Complex Will - Income Trust for Spouse

Understanding this form

The Complex Will - Income Trust for Spouse is a legal document that outlines how a person's assets and property will be distributed upon their death, specifically designed to establish an income trust for their spouse. This form differs from standard wills by allowing for the creation of a trust within the will, ensuring that the spouse receives income while allowing for the management and protection of the estate for the benefit of the children or other heirs. It is crucial for those who want to secure income for their surviving spouse while also considering the needs of their descendants.

Key components of this form

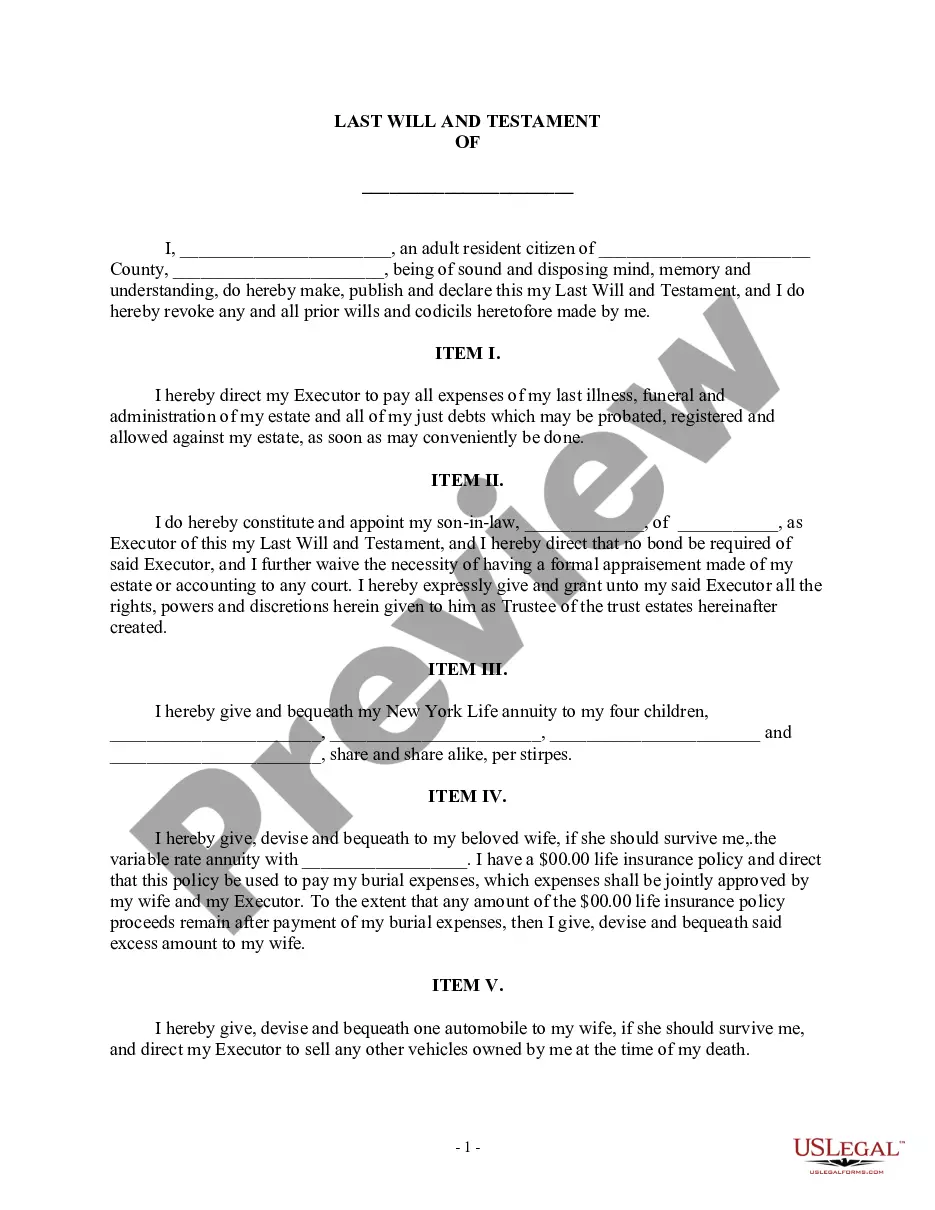

- Testamentary declarations stating the testator's intentions and revocation of prior wills.

