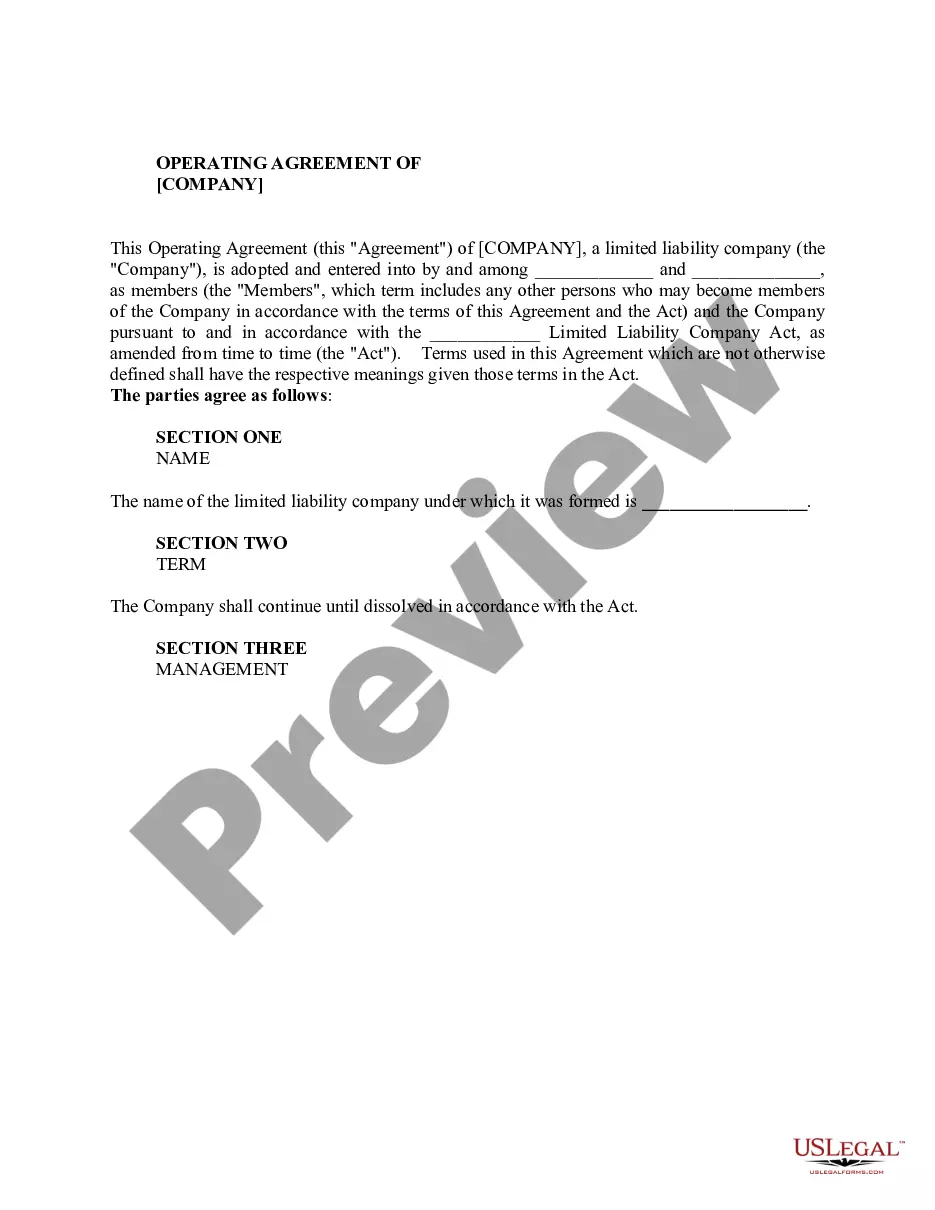

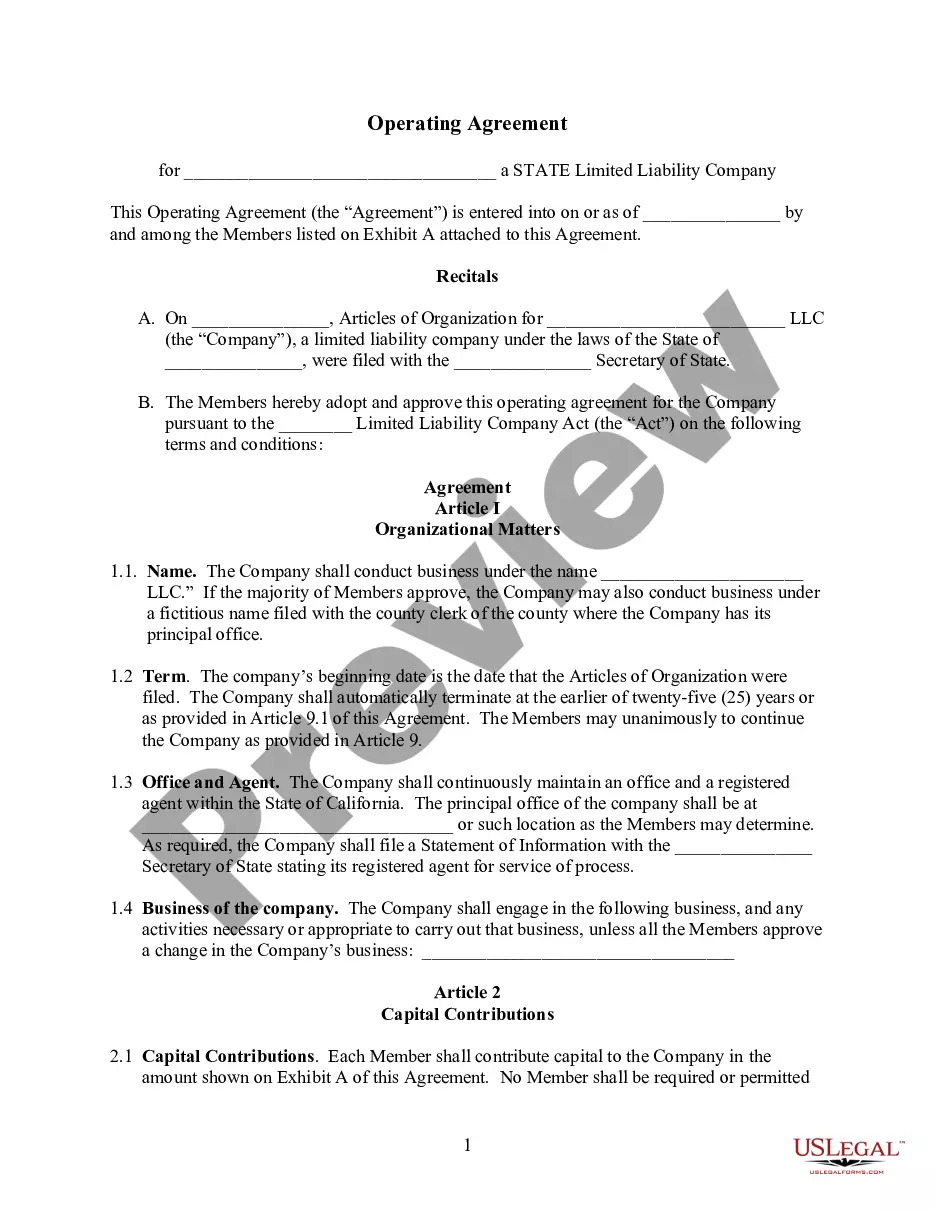

Limited Liability Company LLC Operating Agreement

Overview of this form

The Limited Liability Company (LLC) Operating Agreement is a crucial legal document that outlines the ownership and operational procedures of an LLC. This form details the agreement among members on how the company will be managed, the responsibilities of each member, profit-sharing, and what happens if a member decides to leave or is removed. Unlike simple business formation documents, this comprehensive agreement helps protect members from personal liability for the company's debts and obligations while clarifying management roles and responsibilities.

