Home Equity Conversion Mortgage - Reverse Mortgage

Understanding this form

The Home Equity Conversion Mortgage form, commonly known as a reverse mortgage, is a financial tool designed for homeowners aged 62 and older. This loan allows eligible homeowners to convert part of their home equity into cash, providing tax-free funds to support their retirement. Unlike traditional mortgages, homeowners do not make monthly loan payments; instead, the lender pays the homeowner. The loan must be repaid when the homeowner dies, sells the home, or moves out permanently, making it a unique financial option compared to other mortgage products.

Form components explained

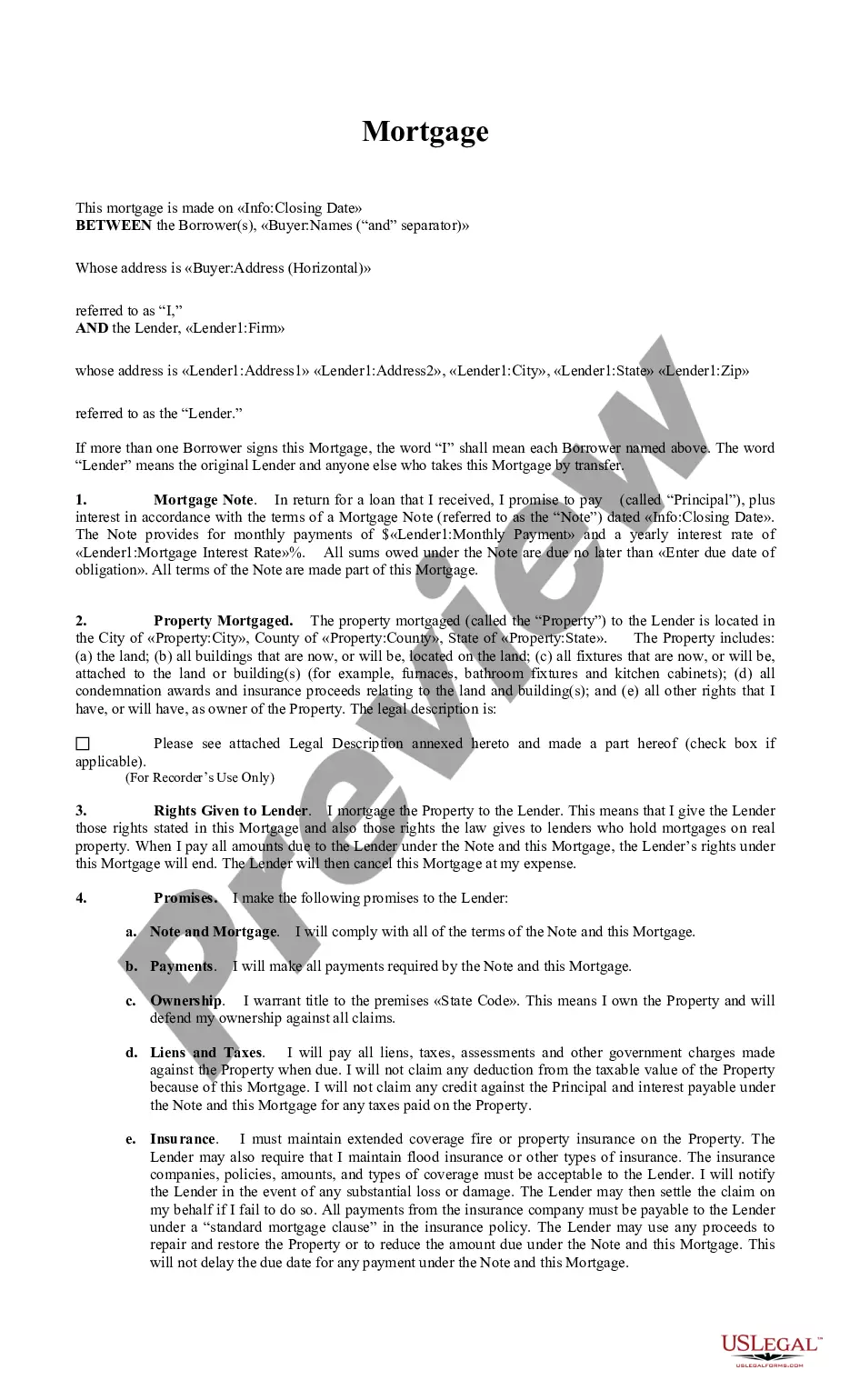

- Date of the mortgage agreement.

- Borrower and lender identification, including their addresses.

- Terms of repayment, including principal and interest obligations.

- Details regarding property insurance and maintenance responsibilities.

- Conditions for loan acceleration and foreclosure procedures.

- Specification of property and rights related to rents and revenues.

Situations where this form applies

This form is essential for seniors who wish to access their home equity without ongoing payment obligations. It is commonly used by homeowners looking to supplement their retirement income, cover healthcare costs, or make home improvements. Additionally, it may be utilized when planning for estate management, allowing homeowners to secure funds while retaining ownership of their home until they pass away or relocate.

Intended users of this form

- Homeowners aged 62 and older.

- Individuals seeking financial assistance during retirement.

- Those who wish to convert home equity into cash without monthly mortgage payments.

- Seniors considering financing for health care or home repairs.

How to complete this form

- Identify and enter the date of the mortgage agreement.

- Fill in the names and addresses of both the borrower and the lender.

- Specify the amounts to be secured by the mortgage and any conditions related to payment.

- Ensure the property description is accurate and complete.

- Review all sections thoroughly, sign, and date to validate the agreement.

Notarization guidance

This form must be notarized to be legally valid. US Legal Forms provides secure online notarization powered by Notarize, allowing you to complete the process through a verified video call.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Incorrectly entering personal information for all parties involved.

