Split-Dollar Life Insurance

About this form

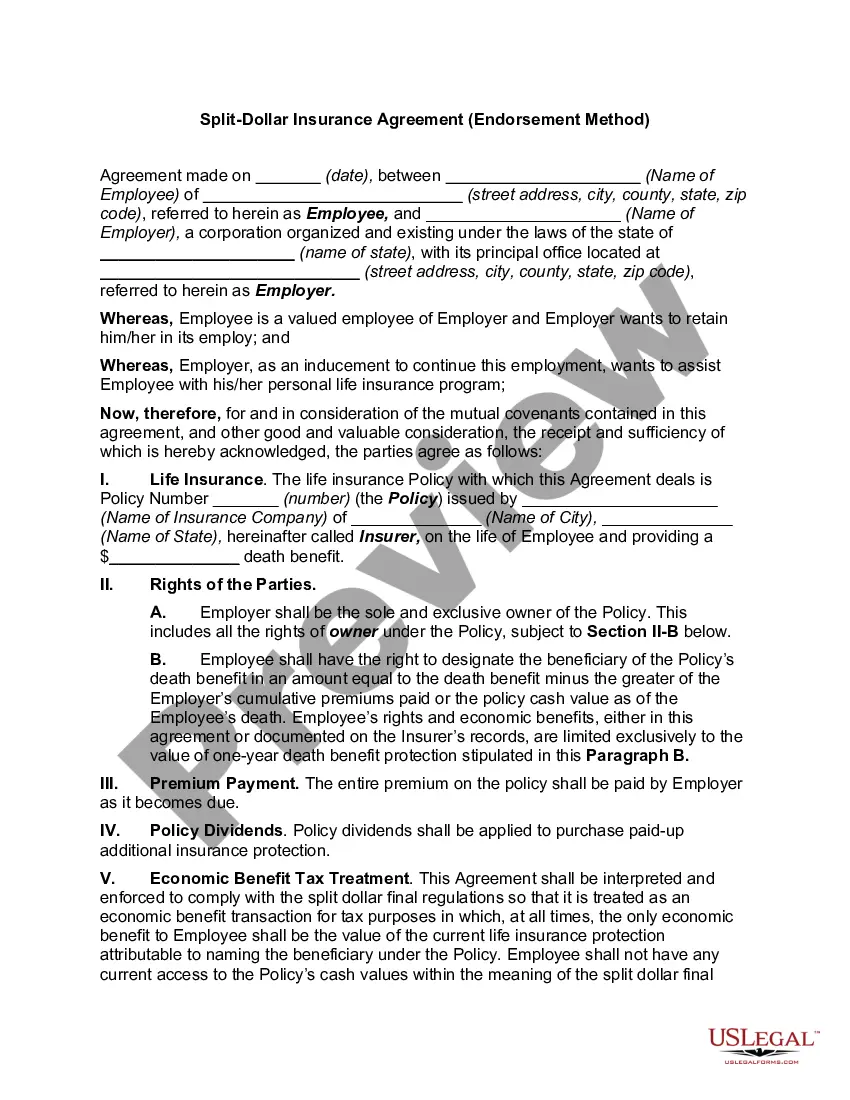

The Split-Dollar Life Insurance form is a legal agreement that outlines the terms under which a corporation provides life insurance benefits to its executive officers. This form details the arrangements for premium payments, insurance policy ownership, and repayment obligations. It serves to ensure that both the corporation and the executive officers clearly understand their roles and responsibilities concerning the life insurance policy, distinguishing it from standard insurance agreements by its corporate structure and loan-like features related to premium advances.

What’s included in this form

- Identification of the corporation and executive officers involved

- Details of premium payments and their loan status

- Insurance policy ownership specifications

- Conditions for repayment of advances upon agreement termination

- Clauses covering policy assignment as collateral

- Termination conditions related to corporate events or changes in status of the executive officers

Common use cases

This form is essential when a corporation decides to implement a split-dollar life insurance plan to provide financial benefits to its executive officers. It is particularly useful in situations where the company wants to subsidize life insurance premiums while ensuring the executives' continued coverage and incentivizing their long-term commitment to the company. It may also be employed during corporate restructuring or succession planning as part of an executive compensation package.

Who should use this form

This form is intended for:

- Corporations looking to offer life insurance benefits to executive officers.

- Human resource managers responsible for executive compensation strategies.

- Legal professionals consulting on compensation agreements in corporate settings.

- Executives participating in a split-dollar life insurance plan.

Steps to complete this form

- Identify the parties involved: Enter the corporation's name and details of the executive officers included in the plan.

- Specify the insurance policies: Outline the details of the life insurance policies provided, including face values and any relevant coverage specifics.

- Detail the premium loan amounts: Fill in the anticipated annual premium amounts that will be provided by the corporation.

- List conditions for repayment: Clearly state the conditions under which the premium advances must be repaid, including specifics around termination events.

- Sign and date the document: Ensure that all parties sign and date the agreement, indicating their acceptance of the terms.

Notarization requirements for this form

Notarization is generally not required for this form. However, certain states or situations might demand it. You can complete notarization online through US Legal Forms, powered by Notarize, using a verified video call available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to include all involved parties' names and roles.

- Overlooking specific repayment conditions, leading to misunderstandings.

- Not reviewing state-specific laws that could impact the agreement.

- Incomplete signatures or dating of the form by all parties involved.

Benefits of completing this form online

- Convenient access to a professionally drafted legal document.

- Ability to edit and customize the form according to specific corporate needs.

- Reliable compliance with legal standards provided by licensed attorneys.

- Instant downloads allow for quick implementation of the plan.

Legal use & context

- This form establishes a legally binding agreement between the corporation and its executive officers.

- It is enforceable in a court of law, provided that it adheres to both federal and state regulations.

- Proper execution and adherence to the terms are crucial to avoid complications related to repayment and tax implications.

Looking for another form?

Form popularity

FAQ

The endorsement split dollar plan is one that is owned by the employer. The premiums are paid by the employer and the beneficiary is listed as the employee.

In a split-dollar plan, an employer and employee execute a written agreement that outlines how they will share the premium cost, cash value, and death benefit of a permanent life insurance policy.Split-dollar plans also require record-keeping and annual tax reporting.

A split-dollar policy is not an insurance policy but refers to a contract between the parties that sets out their duties to split the costs and their rights to share in the proceeds of an insurance policy.

What is Employer Provided Life insurance? Employer provided life insurance is an arrangement where, the employer buys the life insurance plan and pays the premium for the benefit of the employee.Furthermore, the life insurance proceeds to the employee are tax free u/s 10(10D).

Under a collateral assignment split dollar arrangement, the business loans a key employee money to pay the premium on a life insurance policy.He or she owns the policy and has the ability to name the beneficiary, and is taxed on the interest-free element of the loan.

In a split-dollar plan, an employer and employee execute a written agreement that outlines how they will share the premium cost, cash value, and death benefit of a permanent life insurance policy.Generally, the owner of the policy, with some exceptions, is also the owner for tax purposes.

Funding a split dollar plan is a way to reward a key employee while accruing cash value in a whole life insurance policy that can serve as a ready source of funding for the employer. This funding can be used for a future buyout or even a deferred compensation plan.