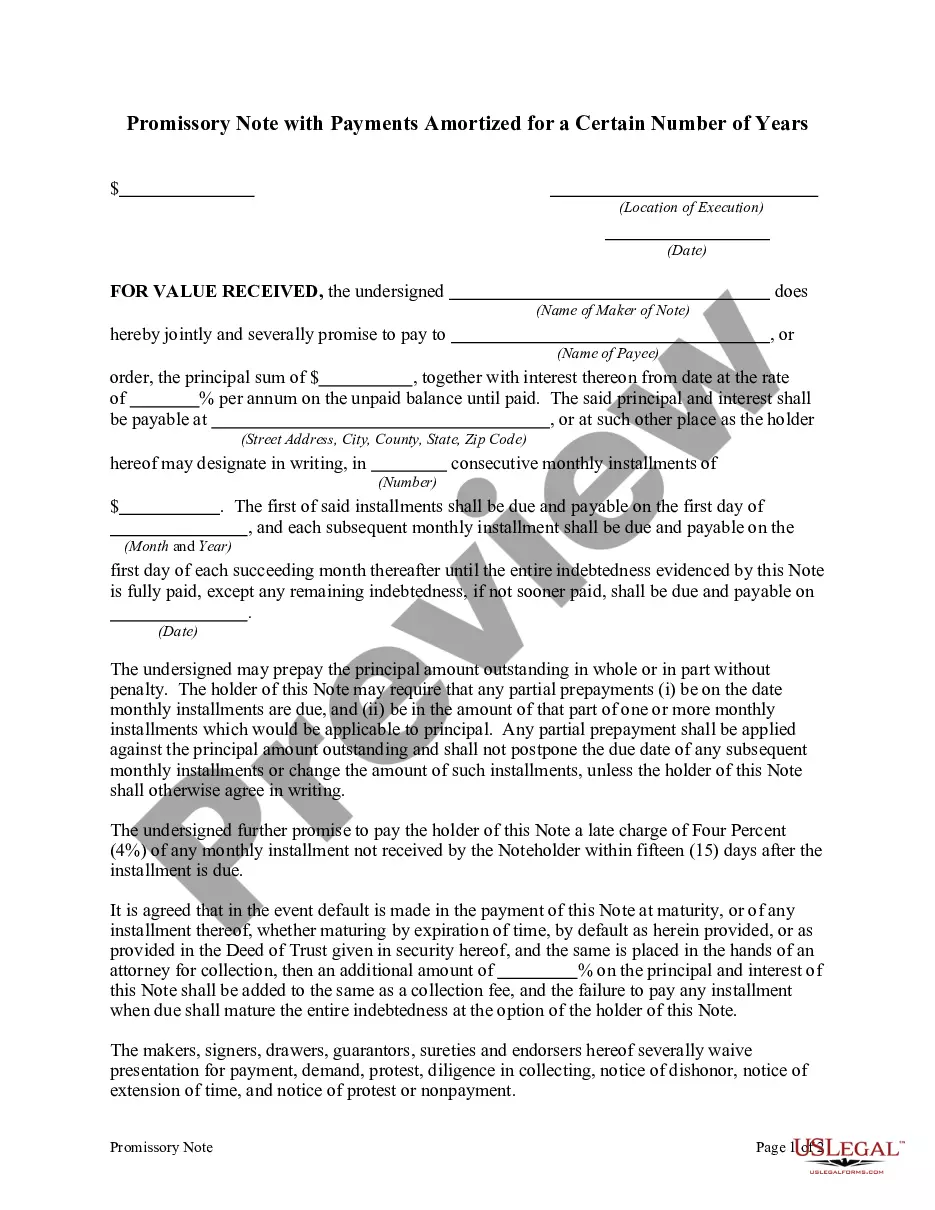

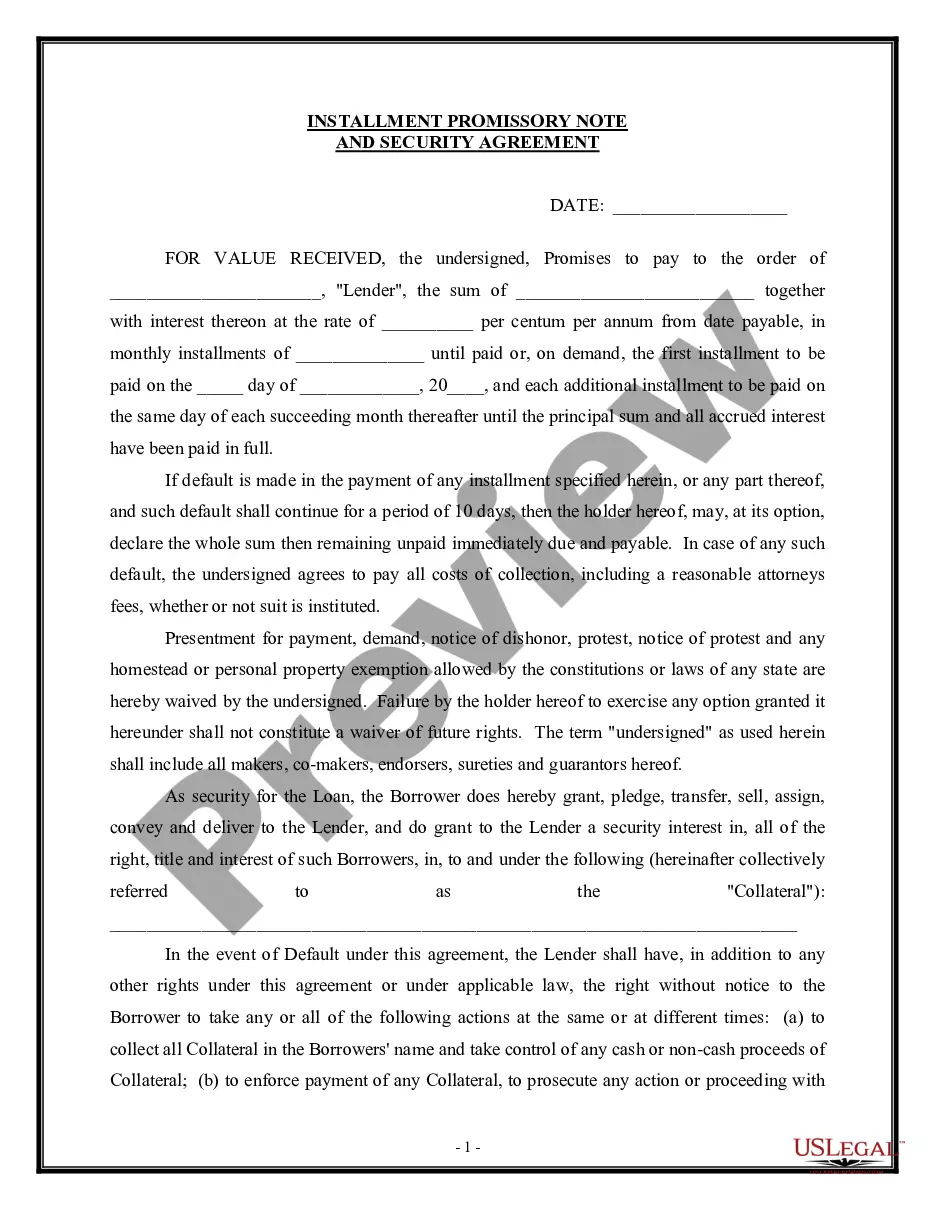

Promissory Note with Installment Payments

What is this form?

This Promissory Note with Installment Payments is a legal document through which a borrower commits to pay a lender a specified amount in monthly installments. Unlike other types of promissory notes, this form specifically outlines that there will be no pre-payment penalty, offering flexibility to the borrower. This form is designed to establish clear terms regarding repayment obligations, interest rates, and default conditions, ensuring protection for both parties involved in the agreement.

Key components of this form

- Identification of the borrower and lender, including their addresses.

