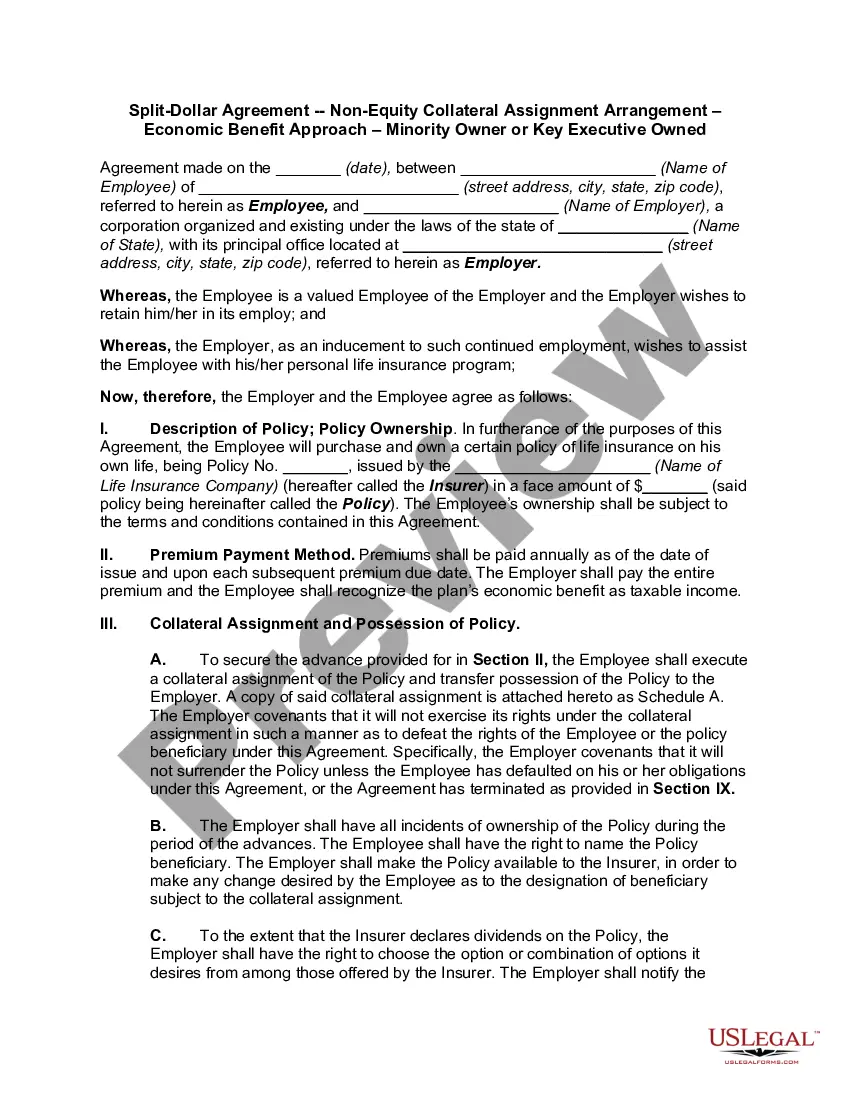

Split-Dollar Insurance Agreement (Endorsement Method)