- Appointment of an executor responsible for managing the estate and distributing assets.

- Specific bequests of property and assets to the surviving spouse and children.

- Creation of an income trust for the benefit of the spouse and future descendants.

- Provisions for the payment of debts, taxes, and funeral expenses out of the estate.

- Instructions for the distribution of any remaining estate assets following specific bequests.

Common use cases

This form should be used when an individual wishes to ensure their spouse is financially supported after their passing while also preserving wealth for future generations. It is particularly beneficial for individuals with complex estates, those who own significant assets, or anyone wanting to avoid probate complications for their beneficiaries.

Who can use this document

- Married individuals who want to provide for their spouse through an income trust.

- Parents who have children and want to ensure their welfare after their death.

- Individuals with considerable assets, such as real estate, investments, or businesses.

- Anyone seeking to create a legally binding document for the distribution of their estate.

How to prepare this document

- Begin by writing your name, county of residence, and date at the top of the form.

- Appoint an executor by naming the individual you trust to manage your estate.

- Clearly specify your spouse's name and the details of property and assets you wish to bequeath to them.

- Include instructions for creating the income trust and how the funds should be managed for your spouse.

- Sign the document in the presence of witnesses, as required by your state laws, to validate the will.

Does this document require notarization?

This form does not typically require notarization unless specified by local law. However, having the will notarized can provide an additional layer of legal protection and may help prevent disputes regarding authenticity.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to appoint a trusted executor, which can lead to disputes.

- Not being specific about whom the assets and property are intended for.

- Neglecting to update the will after major life events, such as marriage or the birth of children.

- Overlooking state-specific requirements that could invalidate the will.

Why complete this form online

- Convenient access to download and fill out your will from home without the need for legal consultations.

- Editability allows you to tailor the form to your specific needs, ensuring your wishes are accurately represented.

- Reliable and professionally drafted content, providing peace of mind regarding legal compliance.

Legal use & context

- This will serves to legally document the testatorâs wishes regarding their estate after death.

- It is enforceable in court, provided it is executed according to relevant state laws.

- Using an income trust within the will can provide financial security for the surviving spouse while ensuring the proper management of the estate for future beneficiaries.

Quick recap

- The form provides a direct way to create an income trust for your spouse within your will.

- It ensures clarity in asset distribution to prevent future disputes among beneficiaries.

- Helps manage estate and inheritance taxes, potentially reducing the tax burden on your loved ones.

Looking for another form?

Form popularity

FAQ

The short answer to the question, Can you withdraw cash from a trust account? is Yes, but there are some caveats.When you create a revocable trust and name someone else as the trustee, it can be helpful to specifically state in your trust that you are allowed to request cash withdrawals as you see fit.

An irrevocable income-only trust is a type of living trust often used for Medicaid planning. It protects assets from being sold to pay for nursing home and other long-term care expenses so that the assets can be passed on to beneficiaries.

A Canadian income trust is a type of investment trust that holds stable, income-producing assets and distributes payments to unitholders, or shareholders, on a periodic (monthly or quarterly) basis.

One important accounting concept is the difference between principal and income. The principal of an estate or trust is the amount originally received, plus capital gains and less debts, expenses, and capital losses.The income is the interest, dividends, and other income earned by the principal.

For What Expenses Can a Miller Trust / QIT Be Used? Funds deposited in a Miller / Qualifying Income Trust can only be used for very specific purposes. A trustee manages the trust account, which includes paying out money deposited in the trust.

How Income Trusts Work. With an income trust, much of the money that comes through the trust goes right back out to pay Medicaid for part of the cost of care. So a qualified income trust doesn't shelter income for the Medicare applicant, but without such an income trust, the applicant wouldn't qualify for Medicaid.

What Is A Qualified Income Trust (QIT)? If an individual's income is over the limit to qualify for Medicaid long-term care services (including nursing home care), a Qualified Income Trust (QIT) allows an individual to become eligible by placing income into an account each month that the individual needs Medicaid.

Money in Miller Trusts also goes towards paying share of cost, or in other words, goes towards paying for the cost of the Medicaid recipient's long-term care.Medical bills not paid for by Medicaid, and Medicare premiums, are also eligible expenses to be paid from an Irrevocable Income Trust.