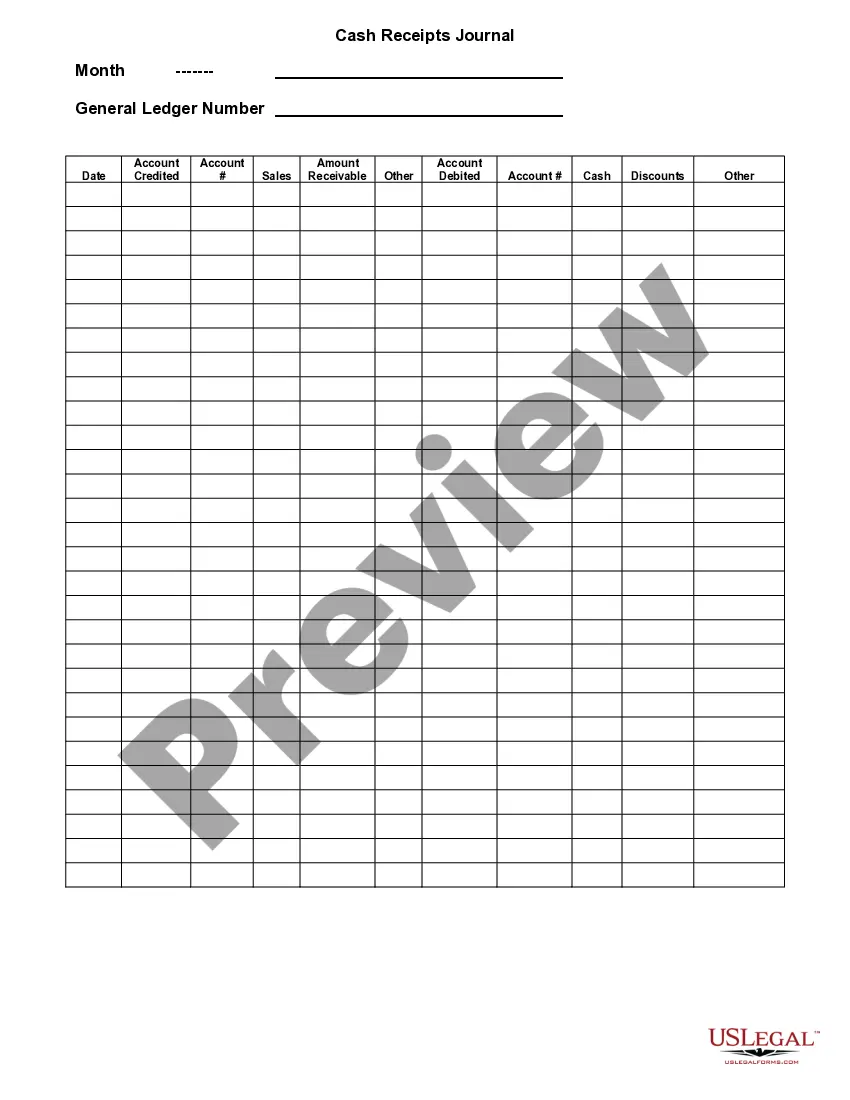

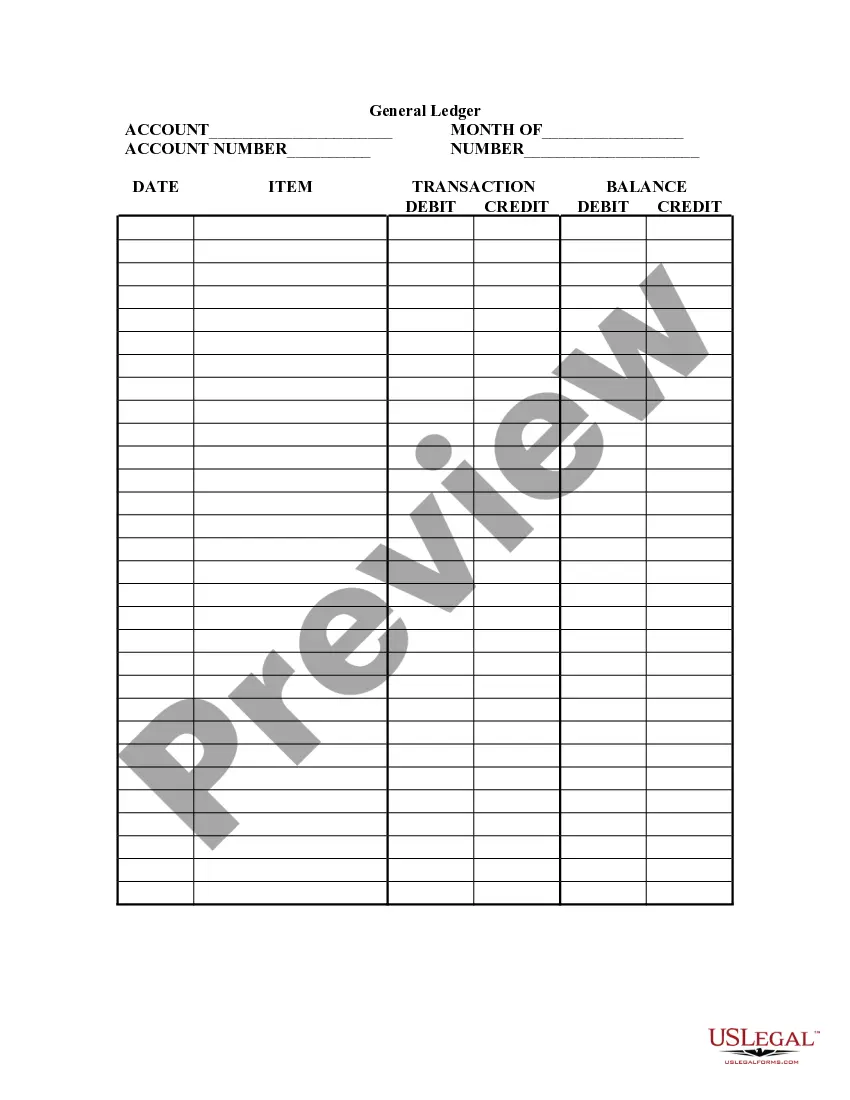

General Journal

What is this form?

The General Journal is a financial form used to record monthly transactions across various accounts. This form provides a standardized method for tracking debits and credits, making it essential for maintaining accurate financial records. Unlike specialized forms tied to specific transaction types, the General Journal serves a broader purpose by accommodating various account entries within a single document.

Form components explained

- Month: Specify the month for the recorded transactions.

- General Ledger Number: Input the unique identifier related to the general ledger.

- Date: Record the date of each transaction.

- Amount Debited: Enter the amount being debited from an account.

- Account Number: Provide the account number associated with the debit.

- Amount Credited: Enter the amount being credited to another account.

- Account Number: Provide the account number linked to the credit.

When to use this form

This form is useful for businesses or individuals who need to document their financial transactions each month. It is particularly applicable when consolidating multiple transactions for various accounts into a comprehensive record. You may also use this form during accounting audits or reviews to ensure accurate financial reporting.

Who should use this form

- Small business owners managing their finances.

- Accountants or bookkeepers maintaining accurate books.

- Individuals tracking personal finances.

- Non-profit organizations documenting their financial activities.

Completing this form step by step

- Start by entering the month for which you are recording transactions.

- Insert the general ledger number relevant to your account system.

- For each transaction, fill in the date when it occurred.

- List the amounts to be debited and credited, making sure they are accurate.

- Provide the corresponding account numbers for both debits and credits.

Notarization guidance

Notarization is not commonly needed for this form. However, certain documents or local rules may make it necessary. Our notarization service, powered by Notarize, allows you to finalize it securely online anytime, day or night.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to enter the correct account numbers.

- Miscalculating totals for debits and credits.

- Not recording all transactions for the month.

- Leaving out the date of the transaction.

Benefits of completing this form online

- Convenient access from anywhere with an internet connection.

- Easy to edit and save multiple versions securely.

- Reliable formatting ensures consistency across records.

