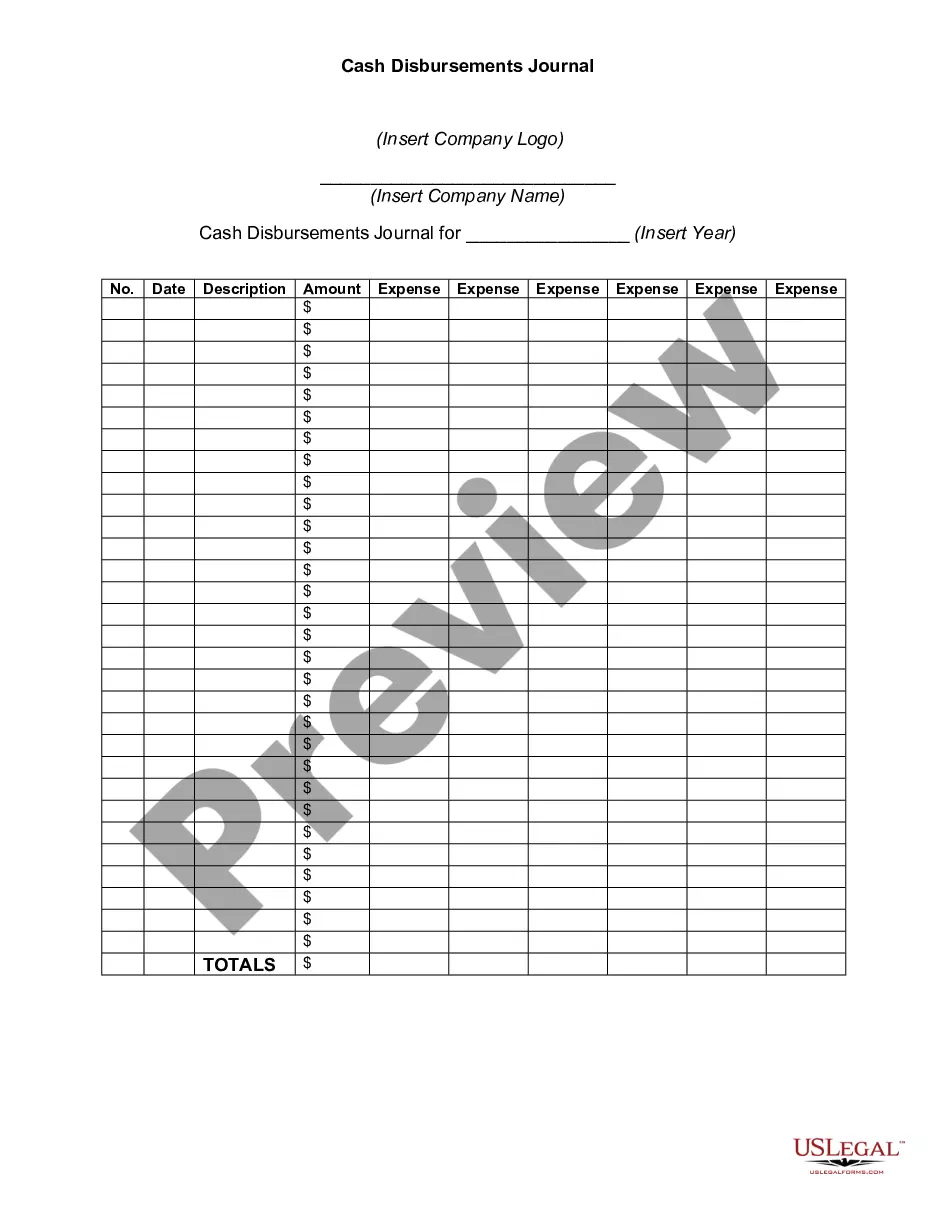

Cash Disbursements Journal

About this form

The Cash Disbursements Journal is a financial record-keeping tool designed to track the cash payments and disbursements from your business. This form helps you maintain a monthly record of all outgoing cash transactions, enabling better financial oversight and planning. It is beneficial to use this journal alongside the Cash Receipts Journal, which records incoming cash, creating a comprehensive overview of your business's cash flow.

Key components of this form

- Month: Specifies the month for tracking disbursements.

- General Ledger Number: Provides a reference number for accounting purposes.

- Date: Records the date of each transaction.

- Check Payee: Identifies who received the payment.

- Account Credited: Indicates the account that will be credited.

- Account Debited: Shows the account from which the cash is deducted.

- Amount Payable: States the total amount of the payment.

When to use this form

You should use the Cash Disbursements Journal whenever your business makes cash payments, including paying vendors, settling bills, or making other financial disbursements. This form is particularly useful for tracking monthly expenses and ensuring accurate financial reporting.

Who can use this document

- Small business owners managing cash flow.

- Accountants and bookkeepers maintaining financial records.

- Individuals responsible for business finances.

Completing this form step by step

- Identify the month for which you are recording cash disbursements.

- Enter the general ledger number for proper account tracking.

- Fill in the date for each disbursement transaction.

- Specify the name of the payee receiving the payment.

- Indicate which account is credited and which account is debited.

- Finally, write the total amount payable for each transaction.

