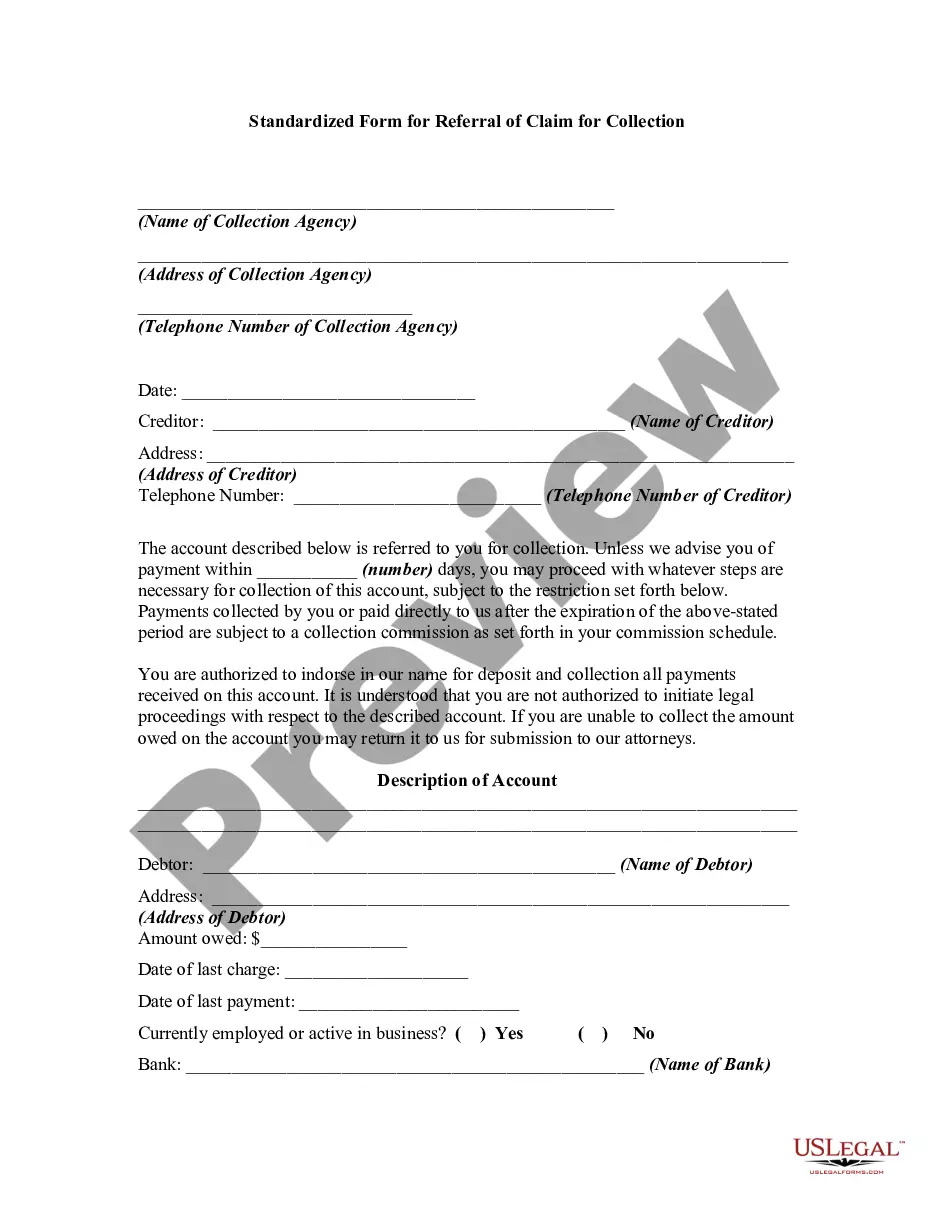

Collection Report

Overview of this form

The Collection Report is a legal document designed to provide details about the status of an unpaid account. It serves as a summary of outstanding debts and outlines recommended actions for the creditor. This form is essential for businesses and individuals managing accounts receivable, as it helps determine the next steps for collecting debts, differing from general invoice forms that do not evaluate credit status or recommend actions.

Key parts of this document

- Date of the report.

- Name and address of the account holder.

- Current account status, indicating how overdue the payment is.

- Total amount owed by the account holder.

- Comments or agreements regarding payment from the account holder.