Understanding this form

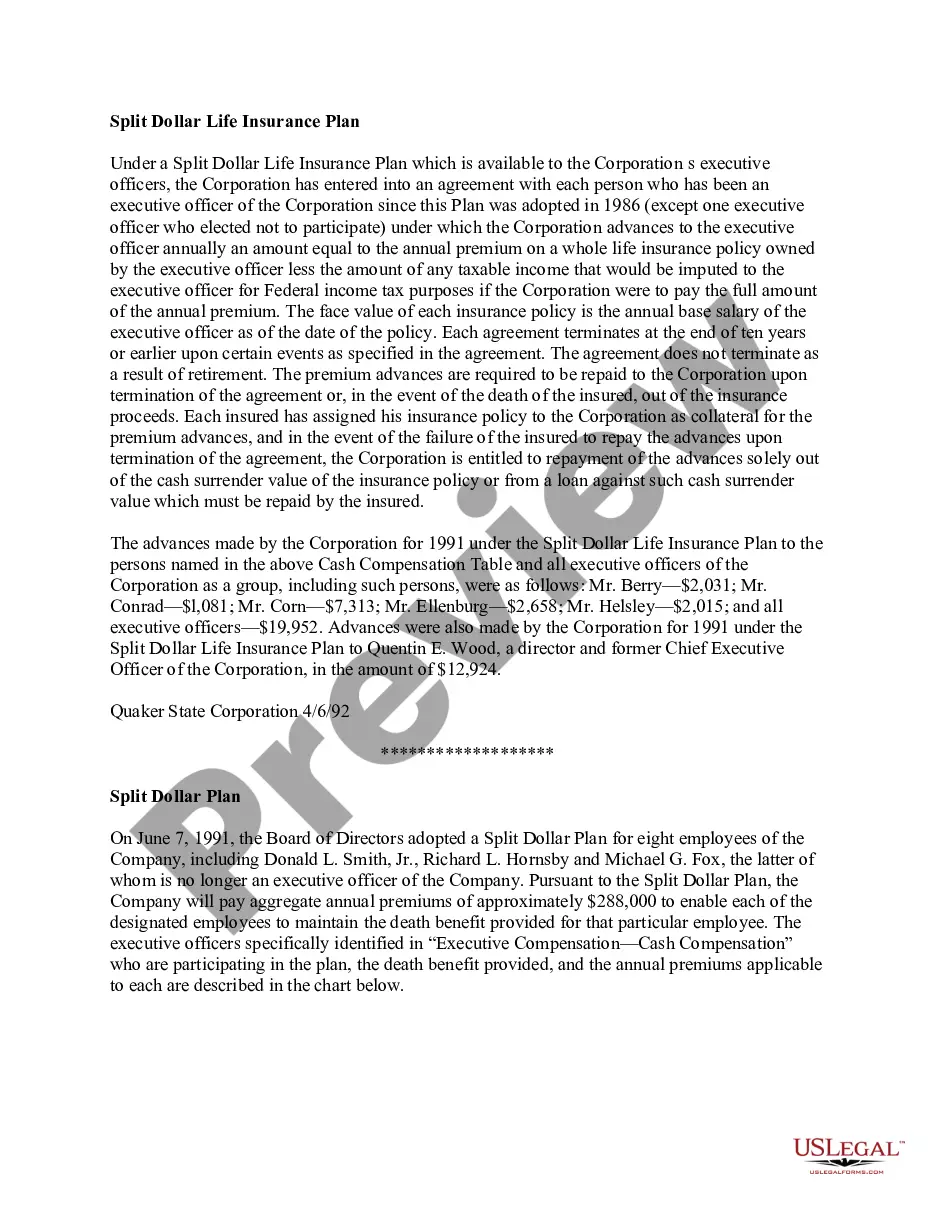

The Split-Dollar Insurance Agreement (Endorsement Method) is a legal document designed to formalize a split-dollar life insurance arrangement between an employer and an employee. In this type of agreement, the employer pays the premiums on a life insurance policy that covers the employee's life. The purpose of this form is to outline the rights and responsibilities of both parties regarding the ownership and benefits of the policy, differentiating it from other insurance arrangements.

Key parts of this document

- Date of the agreement and parties involved (employee and employer)

- Details of the life insurance policy, including the policy number and insurer

- Rights of the parties regarding policy ownership and beneficiary designations

- Premium payment obligations of the employer

- Provisions for terminating the agreement and purchasing the policy

- Compliance with ERISA regulations for employee benefits

")

")

")

")

")

Situations where this form applies

This form should be used when an employer wants to provide a life insurance benefit as part of an employee's compensation package. It is particularly useful in scenarios where the employer is willing to pay the premiums to ensure the employee has coverage, making it an attractive incentive for retaining valuable staff. Additionally, this agreement helps clarify the terms and conditions of the insurance benefits provided.

Who this form is for

- Employers looking to offer life insurance benefits to key employees

- Employees who wish to secure life insurance funded by their employer

- Human resources professionals and legal advisers involved in employee benefits planning

How to prepare this document

- Enter the date of the agreement.

- Fill in the names and addresses of the employee and employer.

- Specify the life insurance policy details, including the policy number and insurer.

- Include any specific terms regarding premium payments and rights to the policy.

- Both parties should sign and date the agreement to finalize it.

Is notarization required?

This form does not typically require notarization to be legally valid. However, some jurisdictions or document types may still require it. US Legal Forms provides secure online notarization powered by Notarize, available 24/7 for added convenience.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to provide accurate information about the life insurance policy.

- Leaving sections of the form blank, such as parties' names or policy details.

- Not including all necessary signatures, which can invalidate the agreement.

Benefits of completing this form online

- Immediate access to the document, allowing for faster completion.

- Editable templates ensure that all necessary sections are properly filled out.

- A reliable tool that simplifies the creation of legally binding agreements.

Looking for another form?

Form popularity

FAQ

A. Employers are responsible for making split-dollar life insurance premiums, regardless of the plan's type. However, it is important to note that under loan arrangements, employees must repay the premiums via collateral assignments made to their employer.

dollar life insurance agreement (or ?splitdollar plan?) is a strategy generally used as an employer benefit or for estate planning involving life insurance. It's an agreement between two or more parties to share the ownership, costs, and benefits of a permanent life insurance policy, like whole life.

Split dollar life insurance funding is a technique in which a funding party, typically the grantor of an ILIT or an entity in which the grantor has an ownership interest, advances money to pay premiums in return for a promise by the trust to repay the advanced premiums upon the occurrence of certain triggering events,

The person who pays for the premiums is based on the type whether it is an endorsement or a collateral assignment. With the endorsement policies the premiums are paid by the employer. In the collateral assignment policies the premiums are paid by the employee by way of loans from the employer.

An endorsement, also known as a rider, adds, deletes, excludes or changes insurance coverage. An endorsement/rider can also be used to increase standard limits of coverage and take precedent over the original agreement or policy.

dollar life insurance agreement (or ?splitdollar plan?) is a strategy generally used as an employer benefit or for estate planning involving life insurance. It's an agreement between two or more parties to share the ownership, costs, and benefits of a permanent life insurance policy, like whole life.

There are 2 types of split dollar plans. Collateral assignment / loan regime. Endorsement split dollar / economic benefit regime.

Disadvantages of split dollar life insurance plans Your business will generally receive no tax deduction for its share of premium payments under the split dollar plan. Depending on how the agreement is structured, employees may have to pay income taxes each year on the value of the economic benefits provided to them.