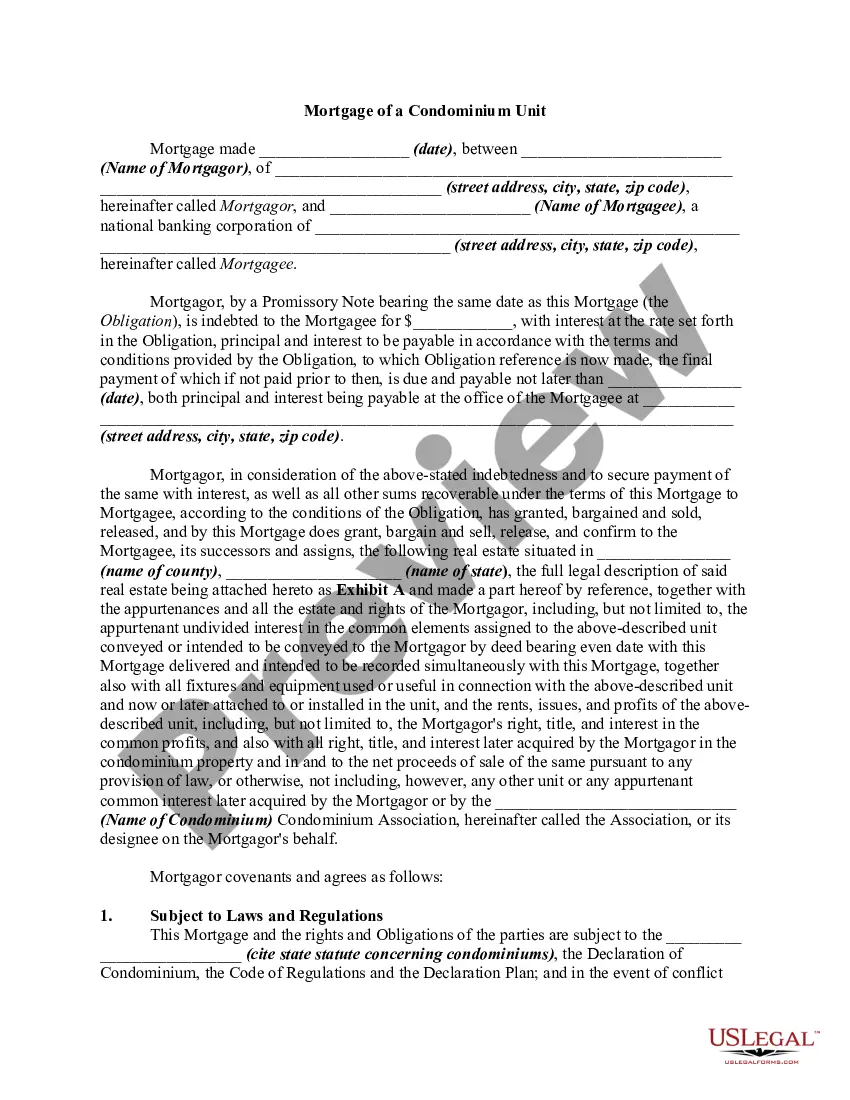

Mortgage of a Condominium Unit

Understanding this form

The Mortgage of a Condominium Unit is a legal agreement that uses a condominium unit as collateral for a loan or obligation. This type of mortgage ensures that if the borrower (mortgagor) defaults on their financial obligations, the lender (mortgagee) has the right to take possession of the property through foreclosure. Unlike traditional mortgages on standalone properties, this form specifically addresses the unique aspects of condominium ownership and management, including shared ownership of common areas and respect for condominium association rules.

Main sections of this form

- Date of the mortgage agreement

- Name and address of the mortgagor and mortgagee

- Details of the indebtedness, including amount and interest rate

- Legal description of the condominium unit

- Representations and warranties by both parties

- Covenants that govern the conduct of the mortgagor

- Conditions regarding taxes, assessments, and insurances

- Events of default and remedies available to the mortgagee

Situations where this form applies

This form should be used when a borrower wants to secure a loan using their condominium unit as collateral. It is typically required by lenders for personal loans, home equity loans, or to refinance existing loans. You may also need to use this form when consolidating debts or obtaining funds for major expenses while leveraging home equity.

Intended users of this form

This form is intended for:

- Individuals or couples who own a condominium unit and are seeking a mortgage.

- Lenders or financial institutions extending loans secured by condominium property.

- Real estate professionals assisting clients in financing condominium units.

How to complete this form

- Identify the parties involved by entering the names and addresses of the mortgagor and mortgagee.

- Specify the date on which the mortgage is executed.

- Provide the amount of indebtedness and the interest rate involved.

- Include a legal description of the condominium unit and attach it as Exhibit A.

- Add any specific provisions related to compliance with local laws and condominium association rules.

- Ensure all signatures are obtained and consider notarization if required by state law.

Notarization requirements for this form

Notarization is required for this form to take effect. Our online notarization service, powered by Notarize, lets you verify and sign documents remotely through an encrypted video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to provide accurate legal descriptions of the property.

- Not including all necessary parties involved in the agreement.

- Omitting critical clauses related to condominium regulations.

- Not properly stating the terms of repayment and interest.

Why complete this form online

- Convenience of downloading and completing the form at your own pace.

- Editability allows for customization to meet specific needs.

- Reliable templates created by licensed attorneys to ensure legal compliance.

Looking for another form?

Form popularity

FAQ

A 30-year mortgage benefits borrowers who are more concerned with obtaining a certain monthly payment or qualifying for a condo loan than the total cost of financing in the long-run. For example, a 30-year loan spreads payments out over 360 months and a 15-year loan only spreads them out over 180 months.

Less Space and Flexibility. Another one of the reasons not to buy a condo is that you have less space and flexibility in how you use your place. Some condos offer owners extra storage space or possibly a basement, but you'll still likely have a smaller, more compact living environment than you would in a house.

Condo/co-op fees or homeowners' association dues are usually paid directly to the homeowners' association (HOA) and are not included in the payment you make to your mortgage servicer. Condominiums, co-ops, and some neighborhoods may require you to join the local homeowners' association and pay dues (HOA dues).

Buying a condominium is a home purchase, but condo financing isn't entirely like mortgages for single-family homes. Getting a condo mortgage requires additional steps in underwriting, and some loan programs have specific rules.

Both the down payment and interest rate on a condo mortgage will be higher than they would for a regular house at the same price. Lenders charge more for loans on condo units because their value depends on more than just the borrower's financials.

The mortgage rates on condominiums are usually higher than what the same borrower would pay if they were purchasing a single-family home on similar terms. That's because condominium mortgages are considered somewhat riskier loans than are mortgages for single-family homes.

Paying your fees Typically, they aren't added to your mortgage, but are separately deducted from your bank account monthly or paid by check, said Riley Adams, a certified public accountant in New Orleans, La. To my knowledge, I have not seen HOA fees included directly in a mortgage before, Adams said.

As a result, it's simply more difficult to get a loan to buy a condo. Assuming you can't pay cash, it's easiest to finance a condo with a conventional mortgage rather than an FHA or VA home loan, which we'll discuss below.For example, a conventional mortgage requires a loan-to-value (LTV) ratio of 80% or less.