Notarization guidance

This form does not typically require notarization unless specified by local law. However, it's important to always check state regulations to ensure compliance.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to update the journal regularly, leading to inaccurate records.

- Omitting accounts to be credited or debited, causing discrepancies in financial reporting.

- Not double-checking the amounts payable, which can result in financial errors.

Why use this form online

- Convenience of accessing and updating your financial records anytime.

- Editability allows for corrections without needing to start over.

- Reliable templates ensure compliance with legal requirements.

Main things to remember

- The Cash Disbursements Journal is essential for tracking business expenses.

- It is effective when used alongside a Cash Receipts Journal for comprehensive cash flow management.

- Proper completion of the form ensures accurate financial reporting and accountability.

Looking for another form?

Form popularity

FAQ

Create the sales entry Record your cash sales in your sales journal as a credit and in your cash receipts journal as a debit. Keep in mind that your entries will vary if you offer store credit or if customers use a combination of payment methods (e.g., part cash and credit).

In business accounting, a disbursement is a payment in cash during a specific time period and is recorded in the general ledger of the business. This record of disbursements shows how the business is spending cash over time. Payments of dividends to shareholders are often termed disbursements.

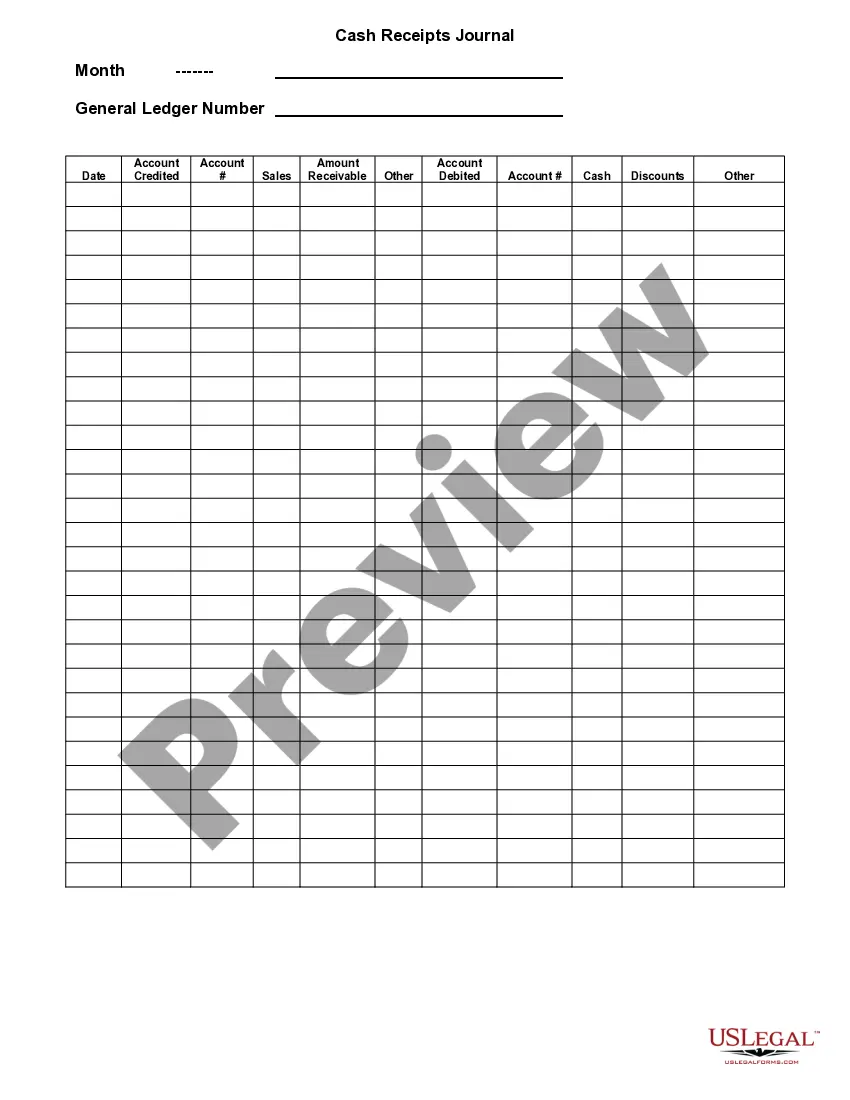

The cash receipts journal is used to record all transactions involving the receipt of cash, including such transactions as cash sales, the receipt of a bank loan, the receipt of a payment on account, and the sale of other assets such as marketable securities.

When recording cash payments to suppliers it is quite common for the cash disbursement journal to include a discounts received column. By using a discounts received column, the business can use the cash disbursement journal to record the invoiced amount, the discount received, and the cash payment.

A cash disbursement journal is a record kept by a company's internal accountants that itemizes all financial expenditures a business makes before those payments are posted to the general ledger.

In other words, a cash disbursements journal is used to record any transaction that includes a credit to cash. All cash inflows are recorded in another journal known as cash receipts journal.

When recording cash payments to suppliers it is quite common for the cash disbursement journal to include a discounts received column. By using a discounts received column, the business can use the cash disbursement journal to record the invoiced amount, the discount received, and the cash payment.

For example, cash disbursed to pay bills is credited to the Cash account (which goes down in value) and is debited to the account from which the bill or loan is paid, such as Accounts Payable.