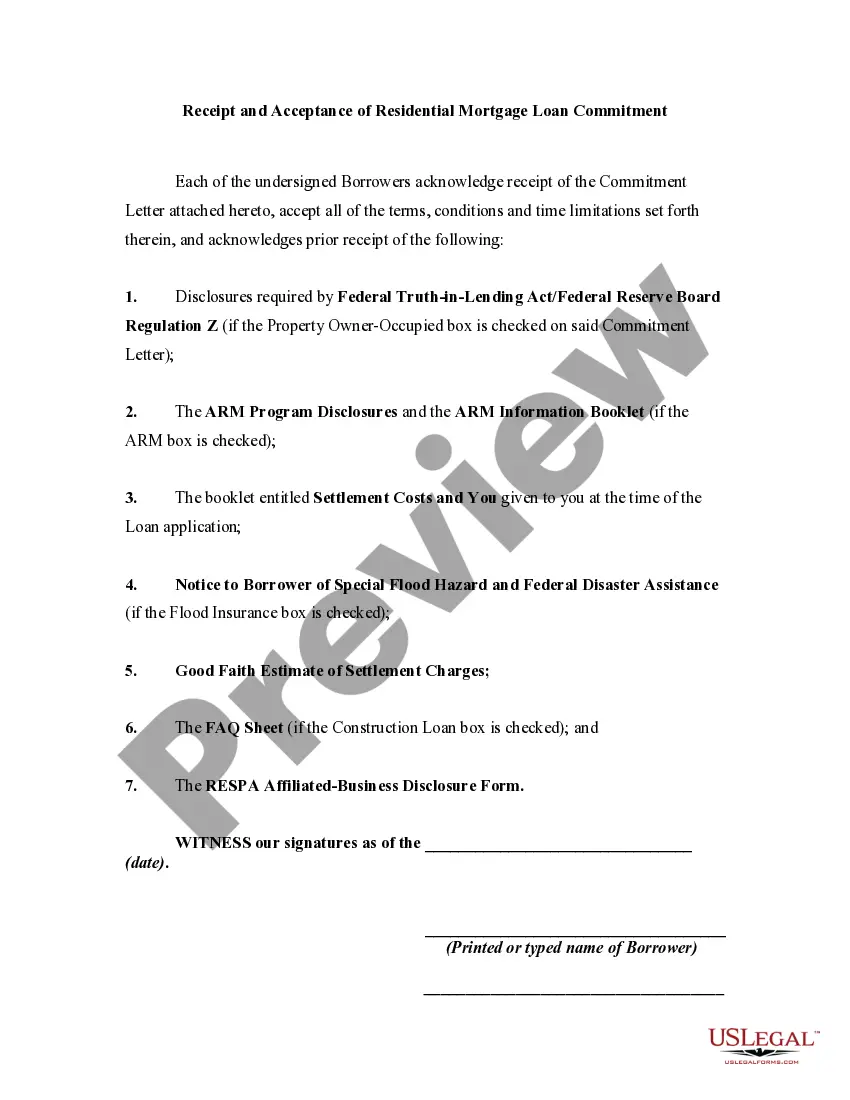

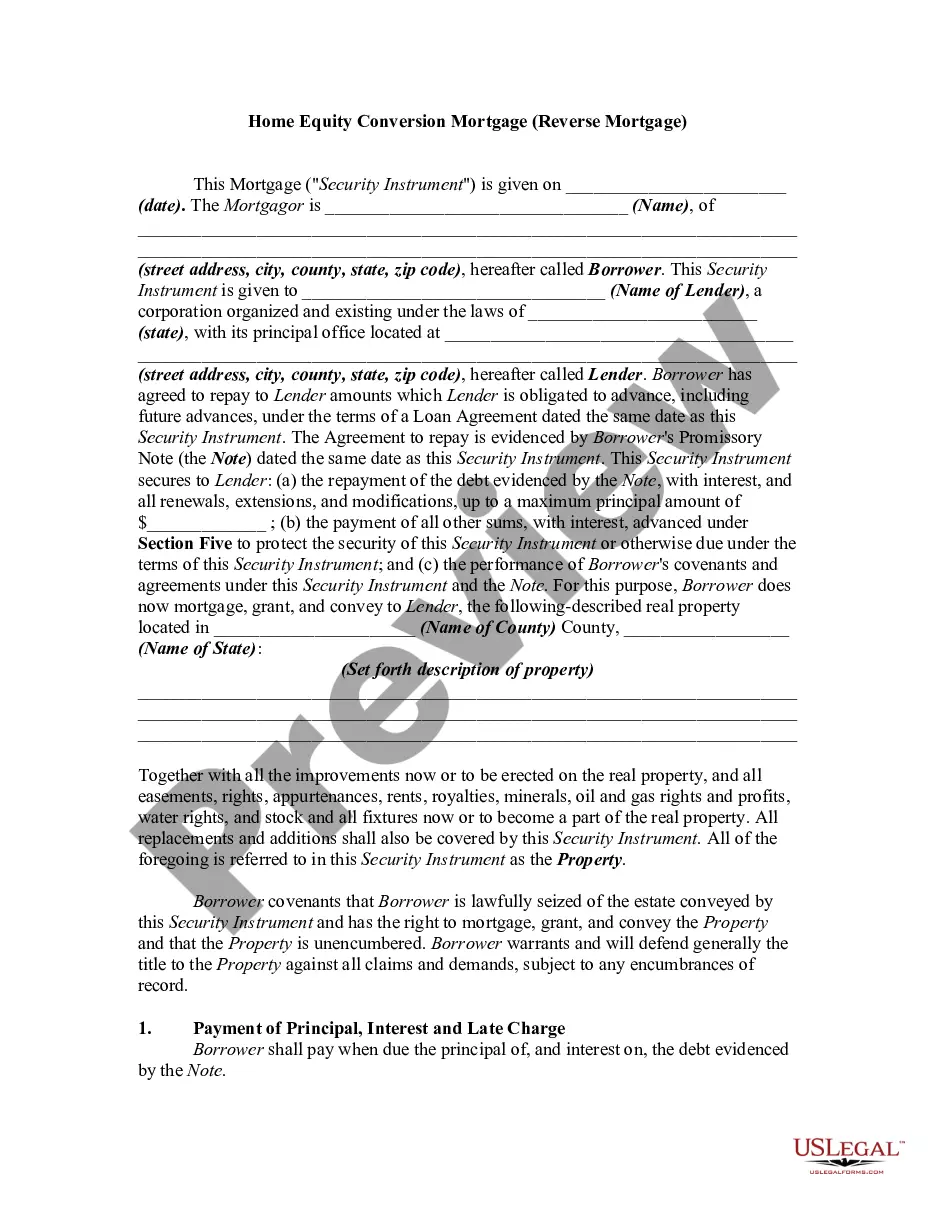

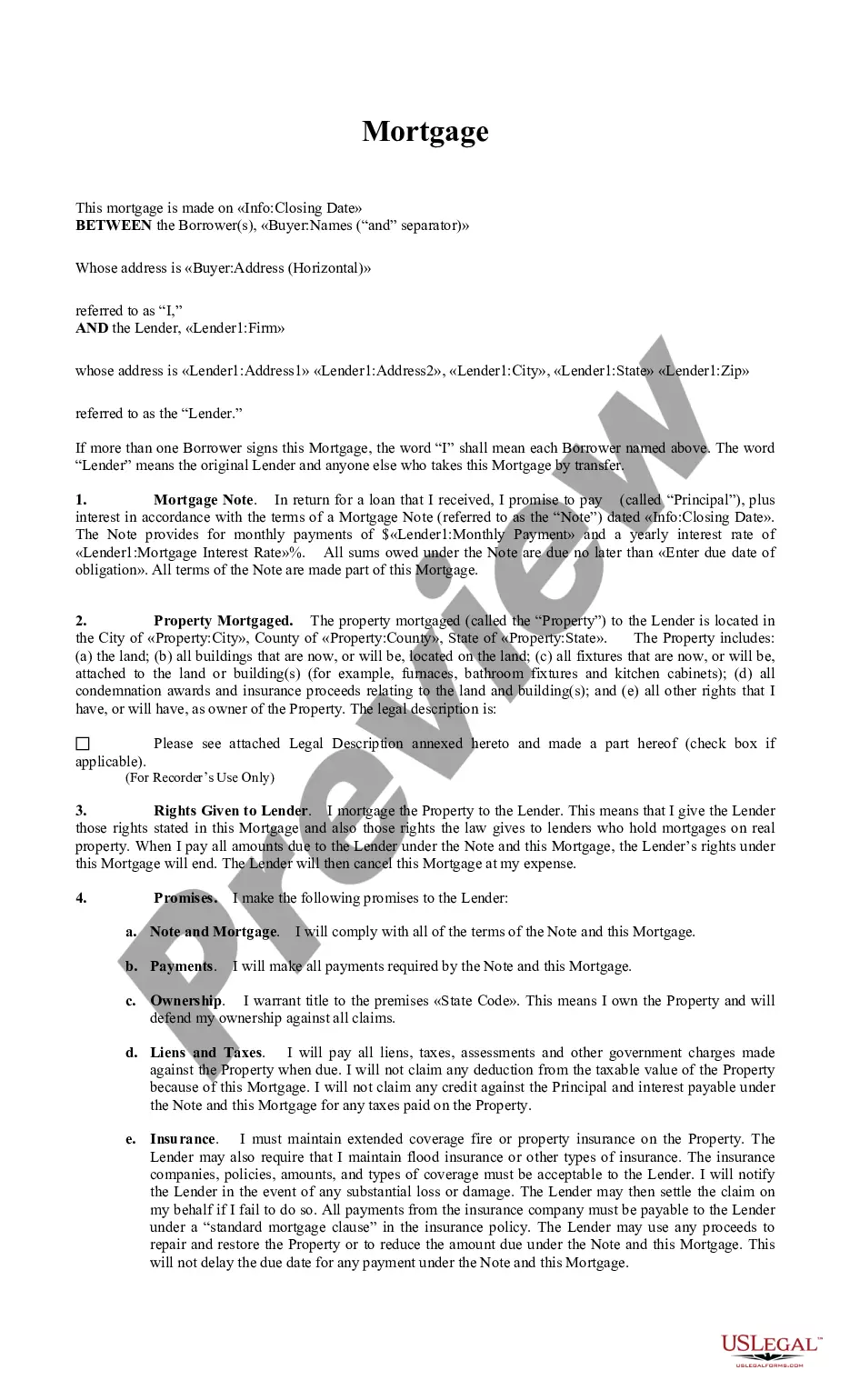

Mortgage Loan Commitment for Home Equity Line of Credit

The Mortgage Loan Commitment for Home Equity Line of Credit is a legal document that signifies the lender's approval of a borrower's application for a home equity line of credit. This form serves as a commitment by the lender to provide funds that may be borrowed as needed, using the equity in the borrower's home as collateral. Unlike traditional home equity loans that offer a lump sum, this commitment allows for flexible borrowing within approved limits, akin to a credit card. It also outlines the terms, conditions, and variable interest rates associated with the credit line, differentiating it from conventional loans.

- Letterhead of the lender and date of issue

- Name and address of the mortgagor

- Loan amount and initial annual percentage rate (APR)

- Principal and interest payment structure

- Terms and conditions including additional fees and requirements

- Commitment expiration date

- Evidence of title and insurance requirements

This form is used when a homeowner applies for a home equity line of credit and receives approval from a lender. It is necessary when the borrower intends to access funds for significant expenses such as home renovations, educational costs, or medical bills, leveraging their home equity while maintaining flexibility in borrowing. The commitment letter is also important when finalizing terms before closing the loan.

This form is intended for:

- Homeowners seeking a line of credit secured by their home equity

- Lenders approving home equity lines of credit

- Mortgage brokers assisting clients with the submission process

To complete this form, follow these steps:

- Identify the lender and provide their letterhead and date.

- Enter the name and complete address of the mortgagor.

- Specify the loan amount and initial APR, ensuring accuracy in figures.

