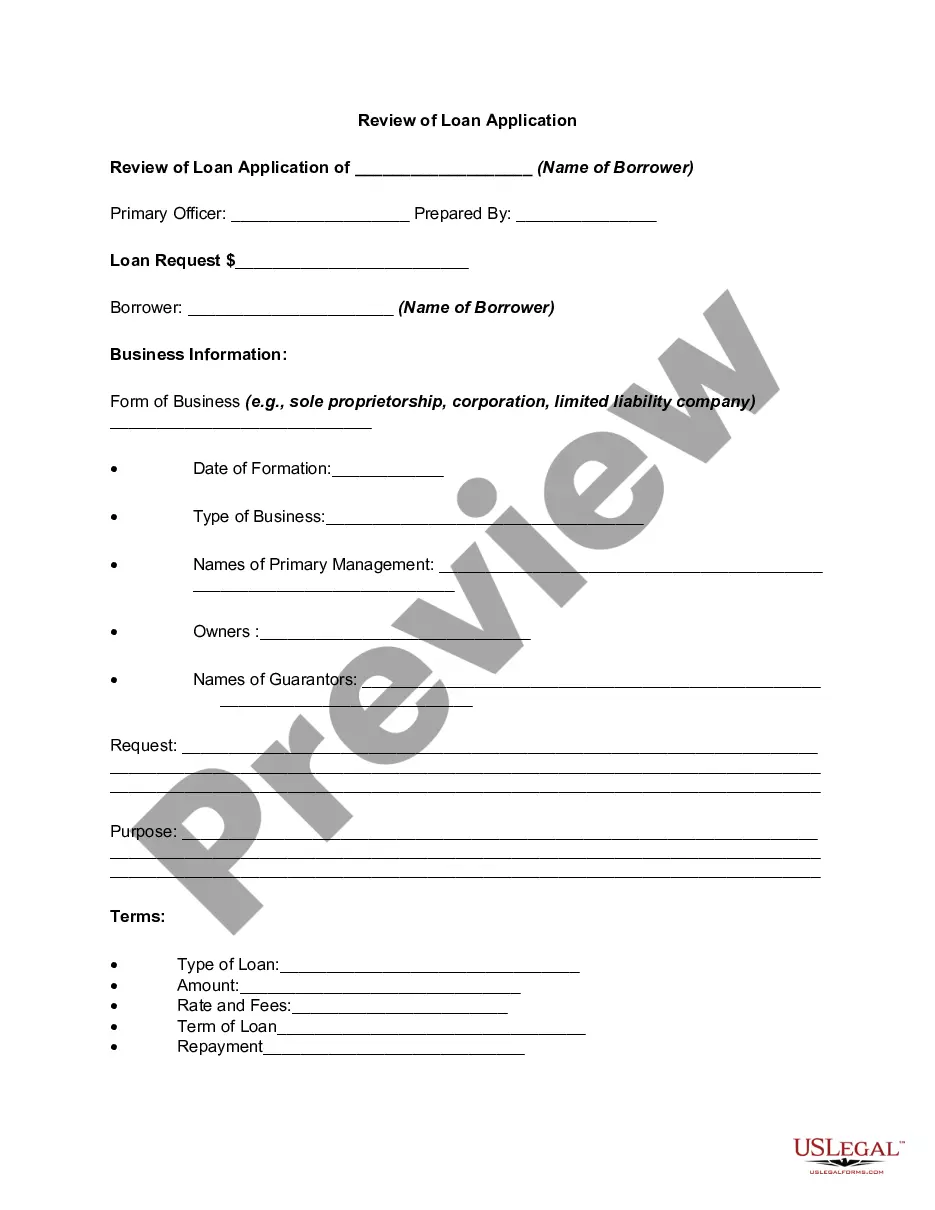

This form is intended for:

