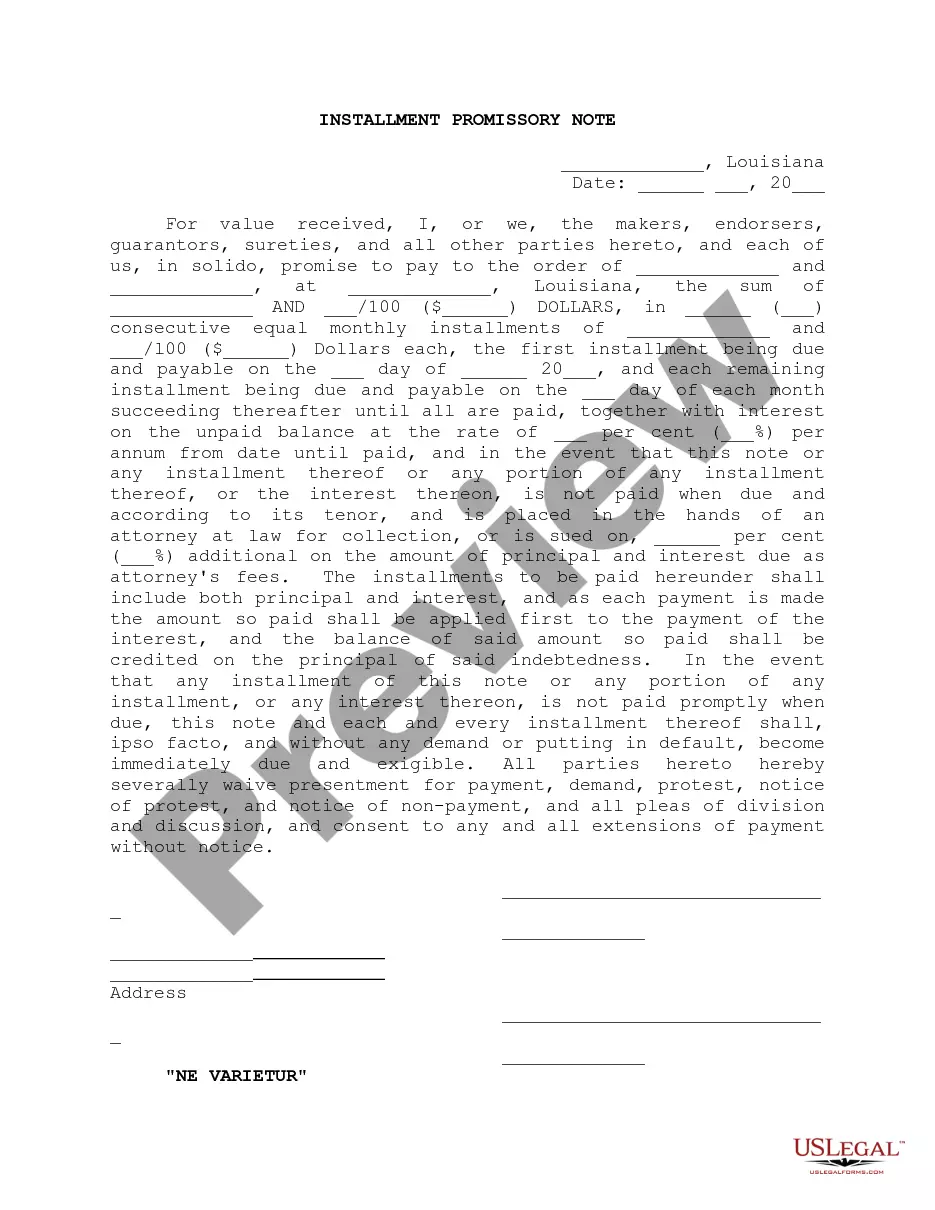

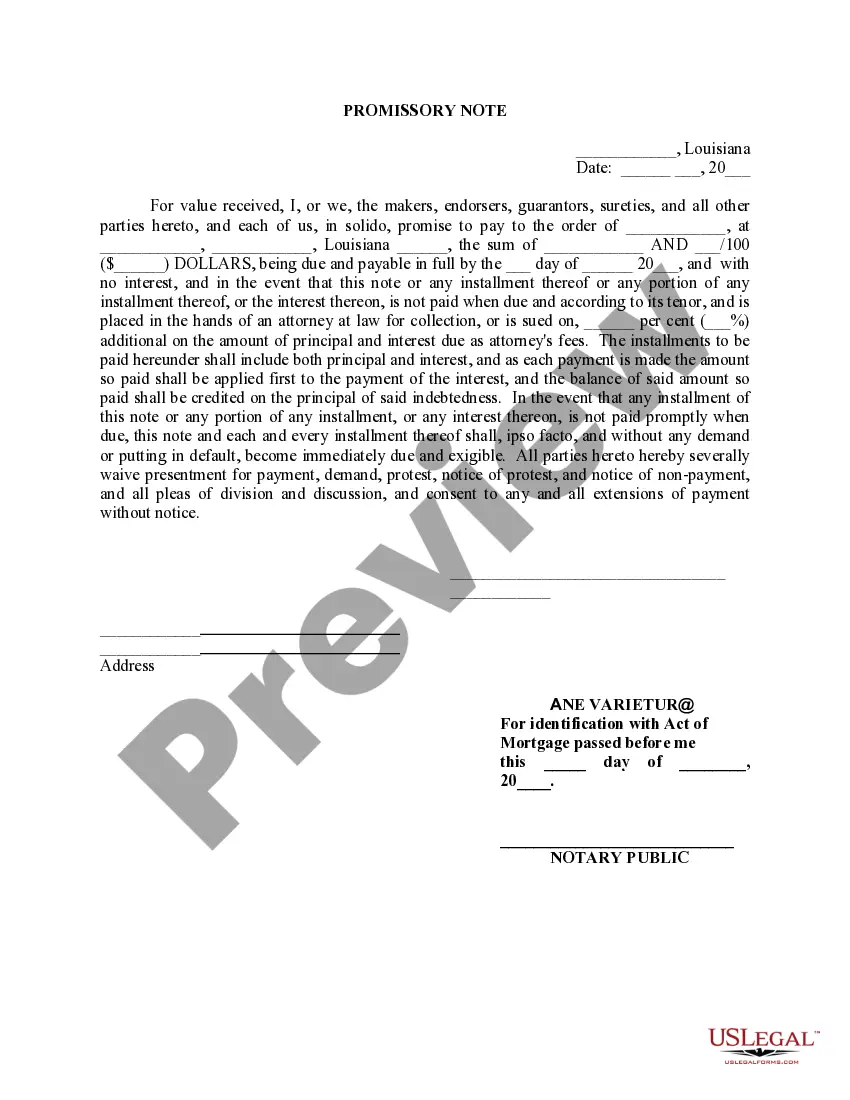

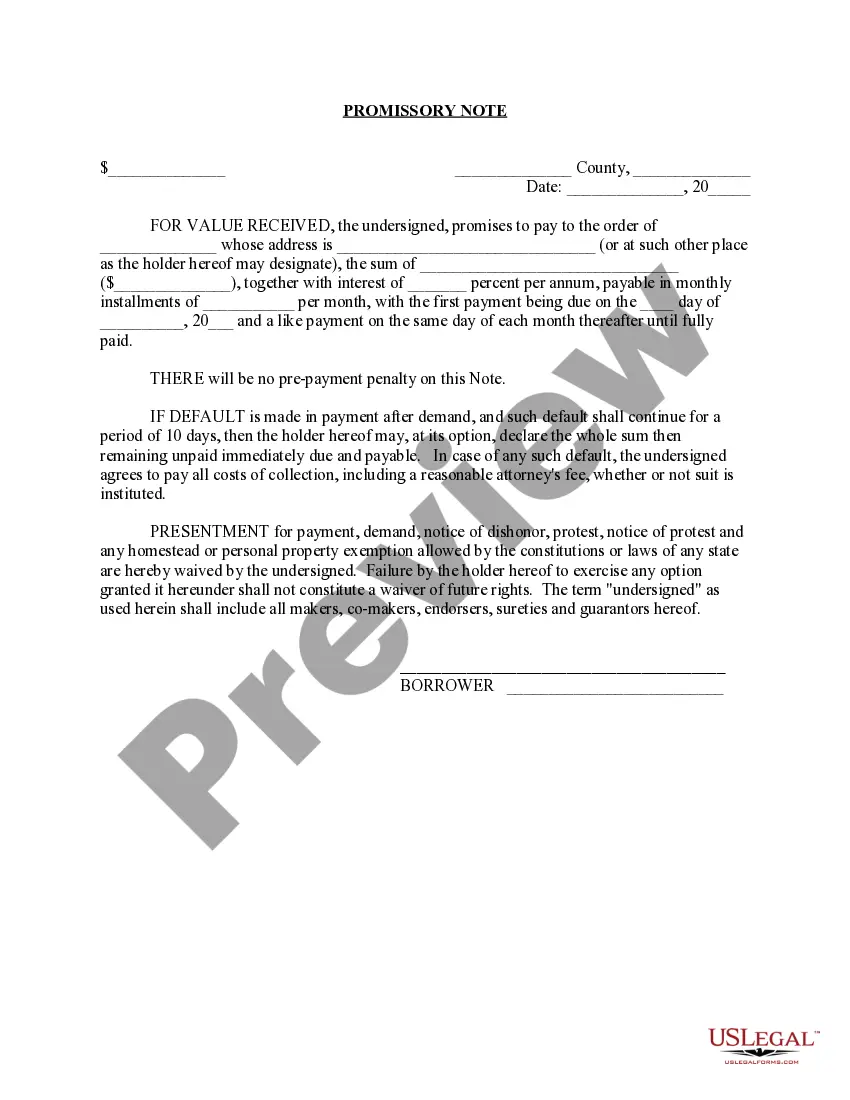

Louisiana Installment Promissory Note Ne Varietur, for Identification with Act of Collateral Mortgage and with Act of Subordination

