Living Trust - Irrevocable

What this document covers

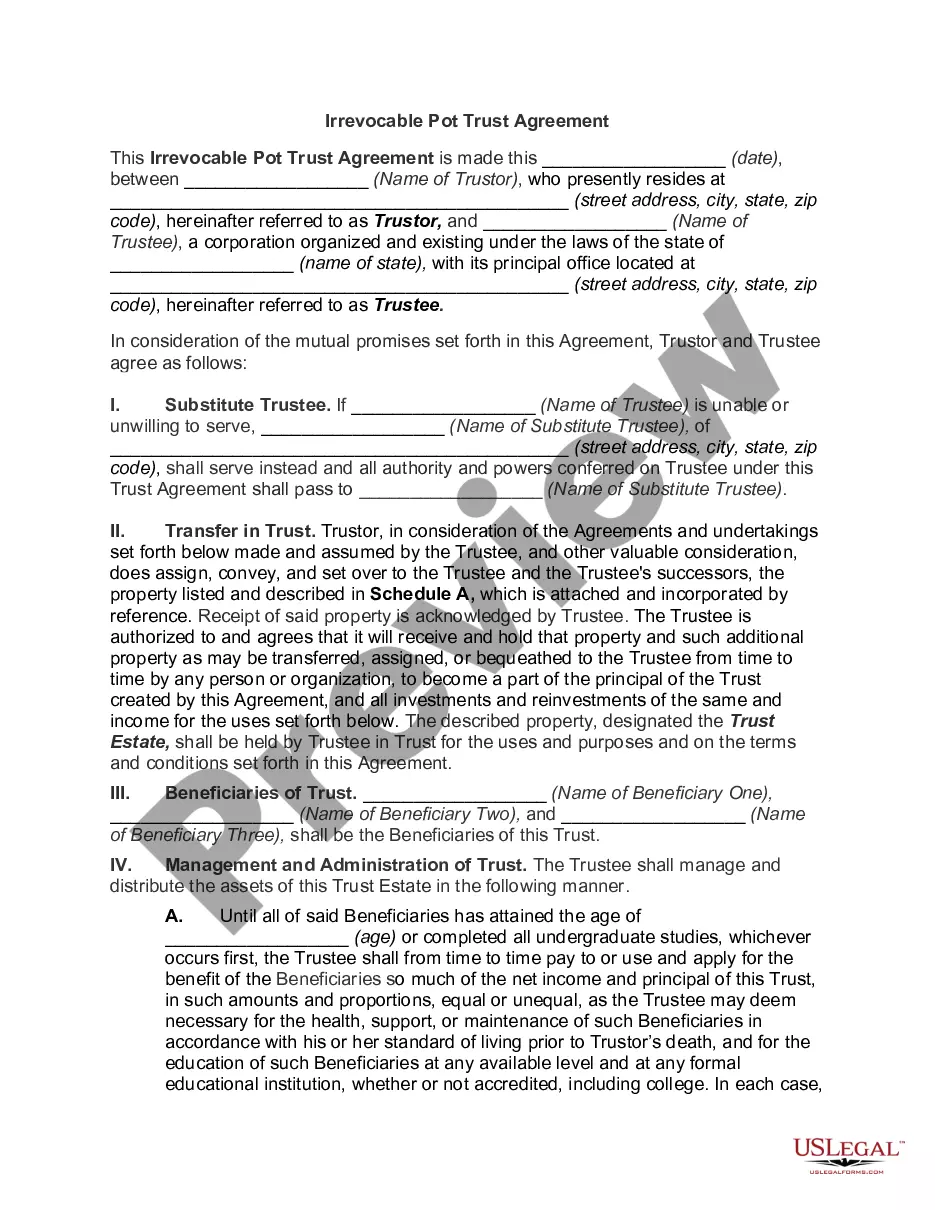

This irrevocable living trust form is a legal document that establishes an agreement between the trustor and the trustee to manage and distribute the trustor's assets upon their incapacity or death. Unlike revocable trusts, an irrevocable trust cannot be modified or terminated once established, making it a more permanent arrangement for estate planning. This type of trust helps avoid probate and can offer tax benefits while providing clear instructions for asset distribution to named beneficiaries.

Main sections of this form

- Trustor and trustee identification

- Purpose and management of trust assets

- Detailed list of transferred property

- Provisions for incapacity and disability

- Distribution instructions upon the trustor's death

When to use this form

This form is essential when an individual wishes to create a durable estate plan that cannot be altered, ensuring that their assets are managed according to their preferences after their incapacity or upon death. It is particularly useful for those looking to protect their assets from creditors or reduce estate taxes.

Intended users of this form

This form is intended for:

- Individuals wanting to establish a permanent trust for asset management.

- Those seeking to avoid probate and simplify the transfer of assets after death.

- People who want to minimize estate taxes or protect assets from creditors.

Completing this form step by step

- Identify the involved parties, including the trustor, trustee, beneficiaries, and successor trustee.

- Clearly describe the assets being transferred into the trust.

- Enter the relevant dates and signatures from all parties involved.

- Attach any necessary schedules detailing specific property or assets.

- Consider having the document reviewed by a legal advisor for accuracy and compliance.

Notarization requirements for this form

This form does not typically require notarization unless specified by local law. However, having a notary public witness the signing can enhance the validity of the trust document and help avoid any future disputes.

Common mistakes

- Failing to list all assets intended for trust transfer.

- Not naming a successor trustee or beneficiary clearly.

- Overlooking necessary signatures or dates.

- Assuming state-specific regulations do not apply.

Why use this form online

- Easy access to downloadable templates tailored to your needs.

- Convenience of filling out forms from the comfort of home.

- Instant updates to reflect changes in state regulations.

Legal use & context

- The irrevocable living trust is a legally binding document that provides clear directives for asset management and distribution.

- It can prevent complications or disputes among beneficiaries regarding asset division after the trustor's passing.

- This form helps protect assets from creditors and may have tax advantages.

- An irrevocable living trust is a binding agreement that cannot be altered after its creation.

- This form is essential for protecting assets and providing clear directives for asset distribution after death.

- It is beneficial for estate tax planning and asset management without court intervention.

Form popularity

FAQ

An irrevocable trust is a type of trust where its terms cannot be modified, amended or terminated without the permission of the grantor's named beneficiary or beneficiaries.Irrevocable trusts cannot be modified after they are created, or at least they are very difficult to modify.

The main downside to an irrevocable trust is simple: It's not revocable or changeable. You no longer own the assets you've placed into the trust. In other words, if you place a million dollars in an irrevocable trust for your child and want to change your mind a few years later, you're out of luck.

If this is how you feel, then you should set up a living irrevocable trust fund. This type of trust can be set up to begin dispersing funds when certain conditions are met. There is no stipulation that you cannot be alive when that happens. You can place cash, stock, real estate, or other valuable assets in your trust.

An irrevocable trust has a grantor, a trustee, and a beneficiary or beneficiaries. Once the grantor places an asset in an irrevocable trust, it is a gift to the trust and the grantor cannot revoke it.To gift assets the estate while still retaining the income from the assets.

Plan the purpose and scope of the irrevocable trust. Choose a trustee. Prepare an irrevocable trust agreement. Obtain a taxpayer identification number for the trust from the Internal Revenue Service.

For a simple irrevocable trust, you could expect to pay $900 on the low end for legal fees. For more complicated trusts, you can expect to pay as much as $3,500 to an estate planning attorney.

Irrevocable trusts require a legally enforceable trust agreement.Once the trust agreement is ready for signature, the parties must sign in the presence of witnesses and the document should be notarized.