Montana Continuation Statement - Corporation

Overview of this form

The Continuation Statement - Corporation is a legal document used to extend the validity of a previously filed Notice of Right to Claim Lien for corporations involved in construction projects. This form allows corporations to maintain their lien rights for an additional year, ensuring they can still make a claim for payment if necessary. The Continuation Statement is essential for protecting a corporationâs financial interests in the construction industry, setting it apart from other lien-related forms which may not address extensions specifically.

Form components explained

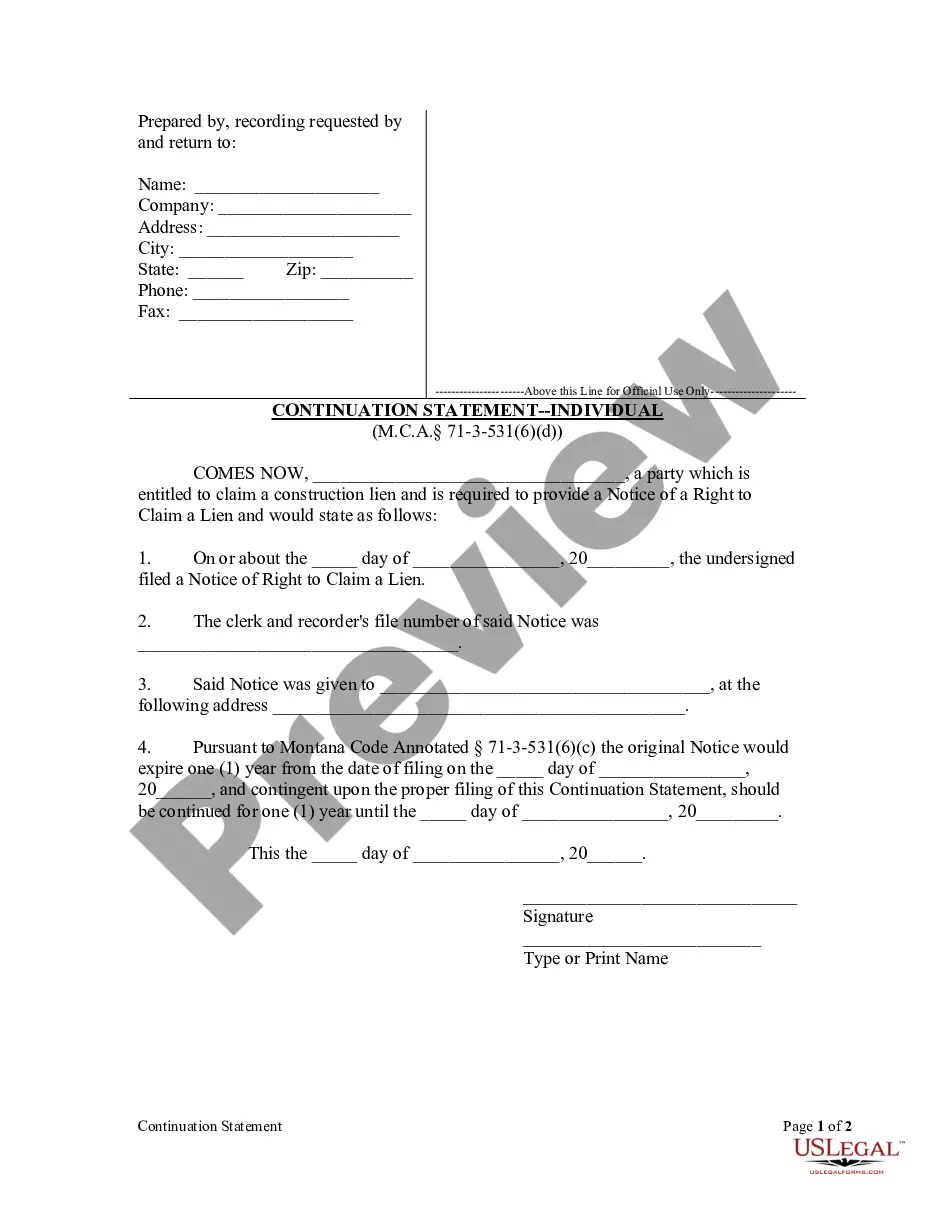

- Identification of the corporation representative and the corporation entitled to claim a lien.

- The date of the original Notice of Right to Claim a Lien filed.

