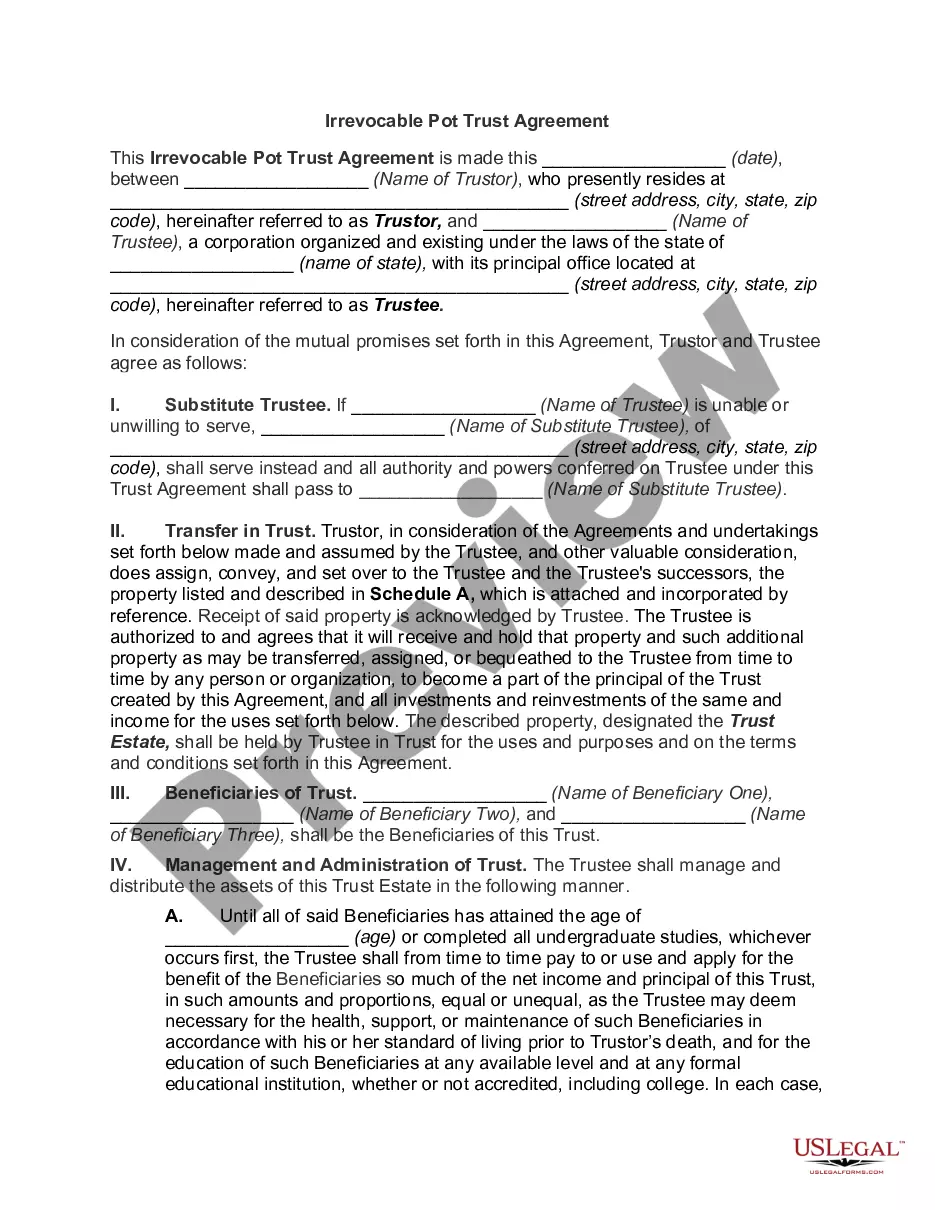

Trust Agreement - Irrevocable

What this document covers

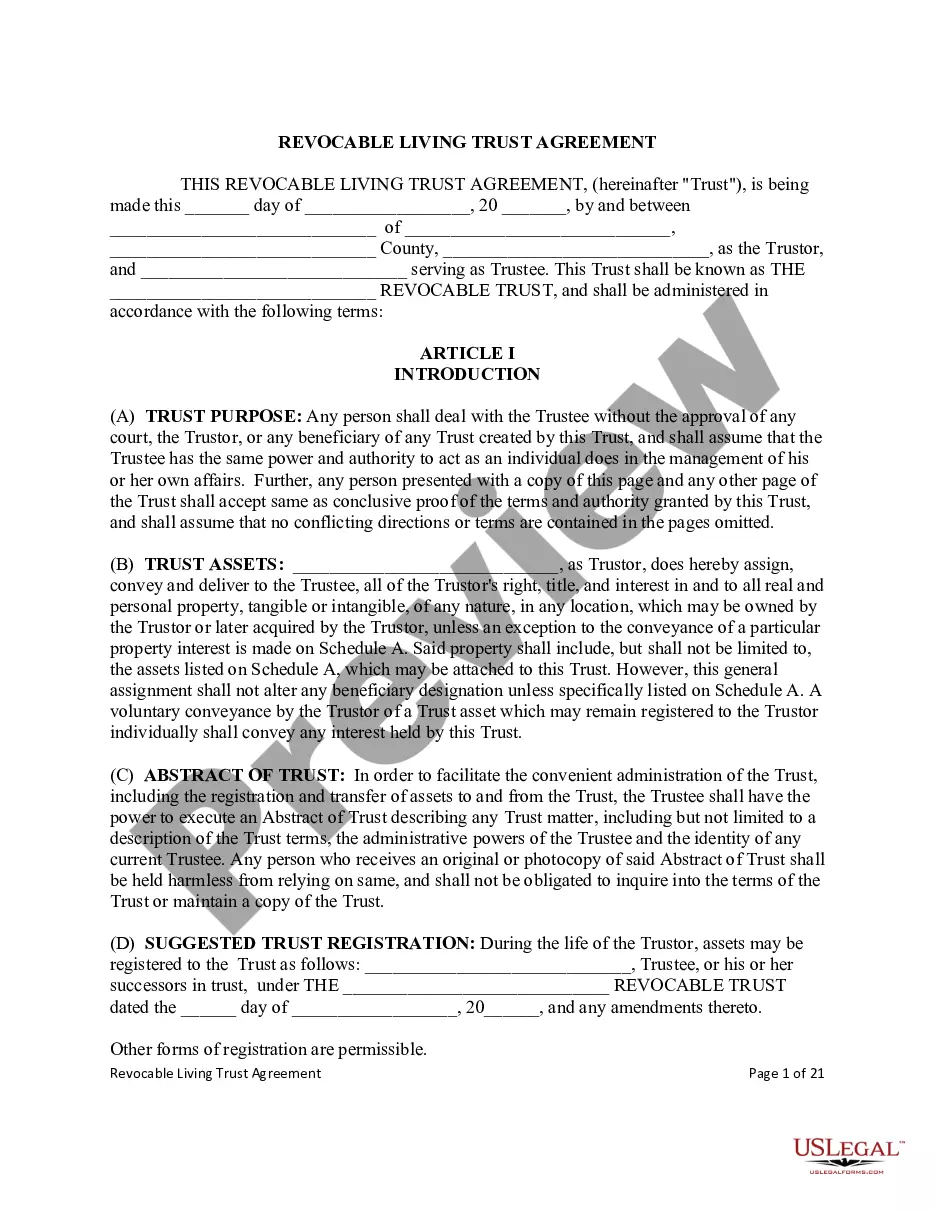

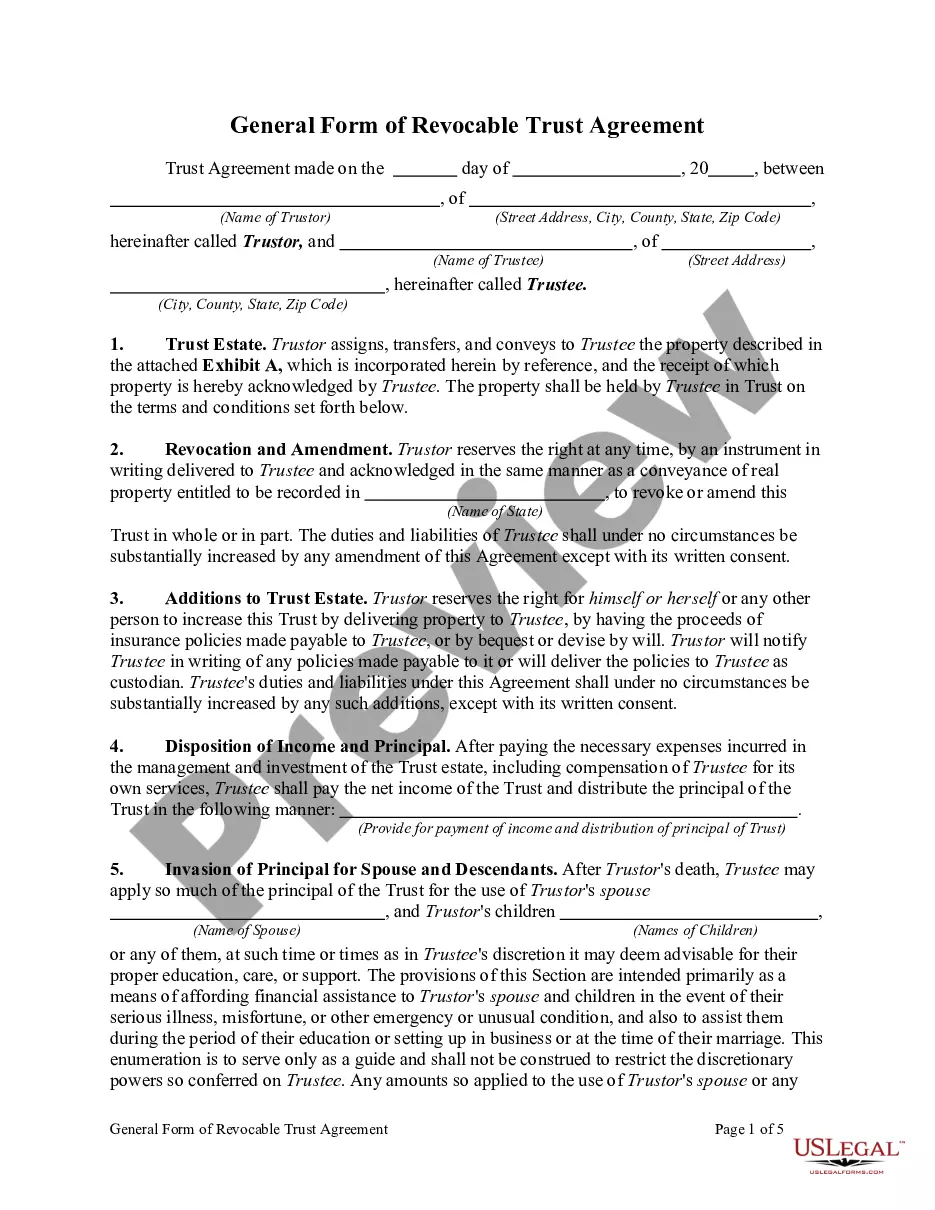

The Irrevocable Trust Agreement is a legal document that establishes an irrevocable trust between the grantor and trustees. This agreement outlines how the trust's assets will be managed and distributed for the benefit of the grantor's spouse and children. Unlike revocable trusts, an irrevocable trust cannot be altered or terminated by the grantor once executed, providing greater security for beneficiaries and potential tax benefits.