What this document covers

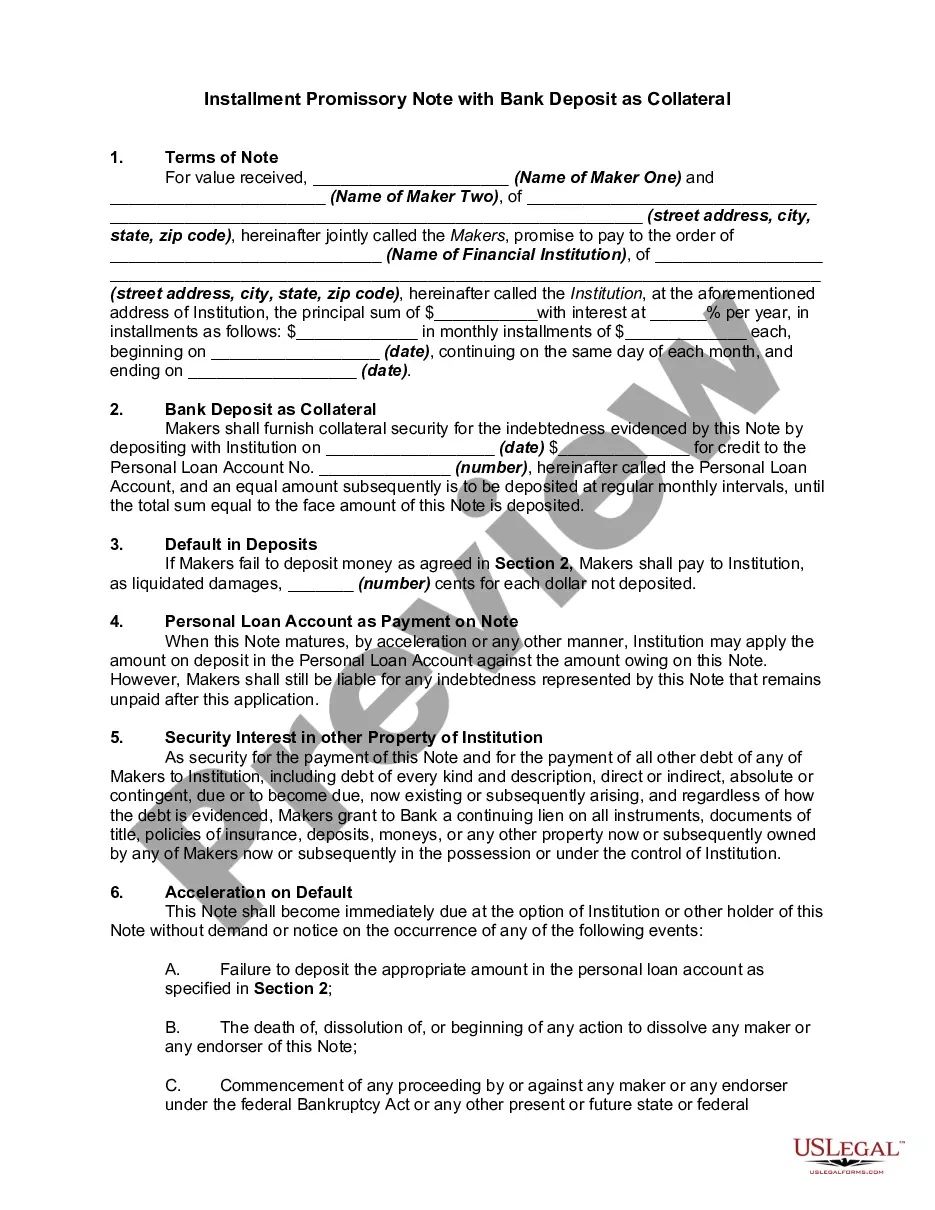

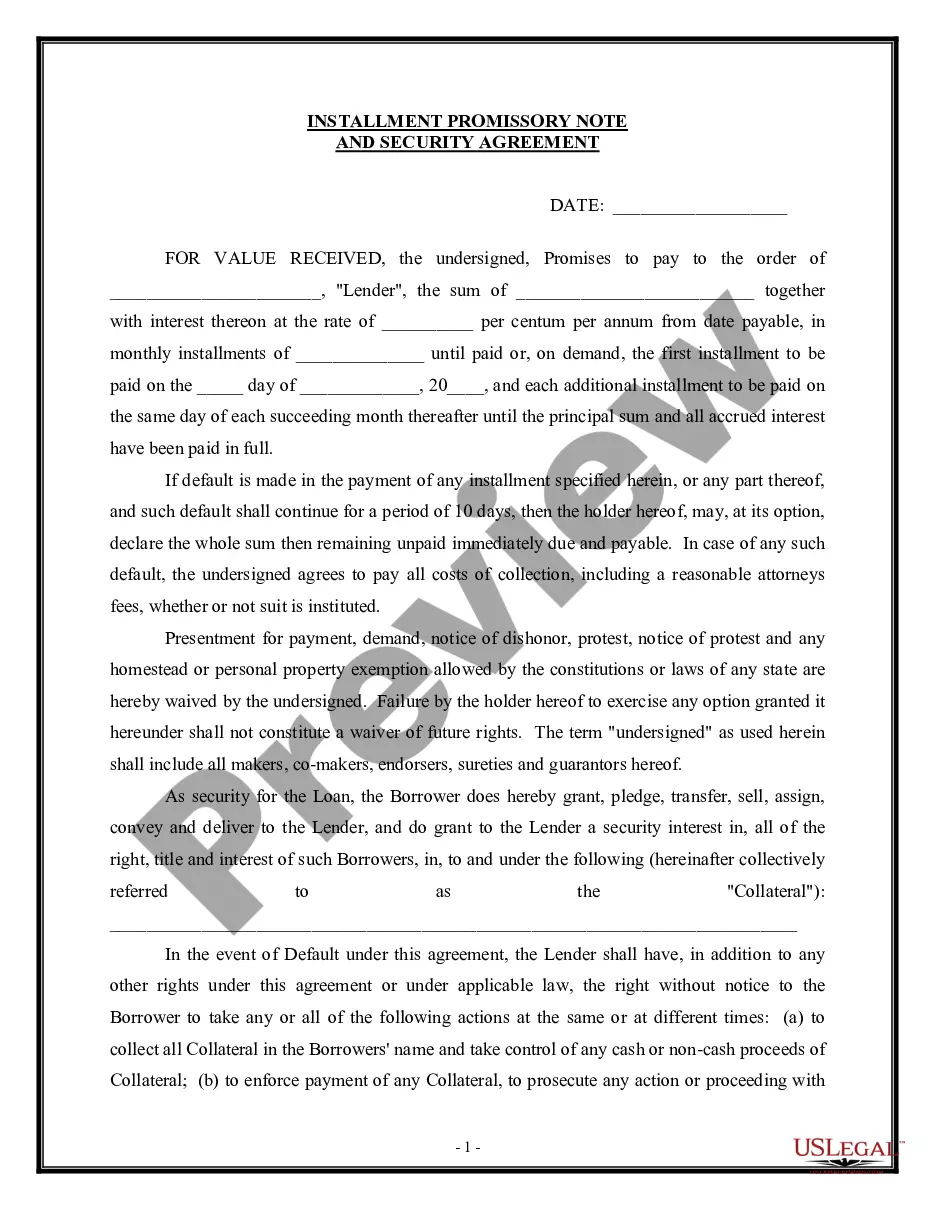

An installment promissory note is a legal document in which a borrower commits to repay a lender in fixed, regular installments over a specified period. This form specifically outlines the terms of a secured loan, which is backed by collateral, making it different from unsecured promissory notes. It is accompanied by an Act of Collateral Mortgage and an Act of Subordination, indicating its serious legal standing and the borrower's obligation to repay the loan under these conditions.