- The file number assigned to the original Notice of Right to Claim a Lien.

- The recipient of the original Notice and their address.

- Confirmation of the expiration date of the original Notice and the new validity period after filing the Continuation Statement.

- Signature of the corporation's representative and acknowledgement by a notary public.

Common use cases

This form should be used when a corporation has filed a Notice of Right to Claim a Lien and wishes to extend it for another year. It is typically required when construction materials or services have been provided and thereâs a need to ensure the right to file a lien remains in effect. It is particularly important if the original Notice is set to expire and the corporation needs additional time to collect payment or resolve outstanding issues.

Who should use this form

This form is intended for:

- Corporations involved in construction or related services that have filed a previous Notice of Right to Claim a Lien.

- Corporate representatives authorized to act on behalf of their organization.

- Businesses that need to secure their financial interests in a construction project.

How to prepare this document

- Identify the representative of the corporation and enter their name along with the corporation's name.

- Fill in the address, city, state, and zip code of the corporation.

- Enter the date when the original Notice of Right to Claim a Lien was filed.

- Provide the file number associated with the original Notice.

- Specify the recipient of the original Notice along with their address.

- Indicate the original expiration date and the new expiration date upon filing this Continuation Statement.

- Sign the form and have it notarized to ensure legal validity.

Does this form need to be notarized?

Yes, this form must be notarized to be legally valid. A notary public will need to verify the identity of the person signing and witness the signing of the Continuation Statement. US Legal Forms offers integrated online notarization, allowing users to complete this process securely from home at any time.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to file the Continuation Statement before the original Notice expires.

- Omitting necessary signatures, including notary acknowledgment.

- Incorrectly entering the dates or file numbers, leading to disputes about validity.

- Not providing complete addresses for involved parties.

Benefits of completing this form online

- Immediate access to a legally vetted template, ensuring compliance with current laws.

- The form can be easily downloaded and customized to fit specific needs.

- Convenient filing, allowing for digital record keeping and faster processing.

Legal use & context

- This form allows corporations to extend their lien rights as provided by Montana law.

- It ensures that the liens remain enforceable in case of payment disputes.

- Failure to file this form in time may jeopardize the corporation's ability to claim a construction lien.

Main things to remember

- The Continuation Statement is essential for extending lien rights in Montana.

- Failing to file on time can result in the loss of valuable legal protections for corporations.

- Proper completion and notarization of this form are necessary for valid lien claims.

Looking for another form?

Form popularity

FAQ

Forming an LLC or a corporation will allow you to take advantage of limited personal liability for business obligations. LLCs are favored by small, owner-managed businesses that want flexibility without a lot of corporate formality. Corporations are a good choice for a business that plans to seek outside investment.

In an LLC, individuals with an ownership share are called members. In a corporation, they are called shareholders. One of the advantages an LLC has over a corporation is that in many states, a creditor cannot collect a member's dividends, whereas in a corporation dividends can be collected from shareholders.

A Limited Liability Company (LLC) is an entity created by state statute. Depending on elections made by the LLC and the number of members, the IRS will treat an LLC either as a corporation, partnership, or as part of the owner's tax return (a disregarded entity).

Both types of entities have the significant legal advantage of helping to protect assets from creditors and providing an extra layer of protection against legal liability. In general, the creation and management of an LLC are much easier and more flexible than that of a corporation.

There's no such thing as a "limited liability corporation." An LLC is a limited liability company. It's not a corporation, and you don't incorporate a business as an LLC. Both register with a state, but an LLC doesn't "incorporate."

To form a Montana corporation, you must file articles of incorporation with the Secretary of State and pay a filing fee, at which point a corporation's existence officially begins. At a minimum, the articles must include the following information: Name of the corporation. Names and addresses of incorporators.

Generally, most entrepreneurs choose to form a Corporation or a Limited Liability Company (LLC). The main difference between an LLC and a corporation is that an llc is owned by one or more individuals, and a corporation is owned by its shareholders.It also provides limited liability protection.

A Limited Liability Company (LLC) is an entity created by state statute. Depending on elections made by the LLC and the number of members, the IRS will treat an LLC either as a corporation, partnership, or as part of the owner's tax return (a disregarded entity).

The main advantage of having an LLC taxed as a corporation is the benefit to the owner of not having to take all of the business income on your personal tax return. You also don't have to pay self-employment tax on your income as an owner from the corporation. The main disadvantage is double taxation.