- Details of the loan amount and a clear statement regarding the interest rate.

- Specific payment schedule including the amount of monthly installments and due date.

- Clause specifying that there is no pre-payment penalty.

- Default conditions outlining the process if a payment is missed.

- Waivers relating to notice of dishonor and collection costs.

Common use cases

You should use this Promissory Note when you are borrowing money and agree to pay back the amount in monthly installments. This document is suitable for personal loans, business financing, or any situation where a formal agreement on repayment terms is necessary. It provides clarity on payment expectations and protects both parties by clearly defining the terms of the loan.

Who should use this form

This Promissory Note is intended for:

- Individuals borrowing money from friends or family.

- Businesses seeking to formalize loans with other businesses or individuals.

- Lenders who wish to document repayment terms clearly and legally.

Instructions for completing this form

- Identify the borrower and lender by completing their names and addresses.

- Enter the loan amount and the corresponding interest rate.

- Specify the monthly installment amount and due date for payments.

- Review and initial all default and waiver clauses to ensure understanding.

- Both parties should sign and date the form to ensure its execution.

Does this document require notarization?

In most cases, this form does not require notarization. However, some jurisdictions or signing circumstances might. US Legal Forms offers online notarization powered by Notarize, accessible 24/7 for a quick, remote process.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to include the correct loan amount or interest rate.

- Neglecting to specify the payment due date accurately.

- Not both parties signing the document.

- Overlooking any options for default remedies or repayment options.

Why complete this form online

- Convenience: Download the form at any time, from anywhere.

- Editability: Customize the document to fit your specific lending situation.

- Reliability: Get access to legally drafted forms by licensed attorneys.

Legal use & context

- Enforceable as a written loan agreement in most jurisdictions.

- Provides clear documentation in case of legal disputes over payments.

- Effective for personal and business loans, creating a record for both parties.

Summary of main points

- The Promissory Note with Installment Payments is crucial for formalizing loans.

- It helps avoid misunderstandings regarding payment terms by outlining clear agreements.

- Ensure all relevant information is accurately filled out to maintain the form's legality.

Looking for another form?

Form popularity

FAQ

What Happens When a Promissory Note Is Not Paid? Promissory notes are legally binding documents. Someone who fails to repay a loan detailed in a promissory note can lose an asset that secures the loan, such as a home, or face other actions.

Step 1 Agree to Terms. Step 2 Run a Credit Report. Step 3 Security and Co-Signer(s) Step 4 Writing the Promissory Note. Step 5 Paying Back the Borrowed Money. Calculating Total Interest Owed. Calculating the Final Payment Amount. Calculating the Monthly Payment Amount.

Write the date of the writing of the promissory note at the top of the page. Write the amount of the note. Describe the note terms. Write the interest rate. State if the note is secured or unsecured. Include the names of both the lender and the borrower on the note, indicating which person is which.

Writing the Promissory Note Terms You can use a template or create a promissory note online. But before you begin, you'll need to gather some information and make decisions about the way the loan will be structured. First, you'll need the names and addresses of both the lender (or "payee") and the borrower.

Personal Promissory Notes This is a particular loan taken from family or friends. Commercial Here, the note is made when dealing with commercial lenders such as banks. Real Estate This is similar to commercial notes in terms of nonpayment consequences.

Promissory notes are legally binding whether the note is secured by collateral or based only on the promise of repayment. If you lend money to someone who defaults on a promissory note and does not repay, you can legally possess any property that individual promised as collateral.

Keep the original promissory note. Once a lender executes a promissory note, he keeps the original of the promissory note. Accept full payment of the loan. Mark paid in full on the promissory note. Place a signature beside the paid in full notation. Mail the original promissory note to the borrower.

A promissory note includes a specific promise to pay, and the steps required to do so (like the repayment schedule), while an IOU merely acknowledges that a debt exists, and the amount one party owes another.

A Promissory Note with Installment Payments specifies and documents the terms of a loan that will be paid back with consistent, equal, payments.You're a borrower and are agreeing to a loan with installments. You're in the business of loans or manage a loan company.