Form components explained

- Formation details of the LLC, including the name and business purpose.

- Roles and responsibilities of members and managers.

- Regulations for membership admission and termination.

- Profit-sharing agreements among members based on their percentage interests.

- Voting rights and procedures for members.

- Dissolution conditions and asset distribution procedures.

Common use cases

This form should be used when establishing a new limited liability company (LLC) or when existing members wish to formalize their operational agreements. It's particularly important when members are involved in joint ventures, have varying levels of investment, or anticipate changes in membership, management, or financial interests. Having an operating agreement is essential for clarity and legal protection among partners.

Who this form is for

- Entrepreneurs forming a new LLC.

- Existing LLC members wishing to formalize their agreement.

- Business partners engaging in shared ownership of an LLC.

- Individuals seeking to establish clear guidelines for management and profit distribution.

Instructions for completing this form

- Identify the parties involved by listing all members of the LLC in the designated section.

- Specify the name of the LLC and detail the business purpose clearly.

- Outline the roles and responsibilities of each member, including any managers.

- Agree on profit-sharing distributions and record the initial contributions of each member.

- Indicate the terms for member voting and how decisions will be made within the LLC.

Does this form need to be notarized?

This form does not typically require notarization to be legally valid. However, some jurisdictions or document types may still require it. US Legal Forms provides secure online notarization powered by Notarize, available 24/7 for added convenience.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to include all members in the agreement, leading to disputes over rights and responsibilities.

- Not specifying the dissolution process, which can complicate matters if the LLC needs to close.

- Neglecting to establish clear voting rights, resulting in potential conflicts on significant decisions.

Benefits of using this form online

- Convenient access to a legally vetted document that can be customized to your specific needs.

- Edit and update as your business grows and changes without needing to consult an attorney each time.

- Reliable templates that ensure compliance with legal standards, providing peace of mind for all members.

Legal use & context

- The LLC Operating Agreement is essential for defining the structure and operation of the company.

- It serves to protect the rights of both members and can be enforced in court if disputes arise.

- Failure to adopt a thorough agreement could lead to misunderstandings and conflicts among members.

Looking for another form?

Form popularity

FAQ

The primary advantage for an LLP is that it establishes a separate legal entity from that of the general partners. As such, an LLP may own property as well as sue and be sued in a legal arena. By far the most beneficial aspect of separate legal status is the limited liability protection it provides.

4 Answers. An LLC protects you from personally from all creditors, whether they be customers, shareholders, or other parties.Because only LLC assets are used to pay off business debts, LLC owners stand to lose only the money that they've invested in the LLC. This feature is often called "limited liability."

Similar to the LLC, the LLP is a hybrid of both the corporation and partnership, to give the greatest advantages for taxation and liability protection. The LLP is not a separate entity for income tax purposes and profits and losses are passed through to the partners.

Public disclosure is the main disadvantage of an LLP. Income is personal income and is taxed accordingly. Profit can not be retained in the same way as a company limited by shares. An LLP must have at least two members. Residential addresses were historically recorded at Companies House.

Personal Liability for Actions by LLC Co-Owners and Employees. In all states, having an LLC will protect owners from personal liability for any wrongdoing committed by the co-owners or employees of an LLC during the course of business.

LLPs have the same tax advantages of LLCs. They cannot, however, have corporations as owners. Perhaps the most significant difference between LLCs and LLPs is that LLPs must have at least one managing partner who bears liability for the partnership's actions.

What is a Limited Liability Company (LLC)?An LLC is a business entity with all the protection of a corporation plus the ability to pass through any business profits and losses to your personal income tax return.

An LLP protects each partner from debts against the partnership arising from professional malpractice lawsuits against another partner.

A Limited liability company (LLC) is a business structure that offers limited liability protection and pass-through taxation. As with corporations, the LLC legally exists as a separate entity from its owners. Therefore, owners cannot typically be held personally responsible for the business debts and liabilities.