- Individuals applying for personal loans secured by their residential property

- Business owners seeking financing against commercial real estate

- Real estate investors looking to secure funding for property acquisitions

- Mortgage brokers assisting clients in the loan application process

How to complete this form

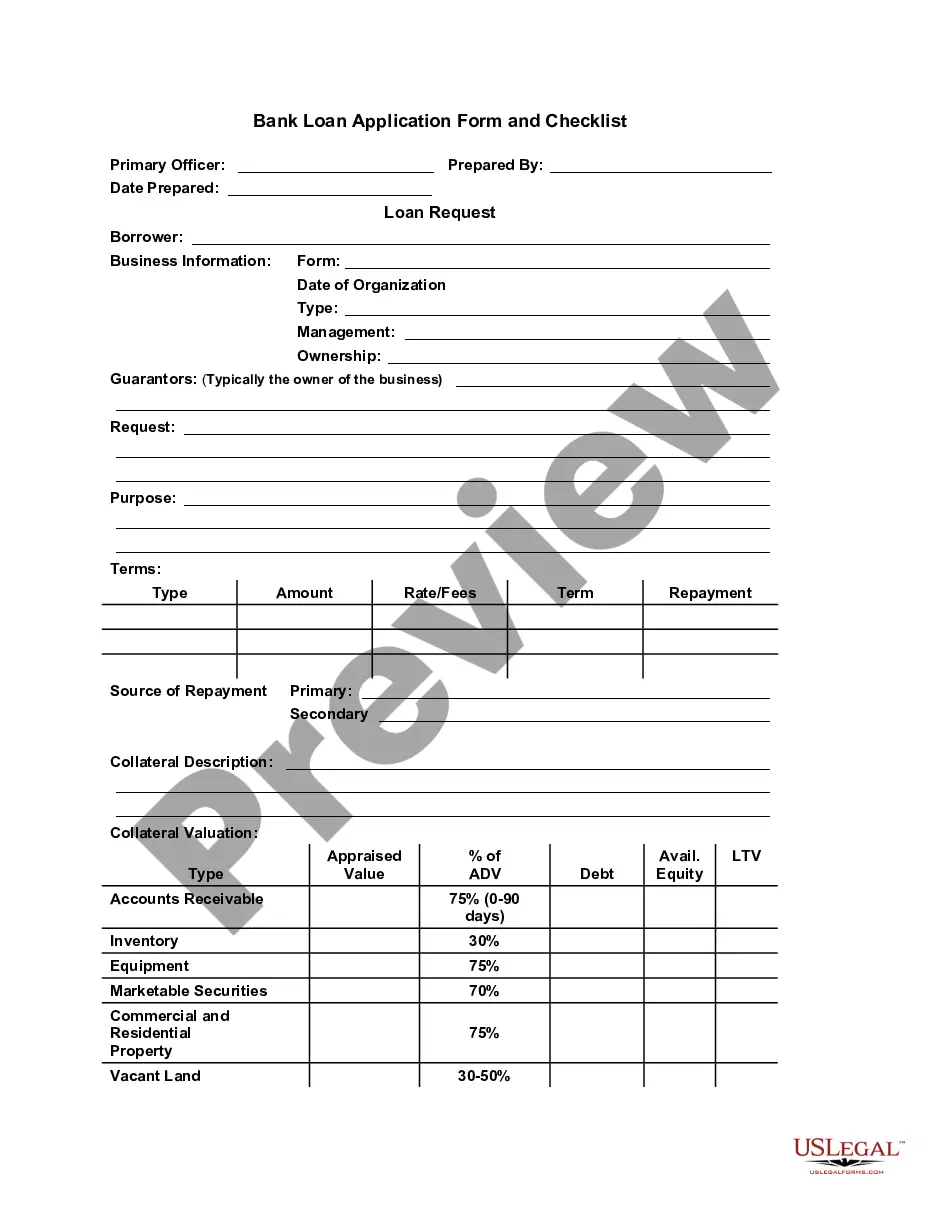

- Identify the borrower(s) and lender involved in the transaction.

- Complete the Application Business Loan Request with accurate details regarding the loan amount and purpose.

- Prepare the Financial Statement on Borrower(s) to provide a clear picture of financial standing.

- If applicable, include the Government Monitoring Sheet for residential loans.

- Attach copies of Signers' IDs, ensuring they are current and legible.

- Review all sections for completeness before submission.

Does this document require notarization?

In most cases, this form does not require notarization. However, some jurisdictions or signing circumstances might. US Legal Forms offers online notarization powered by Notarize, accessible 24/7 for a quick, remote process.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to include all required documentation, leading to delays.

- Providing inaccurate or outdated financial information.

- Not verifying the identity of all signers through proper ID documentation.

- Overlooking the requirement for a Government Monitoring Sheet if applying for a residential loan.

Benefits of completing this form online

- Easy access to download and fill out the form at your convenience.

- Editable format allows users to tailor the application to specific needs.

- Reliable legal language and structure ensure compliance with legal standards.

Quick recap

- The Loan Application Checklist helps ensure you submit a complete and organized application.

- Includes essential components like financial statements, ID copies, and regulatory sheets.

- Consult state-specific laws to adhere to requirements regarding loan applications.

Looking for another form?

Form popularity

FAQ

Used by borrowers seeking financing against real property, this checklist‑style form outlines the essential components and helps verify that all required information is provided. It guides applicants through a complete loan package for real estate loans, including the closing section for signatures and dates and items like the Application Business Loan Request, Financial Statement, Government Monitoring Sheet (if residential), and ID copies.

This form acts as a checklist to ensure all essential documents are included for a loan secured by real property. The listed components are: Application Business Loan Request, Financial Statement on Borrower(s), Government Monitoring Sheet (if residential), Copies of Signers' ID (if not already on file), and a closing section for signatures and dates. It helps applicants assemble a complete package for lender review.

Lenders typically want a complete, well‑documented loan package before reviewing an application. The form helps borrowers ensure key documents are included for a loan secured by real property, such as the Application Business Loan Request, Financial Statement on Borrower(s), residential Government Monitoring Sheet (if applicable), copies of signers’ ID, and a closing section with signatures. The checklist supports a smoother review.

The purpose of a loan review is to confirm the loan package is complete and ready for evaluation for a loan secured by real property. By using a checklist format, the form ensures required documentation is included and properly organized, helping speed the lender's assessment and underwriting process.

During the loan review, the lender checks that all required documents are present and correctly completed per the checklist. The form guides this process by citing components like the Application Business Loan Request, Financial Statement on Borrower(s), Government Monitoring Sheet (if residential), copies of signers’ IDs, and the closing section for signatures and dates, facilitating underwriting.

This form differs from many other loan application forms by using a dedicated checklist format to verify that every required document is included, plus a closing section for signatures and dates. It is specifically designed for loans secured by real property, including items like the Government Monitoring Sheet (for residential loans), which may not appear on standard applications.