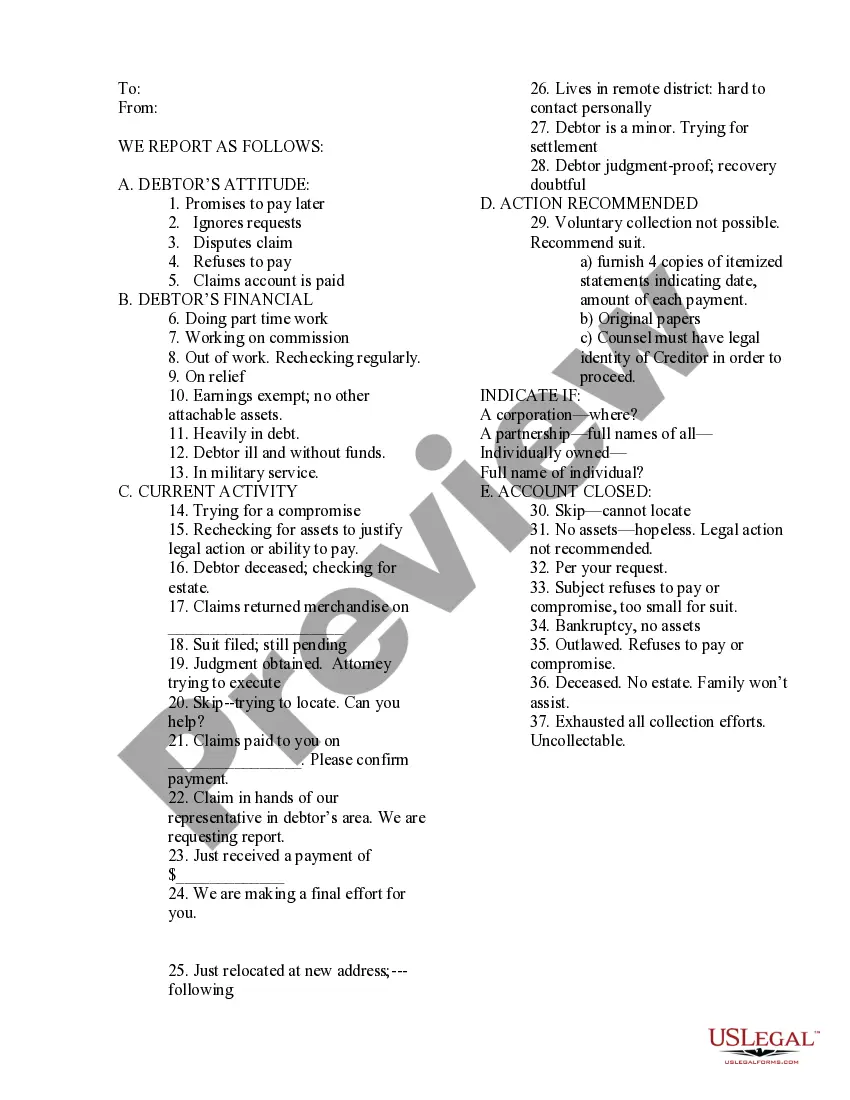

- Recommended actions based on the account status.

When this form is needed

This form should be utilized when a business or individual needs to assess the status of an unpaid account. It is particularly useful when an account becomes overdue and the creditor must decide how to proceed with credit extension or collection efforts.

Who can use this document

This form is intended for:

- Business owners managing accounts receivable.

- Accountants or finance professionals overseeing collections.

- Individuals or organizations that wish to document the status of debts owed to them.

How to complete this form

- Fill in the date of the report.

- Enter the account name and address of the account holder.

- Mark the appropriate box indicating the account status (current, 30 days overdue, etc.).

- Specify the total amount owed by the account holder.

- Provide any comments or agreements regarding the payment from the account holder.

- Select the recommended action to take based on the account status.

Notarization guidance

This form usually doesn’t need to be notarized. However, local laws or specific transactions may require it. Our online notarization service, powered by Notarize, lets you complete it remotely through a secure video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Not updating the account status regularly.

- Failing to collect all necessary information, such as address or total owed.

- Neglecting to document any agreements made with the account holder.

Benefits of completing this form online

- Convenience of immediate access and download.

- Editability ensures that you can customize the report for each account.

- Reliability of using a template created by licensed attorneys.

Main things to remember

- The Collection Report assesses the status of unpaid accounts and suggests actions.

- It is essential for businesses and individuals managing debt collections.

- Completing it accurately aids in informed decision-making about debt recovery.

Looking for another form?

Form popularity

FAQ

To find out what you have in collections, you will need to check your latest credit reports from each of the 3 credit bureaus. Collection agencies are not required to report their account information to all three of the national credit reporting agencies.

Once an account is sold to a collection agency, the collection account can then be reported as a separate account on your credit report. Collection accounts have a significant negative impact on your credit scores. Collections can appear from unsecured accounts, such as credit cards and personal loans.

It's always a good idea to pay collection debts you legitimately owe. Paying or settling collections will end the harassing phone calls and collection letters, and it will prevent the debt collector from suing you.

Unfortunately, a debt in collections is one of the most serious negative items that can appear on credit reports because it means the original creditor has written off the debt completely.Generally, an account in collection will remain on your credit reports for seven years.

If you've neglected to pay off a medical or credit card bill, a collection account may appear on your credit reports. This typically happens when the original company owed writes off your debt as a loss and sells it to a debt collection agency.

If you pay the collection agency directly, the debt is removed from your credit report in six years from the date of payment. If you don't pay, it purges six years from the last activity date, but you may be at risk for wage garnishment.

Debt collectors report accounts to the credit bureaus, a move that can impact your credit score for several months, if not years.The late payments and subsequent charge-off that typically precede a collection account already will have damaged your credit score by the time the collection happens.