- Outline the terms of principal and interest payments.

- Add any additional terms, including fees or required items prior to closing.

- Include the commitment expiration date and any necessary insurance or appraisal information.

This form does not typically require notarization unless specified by local law. Ensure that all parties involved understand their obligations and the conditions of the commitment before finalization.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid when completing this form include:

- Failing to accurately fill out the borrowerâs name and address information.

- Not specifying the correct loan amount or interest rate.

- Omitting required additional terms or conditions.

- Missing the commitment expiration date, which could delay processing.

Benefits of using this form online include:

- The convenience of downloading and printing from home.

- The ability to easily fill out the form electronically or by hand.

- Access to legal templates drafted by licensed attorneys, ensuring compliance and reliability.

- The form serves as a commitment from the lender for a home equity line of credit.

- It outlines key loan terms, interest rates, and obligations for both the borrower and lender.

- Completing this form correctly is essential for a smooth approval process.

- Understanding state-specific requirements is critical to ensure compliance.

Looking for another form?

Form popularity

FAQ

Federally-related mortgage loans can often close within 30 days, but special first-time home buyer programs, particularly those involving help with the buyer's down payment, might take 35 to 50 days. These special loans typically require approval from two underwriting processes.

HELOCs allow you to make interest-only payments during the draw period, then you make principal and interest payments after. Additional principal payments on a home equity loan reduce your payment period; for a HELOC, they reduce your monthly payments.

