PLLC Operating Statement

What this document covers

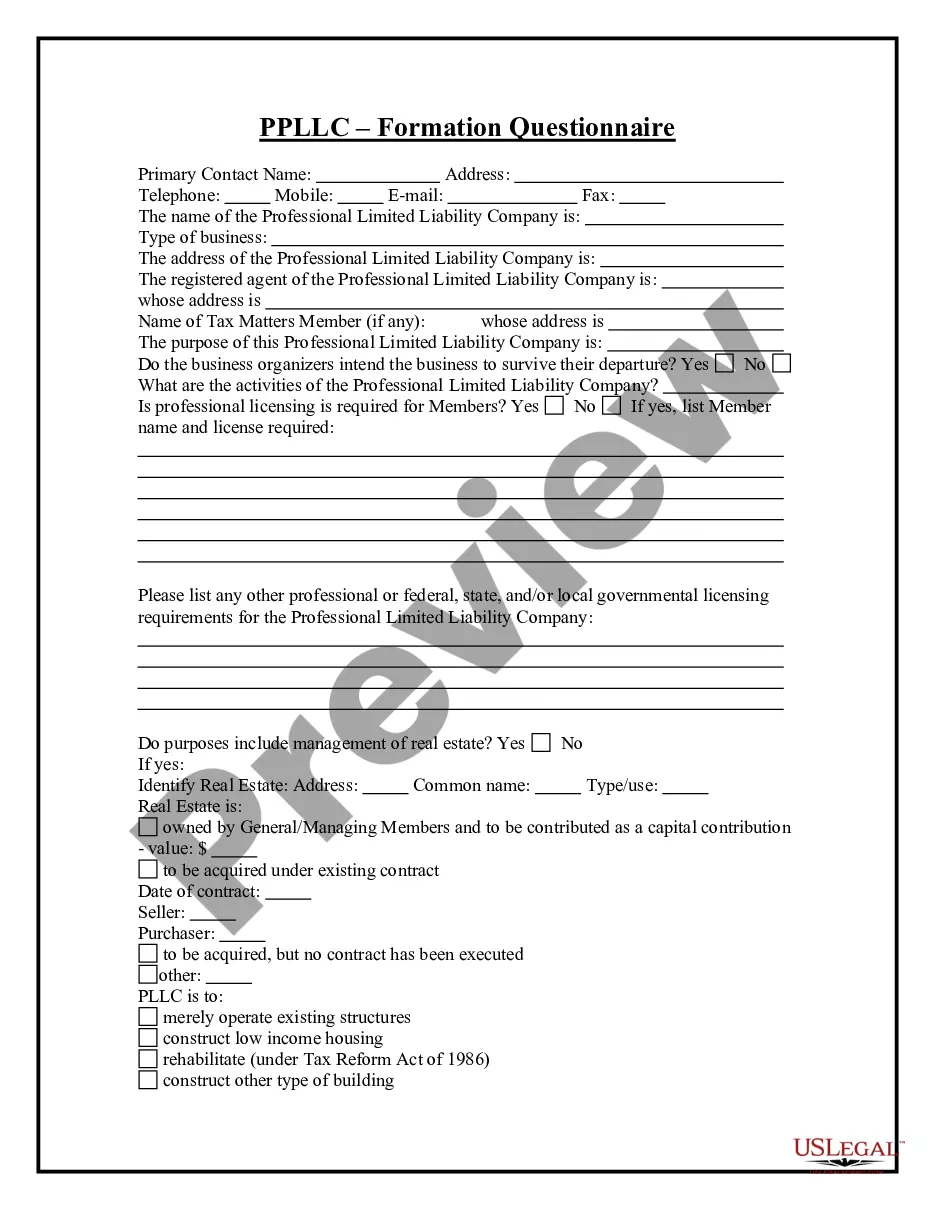

The PLLC Operating Statement is a legal document that outlines the operational framework for a Professional Limited Liability Company (PLLC). This form details the roles, responsibilities, and regulations governing the members of the LLC, ensuring that all parties understand the laws that guide their professional practices. Unlike regular LLC operating agreements, this statement specifically caters to professional service providers, such as accountants and attorneys, who may face unique regulatory requirements in their fields.

