Profit and Loss Statement

What is this form?

The Profit and Loss Statement is a financial document that summarizes the revenues, costs, and expenses incurred during a specified period for a business. Its primary purpose is to provide insight into the company's profitability and operational efficiency. Unlike balance sheets that depict financial position at a specific point in time, the Profit and Loss Statement gives a dynamic view of financial performance over time, making it an essential tool for business owners and stakeholders alike.

Key parts of this document

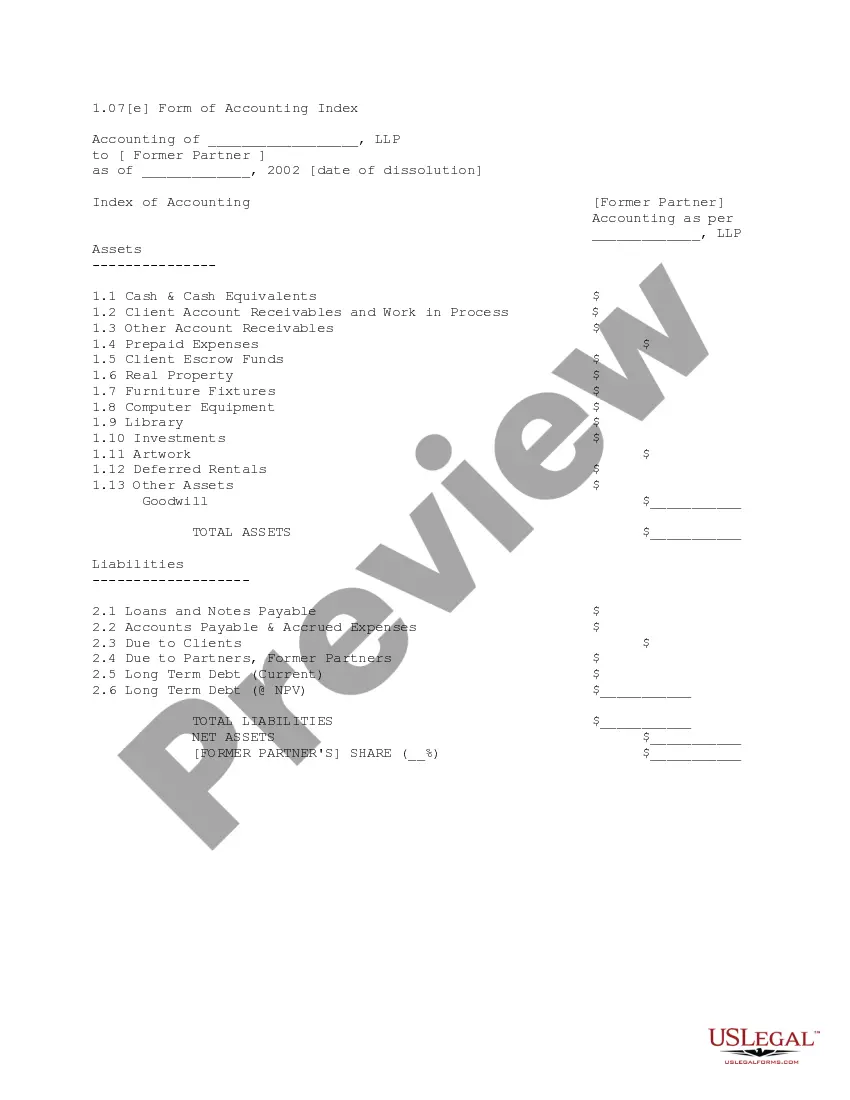

- Revenue or sales: Total income generated from goods or services sold during the period.

- Cost of goods sold: Direct costs attributable to the production of goods sold by the company.

- Gross profit: Revenue less the cost of goods sold.

- Operating expenses: Costs required for the day-to-day functioning of the business, excluding cost of goods sold.

- Net profit or loss: The final figure calculated by subtracting total expenses from total revenue.

When to use this document

The Profit and Loss Statement should be used during financial planning, tax preparation, and performance evaluations. It is particularly helpful when seeking loans, attracting investors, or managing budgets. This form is essential for any business that needs to assess its financial health or understand its revenue streams and cost management strategies.

Intended users of this form

- Business owners looking to analyze their financial performance.

- Accountants preparing financial statements for clients.

- Investors assessing potential investment opportunities.

- Financial institutions evaluating loan applications.

- Start-ups needing to create a business plan for funding.

How to complete this form

- Gather financial records, including sales data and expenses.

- Calculate total revenue and cost of goods sold for the period.

- Determine gross profit by subtracting cost of goods sold from total revenue.

- List all operating expenses incurred during the period.

- Subtract total expenses from gross profit to determine net profit or loss.

Does this form need to be notarized?

This form does not typically require notarization unless specified by local law.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to accurately categorize expenses, leading to misleading profit figures.

- Omitting non-operating income and expenses which can skew results.

- Not aligning the reporting period with accounting practices, causing inconsistencies.

Benefits of using this form online

- Easy accessibility allows users to fill out the form anytime and anywhere.

- Editability ensures users can make adjustments without redoing the entire document.

- Reliability from professionally drafted templates by licensed attorneys.

Legal use & context

- The Profit and Loss Statement is essential for compliance during audits.

- It can be used in financial reporting to stakeholders and regulatory bodies.

Main things to remember

- The Profit and Loss Statement summarizes a business's financial performance over time.

- It is essential for assessing profitability and making informed business decisions.

- Accurate completion is crucial for compliance and financial analysis.

Looking for another form?

Form popularity

FAQ

The profit and loss (P&L) statement is a financial statement that summarizes the revenues, costs, and expenses incurred during a specified period, usually a fiscal quarter or year. The P&L statement is synonymous with the income statement.

Step 1: Calculate revenue. Step 2: Calculate cost of goods sold. Step 3: Subtract cost of goods sold from revenue to determine gross profit. Step 4: Calculate operating expenses. Step 5: Subtract operating expenses from gross profit to obtain operating profit.

A Profit and Loss (P & L) statement measures a company's sales and expenses during a specified period of time.The categories include net sales, costs of goods sold, gross margin, selling and administrative expense (or operating expense), and net profit.

A profit and loss statement (P&L), or income statement or statement of operations, is a financial report that provides a summary of a company's revenues, expenses, and profits/losses over a given period of time. The P&L statement shows a company's ability to generate sales, manage expenses, and create profits.

What is a profit and loss statement? A profit and loss (or income) statement lists your sales and expenses. It tells you how much profit you're making, or how much you're losing. You usually complete a profit and loss statement every month, quarter or year.

First, show your business net income (usually titled "Sales") for each quarter of the year. Then, itemize your business expenses for each quarter. Then show the difference between Sales and Expenses as Earnings.

Choose a time frame. List your business revenue for the time period, breaking the totals down by month. Calculate your expenses. Determine your gross profit by subtracting your direct costs from your revenue. Figure out if you're making money.

Though the main purpose of an income statement is to convey details of profitability and business activities of the company to the stakeholders, it also provides detailed insights into the company's internals for comparison across different businesses and sectors.

Step 1: Calculate revenue. Step 2: Calculate cost of goods sold. Step 3: Subtract cost of goods sold from revenue to determine gross profit. Step 4: Calculate operating expenses. Step 5: Subtract operating expenses from gross profit to obtain operating profit.