HELOCs generally have variable interest rates. The interest rate is based on a benchmark rate, such as the federal funds rate, plus a margin, which is established by the lender. When interest rates go up, your monthly payment will go up too.

HELOC repayment Typically, you're only required to make interest payments during the draw period, which tends to be 10 to 15 years. You can also make payments back toward the principal during the draw period. When you pay off part of the principal, those funds go back to your line amount.

A home equity loan is also a mortgage.Assuming your credit is good, and you otherwise qualify, you can take out an additional loan using that $100,000 as collateral. Like a traditional mortgage, a home equity loan is an installment loan repaid over a fixed term.

Pay interest only on the amount you draw. Use as much (or as little) of the credit line as you need during the draw period, which usually lasts 10 years. Pay the balance to zero and charge it again during the draw period.

At any time, you can pay off any remaining balance owed against your HELOC.If you pay off your HELOC balance early, your lender may offer you the choice to close the line of credit or keep it open for future borrowing. Why you should close a HELOC. Sometimes, a lender will charge annual fees for open lines of credit.

You can replace your HELOC with a new HELOC. This gives you more time to pay off your balance, and may lower your payment. You can replace your HELOC with a HELOAN, giving you a fixed interest rate and additional time to retire your balance.You can combine the HELOC and your first mortgage into a new first mortgage.

The letter will also feature your lender's information, your loan number, and the date your commitment letter will expire. You'll also find the terms of you loan listed in the letter. These may include the amount of money you'll pay each month and the number of monthly payments you'll make until the loan is paid off.