Key parts of this document

- Company name and ratification of the certificate of formation.

- Purpose and scope of the PLLC's operations.

- Details on member roles, voting powers, and management structure.

- Financial and accounting matters, including fiscal year and profit distribution.

- Provisions for the withdrawal, incapacity, and death of members.

- Guidelines for the dissolution of the entity and asset distribution.

Situations where this form applies

This form should be used when establishing a Professional Limited Liability Company for services in public accounting or similar professions. It is essential when forming a PSC (Professional Services Corporation) that requires compliance with specific legal and ethical standards, and it helps clarify the operational dynamics among multiple professionals working together in a business entity.

Who should use this form

This form is intended for:

- Founding members of a new professional limited liability company (PLLC).

- Accountants, attorneys, and other licensed professionals seeking to limit personal liability while practicing their professions.

- Existing PLLCs that need to update or formalize their operational statement.

Instructions for completing this form

- Identify and list the founding members and any additional members of the PLLC.

- Specify the PLLC's name and confirm it complies with state regulations.

- Define the purpose of the PLLC, outlining the professional services to be offered.

- Enter the financial contributions, ownership percentages, and any terms related to profit-sharing amongst members.

- Include provisions for member management, meetings, and voting requirements.

Does this document require notarization?

In most cases, this form does not require notarization. However, some jurisdictions or signing circumstances might. US Legal Forms offers online notarization powered by Notarize, accessible 24/7 for a quick, remote process.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to properly name the PLLC in compliance with state regulations.

- Not clearly outlining each member's roles and responsibilities.

- Omitting vital financial details, such as how profits will be shared.

- Neglecting to update the statement as member participation changes.

Why use this form online

- Quick and easy access to a professionally drafted document tailored for your needs.

- Editable fields allow for customization based on the specific requirements of your PLLC.

- Reliable templates ensure compliance with legal standards and help prevent common errors.

Looking for another form?

Form popularity

FAQ

The core elements of an LLC operating agreement include provisions relating to equity structure (contributions, capital accounts, allocations of profits, losses and distributions), management, voting, limitation on liability and indemnification, books and records, anti-dilution protections, if any, restrictions on

Get together with your co-owners and a lawyer, if you think you should (it's never a bad idea), and figure out what you want to cover in your agreement. Then, to create an LLC operating agreement yourself, all you need to do is answer a few simple questions and make sure everyone signs it to make it legal.

You do not need an attorney to form an LLC. Most states allow LLC formation by registering the business entity on your secretary of state's website and with the Internal Revenue Service (IRS). Once you register, you can buy or rent a building and have company bank accounts. Unfortunately, your company can also be sued.

As the owner of a single-member LLC, you don't get paid a salary or wages. Instead, you pay yourself by taking money out of the LLC's profits as needed. That's called an owner's draw. You can simply write yourself a check or transfer the money from your LLC's bank account to your personal bank account.

Choose a name for your LLC. File Articles of Organization. Choose a registered agent. Decide on member vs. manager management. Create an LLC operating agreement. Comply with other tax and regulatory requirements. File annual reports. Out of state LLC registration.

The LLC structure offers protection of personal assets in the same way a corporation protects shareholder assets. Creditors cannot sue members for liabilities of the company if the LLC goes into default. Owners receive a share of the profits of the company in proportion to their equity contribution as in a partnership.

Member Financial Interest. What percentage ownership does each member have? Corporate Governance. Corporate Officer's Power and Compensation. Non-Compete. Books and Records Audit. Arbitration/Forum Selection. Departure of Members. Fiduciary duties.

Pursuant to California Corporation's Code §17050, every California LLC is required to have an LLC Operating Agreement. Next to the Articles of Organization, the LLC Operating Agreement is the most important document in the LLC.

An operating agreement is a key document used by LLCs because it outlines the business' financial and functional decisions including rules, regulations and provisions. The purpose of the document is to govern the internal operations of the business in a way that suits the specific needs of the business owners.