What’s included in this form

- Identification of the grantor and trustees.

- Details regarding the trust property and how it is to be managed.

- Provisions for the distribution of income and principal to beneficiaries.

- Criteria for the advancement of funds to beneficiaries for education, housing, or business purposes.

- Instructions for the trust's administration and powers of trustees.

When to use this form

This form is typically used in situations where an individual wants to create a trust to benefit their spouse and children while also achieving potential tax benefits and asset protection. It is useful for individuals who wish to provide specific instructions for managing their assets and ensuring their distribution upon their death or incapacitation.

Who this form is for

- Individuals seeking to manage their estate and provide for their family's future financial needs.

- Those looking to protect their family assets from creditors and ensure they are used in specific ways.

- People who want to establish a clear plan for their trust assets after their passing.

How to prepare this document

- Identify the grantor and trustees by entering their full names and addresses.

- List the property being transferred into the trust, as detailed in Schedule A.

- Specify the beneficiaries, including the grantor's spouse and children, as well as any conditions for their benefits.

- Provide detail on any distributions from the trust, including conditions for principal or income access.

- Have the necessary parties sign the agreement in the presence of a notary public, if required.

Notarization guidance

Notarization is required for this form to take effect. Our online notarization service, powered by Notarize, lets you verify and sign documents remotely through an encrypted video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to clearly outline the trust property or beneficiaries.

- Not obtaining the necessary notarizations or witness signatures.

- Ignoring specific state laws related to irrevocable trusts.

Why complete this form online

- Convenience of accessing and completing the form from home.

- Editable templates that allow for personalization based on individual needs.

- Reliable resources and support available during the completion process.

Quick recap

- An irrevocable trust cannot be altered or revoked, providing certainty in asset distribution.

- This form is essential for protecting family assets and ensuring financial support for dependents.

- Proper execution, including notarization, is crucial for the trust's legality.

- Understanding the specific provisions and conditions is vital for both grantors and beneficiaries.

Looking for another form?

Form popularity

FAQ

A will and a trust are separate legal documents that typically share a common goal of facilitating a unified estate plan.Since revocable trusts become operative before the will takes effect at death, the trust takes precedence over the will, when there are discrepancies between the two.

After death, the sum of money equal to the estate tax exemption in the year that they die is put in an irrevocable trust called the bypass trust, or B trust. This trust is also known as the decedent's trust.The estate tax on the A trust is deferred until after the death of the surviving spouse.

When you transfer your assets into an irrevocable trust, you relinquish control of them. The trust is now the owner of the assets, which you'll retitle or register in the trust's name. The assets are no longer yours, and have no bearing on your wealth, the value of your estate, or your tax liability .

A testamentary trust is revocable during the testator's lifetime because it doesn't actually exist yet. It won't come into being until after death.The trust becomes irrevocable when the grantor dies and is no longer able to change the terms of the will.

The main downside to an irrevocable trust is simple: It's not revocable or changeable. You no longer own the assets you've placed into the trust. In other words, if you place a million dollars in an irrevocable trust for your child and want to change your mind a few years later, you're out of luck.

An irrevocable trust is a type of trust where its terms cannot be modified, amended or terminated without the permission of the grantor's named beneficiary or beneficiaries.Irrevocable trusts cannot be modified after they are created, or at least they are very difficult to modify.

The main reasons for setting up an irrevocable trust are for estate and tax considerations. The benefit of this type of trust for estate assets is that it removes all incidents of ownership, effectively removing the trust's assets from the grantor's taxable estate.

A will covers any property that is only in your name when you die. It does not cover property held in joint tenancy or in a trust. A trust, on the other hand, covers only property that has been transferred to the trust.Another difference between a will and a trust is that a will passes through probate.

There are no conditions or reservations of power in Grantor to free any or all of the property constituting said Trust estate from the terms of this Trust.