Key parts of this document

- Date of the agreement

- Identification of the borrower and lender

- Loan amount and repayment terms, including installment amounts

- Interest rate and calculations for late payments

- Clauses regarding default and attorney fees

- Notarization fields for legal validation

When to use this document

This form is essential when a borrower needs to secure a loan with property as collateral, particularly in real estate transactions. It should be used when making an agreement for repayment in installments, ensuring both parties understand their obligations. For example, it is suitable for personal loans, mortgages, or any financial arrangement where property is pledged as security.

Who should use this form

This form is intended for:

- Borrowers seeking to obtain a secured loan

- Lenders providing loans that involve collateral

- Individuals involved in real estate transactions requiring a clear repayment structure

- Attorneys advising clients on secured lending agreements

Steps to complete this form

- Enter the date of the agreement at the top of the form.

- Identify the parties involved by entering the names and addresses of the borrower and lender.

- Specify the loan amount and repayment details, including the number of installments and due dates.

- Include the interest rate and detail any attorney fees in case of default.

- Ensure all parties sign the document in the presence of a notary public.

- Check that the notary completes the paraphing process for legal validity.

Is notarization required?

Notarization is required for this form to take effect. Our online notarization service, powered by Notarize, lets you verify and sign documents remotely through an encrypted video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to fill out all fields completely, leading to potential misunderstandings.

- Not specifying the interest rate correctly, which could cause legal disputes.

- Omitting notarization, which may render the document unenforceable in certain situations.

- Leaving out critical details regarding payment default conditions.

Advantages of online completion

- Accessible anytime and anywhere for easy completion and download.

- Editable form allows for customized terms to fit specific needs.

- Reliability of professionally drafted templates ensures legal compliance.

- Instant access to up-to-date legal forms without waiting for physical copies.

Legal use & context

- This form serves as a legally binding agreement for secured loans delineated by state laws.

- The borrower is obligated to repay the lender as per the terms outlined in the promissory note.

- Non-compliance with the payment terms can lead to legal action and the immediate demand for full payment.

Summary of main points

- An installment promissory note is crucial for secured lending agreements.

- Properly filling out and notarizing this form is essential for enforceability.

- This document not only outlines repayment terms but also protects the lender's interests.

- Using a reputable source for the form ensures that it meets legal standards.

Looking for another form?

Form popularity

FAQ

Personal real estate. Home equity. Personal vehicles. Paychecks. Cash or savings accounts. Investment accounts. Paper investments. Fine art, jewelry or collectibles.

Property or assets that are committed by an individual in order to guarantee a loan. Upon default, the collateral becomes subject to seizure by the lender and may be sold to satisfy the debt. EXAMPLE. In securing a mortgage, the borrower may offer the house as collateral.

Collateral is an asset pledged to a lender until a loan is repaid. If the loan isn't repaid, the lender may seize the collateral and sell it to pay off the loan. Obvious forms of collateral include houses, cars, stocks, bonds and cash -- all things that are readily convertible into cash to repay the loan.

These include checking accounts, savings accounts, mortgages, debit cards, credit cards, and personal loans., he may use his car or the title of a piece of property as collateral. If he fails to repay the loan, the collateral may be seized by the bank, based on the two parties' agreement.

The term collateral refers to an asset that a lender accepts as security for a loan.The collateral acts as a form of protection for the lender. That is, if the borrower defaults on their loan payments, the lender can seize the collateral and sell it to recoup some or all of its losses.

These include checking accounts, savings accounts, mortgages, debit cards, credit cards, and personal loans., he may use his car or the title of a piece of property as collateral. If he fails to repay the loan, the collateral may be seized by the bank, based on the two parties' agreement.

The term collateral refers to an asset that a lender accepts as security for a loan.The collateral acts as a form of protection for the lender. That is, if the borrower defaults on their loan payments, the lender can seize the collateral and sell it to recoup some or all of its losses.

Personal loans are typically unsecured, meaning they don't require collateral, but lenders require some personal loans to be backed by something that holds monetary value. Collateral on a secured personal loan can include things like cash in a savings account, a car or even a home.

The term collateral refers to an asset that a lender accepts as security for a loan. Collateral may take the form of real estate or other kinds of assets, depending on the purpose of the loan. The collateral acts as a form of protection for the lender.