- Failing to provide a complete property description.

- Not reviewing the terms and conditions before signing.

- Omitting necessary signatures and dates.

Benefits of using this form online

- Convenience: Download and complete your form from the comfort of your home.

- Editability: Easily modify any section as needed before finalizing.

- Reliability: Forms are drafted by licensed attorneys to ensure compliance with legal standards.

Looking for another form?

Form popularity

FAQ

The only reverse mortgage insured by the U.S. Federal Government is called a Home Equity Conversion Mortgage (HECM), and is only available through an FHA-approved lender. The HECM is FHA's reverse mortgage program that enables you to withdraw a portion of your home's equity.

The chief difference between a reverse mortgage and a home equity loan is that the reverse mortgage requires no payments.On a home equity loan, monthly payments are made until the loan is repaid, usually for a term of 30 years.

A home equity conversion mortgage (HECM) is a type of reverse mortgage that is Federal Housing Administration (FHA) insured.HECM terms are often better than those of private reverse mortgages, but the loan amount is fixed, and mortgage insurance premiums are required.

Inform the lender you have a reverse mortgage and want a HELOC. To take out a HELOC, you must have remaining equity in the home. Since you can't convert the reverse mortgage to a HELOC, you must pay off the mortgage. The loan balance can be rolled into the HELOC, resulting in a higher monthly payment.

What Is a HECM Reverse Mortgage? It is a loan to a senior secured by a mortgage lien on the senior's house, with most of the loan proceeds usually paid out over time rather than upfront, and with no repayment obligation so long as the senior lives in the house.

The general rule of thumb is that a reverse mortgage works better for someone who needs a long-term, steady source of income, while a home equity loan is better for someone who needs short-term cash that they can repay.

The Home Equity Conversion Mortgage (HECM) is Federal Housing Administration's. (FHA) reverse mortgage program which enables you to withdraw some of the equity. in your home. You choose how you want to withdraw your funds, whether in a fixed. monthly amount or a line of credit or a combination of both.