Legal use & context

- Provides a structured format for financial accountability.

- Can be used in financial audits to justify transactions made over time.

- Ensures compliance with federal and state financial reporting standards.

Main things to remember

- The General Journal is essential for tracking various financial transactions.

- Accurate completion of this form ensures better financial management.

- Use this form monthly to maintain a comprehensive financial overview.

Looking for another form?

Form popularity

FAQ

Another way to visualize business transactions is to write a general journal entry. Each general journal entry lists the date, the account title(s) to be debited and the corresponding amount(s) followed by the account title(s) to be credited and the corresponding amount(s).

Describe the purpose and structure of a journal entry. Identify the purpose of a journal. Define trial balance and indicate the source of its monetary balances. Prepare journal entries to record the effect of acquiring inventory, paying salary, borrowing money, and selling merchandise.

It is easy to begin sentences with, I feel, or I think, or I wonder. Don't feel pressured to stick to any particular form or topic. The beginning of your journal writing can just be an introduction to your thoughts at the time. This is your personal space, so you should feel comfortable writing.

The accounts into which the debits and credits are to be recorded. The date of the entry. The accounting period in which the journal entry should be recorded. The name of the person recording the entry. Any managerial authorization(s)

Each journal entry includes the date, the amount of the debit and credit, the titles of the accounts being debited and credited (with the title of the credited account being indented), and also a short narration of why the journal entry is being recorded.

Journal entries are how transactions get recorded in your company's books on a daily basis. Every transaction that gets entered into your general ledger starts with a journal entry that includes the date of the transaction, amount, affected accounts, and description.

A journal is a record of transactions listed as they occur that shows the specific accounts affected by the transaction. Used in a double-entry accounting system, journal entries require both a debit and a credit to complete each entry.

The General Journal Entry includes a brief description of the entry, the Account name, amounts, and whether those amounts are recorded in the debit or credit side of accounts. All General Journal Entries must be balanced - that is the total debits must equal the total credits.