Letter Informing Debt Collector of False or Misleading Misrepresentations in Collection Activities - Falsely Representing that Debtor has or is Committing Criminal Fraud by Nonpayment of a Debt

Overview of this form

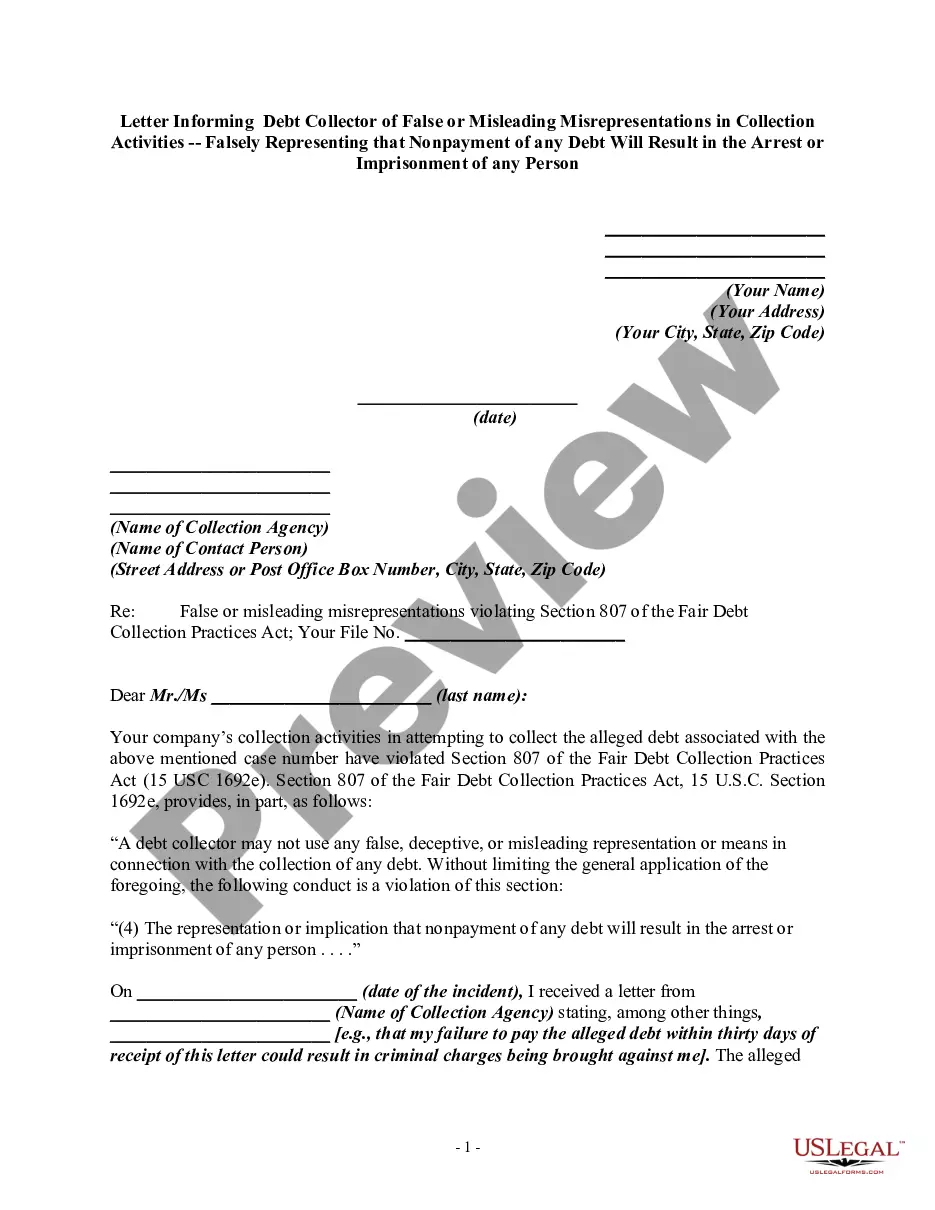

This form is a Letter Informing Debt Collector of False or Misleading Misrepresentations in Collection Activities. It serves to notify a debt collector that they have violated Section 807 of the Fair Debt Collection Practices Act by making false claims about criminal fraud due to nonpayment of a debt. This letter is an important tool for consumers to protect themselves against unethical debt collection practices and clarify the nature of their debt as strictly civil, not criminal.

Form components explained

- Your name and contact information.

- Date of the letter.

- Details of the collection agency and the specific contact person.

- Reference to the false representation made by the debt collector.

- Explanation regarding the nature of the alleged debt.

- Closing statement requesting cessation of unlawful behavior.

When to use this document

This form should be used when a debt collector has made misleading statements regarding the legal implications of nonpayment. If you have received threats or accusations implying that you have committed a crime simply due to not paying a debt, this letter will help you formally address these misrepresentations and provide clarification about your situation.

Who needs this form

- Consumers who have been contacted by debt collectors.

- Individuals who believe they have been subjected to false claims of criminal fraud by debt collectors.

- Anyone wishing to formally notify a debt collector of unethical collection actions.

How to complete this form

- Enter your name and address in the designated fields.

- Add the date on which you are sending the letter.

- Fill in the name of the collection agency and the contact person's name.

- State the specific misrepresentation made by the debt collector and provide context.

- Request that the agency cease its misleading collection practices.

- Sign your name at the bottom of the letter.

Does this document require notarization?

This form does not typically require notarization unless specified by local law. However, verifying if your state has any specific requirements can be beneficial.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to include accurate contact information for both parties.

- Not specifying the date of the misleading communication.

- Using vague language instead of clearly stating the false representation.

- Neglecting to sign the letter before sending it.

Benefits of completing this form online

- Convenience of immediate access to a legally vetted template.

- Ability to customize the form to fit your specific situation.

- Downloadable format for easy filing and record-keeping.

- Reliability, knowing the form adheres to current legal standards.

Looking for another form?

Form popularity

FAQ

Harassment of the debtor by the creditor More than 40 percent of all reported FDCPA violations involved incessant phone calls in an attempt to harass the debtor.

Debt collectors cannot harass or abuse you. They cannot swear, threaten to illegally harm you or your property, threaten you with illegal actions, or falsely threaten you with actions they do not intend to take. They also cannot make repeated calls over a short period to annoy or harass you.

In general, if you want to escalate the issue with the debt collector, you should do so within 30 days of receiving the validation letter. This includes disputing that you owe the debt, requesting additional verification of the debt, or requesting the name and address of the original creditor.

Write a letter disputing the debt. You have 30 days after receiving a collection notice to dispute a debt in writing. Dispute the debt on your credit report. Lodge a complaint. Respond to a lawsuit. Hire an attorney.

Never Give Them Your Personal Information. A call from a debt collection agency will include a series of questions. Never Admit That The Debt Is Yours. Even if the debt is yours, don't admit that to the debt collector. Never Provide Bank Account Information.

Unfair practices are prohibited Deposit or threaten to deposit a postdated check before your intended payment date. Take or threaten to take property if it's not allowed. Collect more than you owe on a debt, which may include fees and interest.

Debt validation is your federal right granted under the Fair Debt Collection Practices Act (FDCPA). To request debt validation, you must send a written request to the debt collector within 30 days of being contacted by the collection agency.

If you pay the collection agency directly, the debt is removed from your credit report in six years from the date of payment. If you don't pay, it purges six years from the last activity date, but you may be at risk for wage garnishment.

Step 1: Keep detailed records of what the debt collector is doing. Step 2: Take action write to the debt collector, complain to an External Dispute Resolution scheme (Ombudsman Service) or VCAT. Step 3: Complain to a Regulator.