Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children

Understanding this form

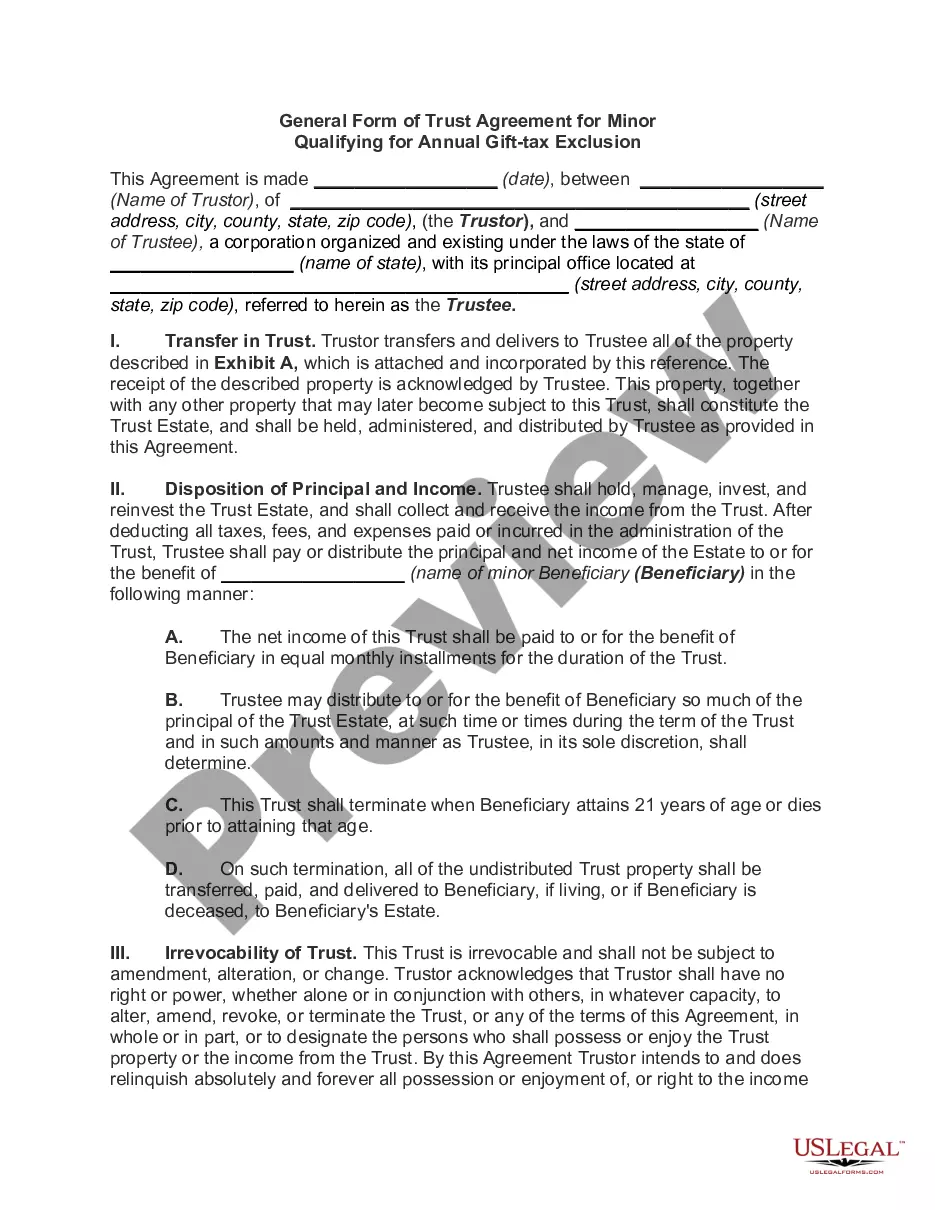

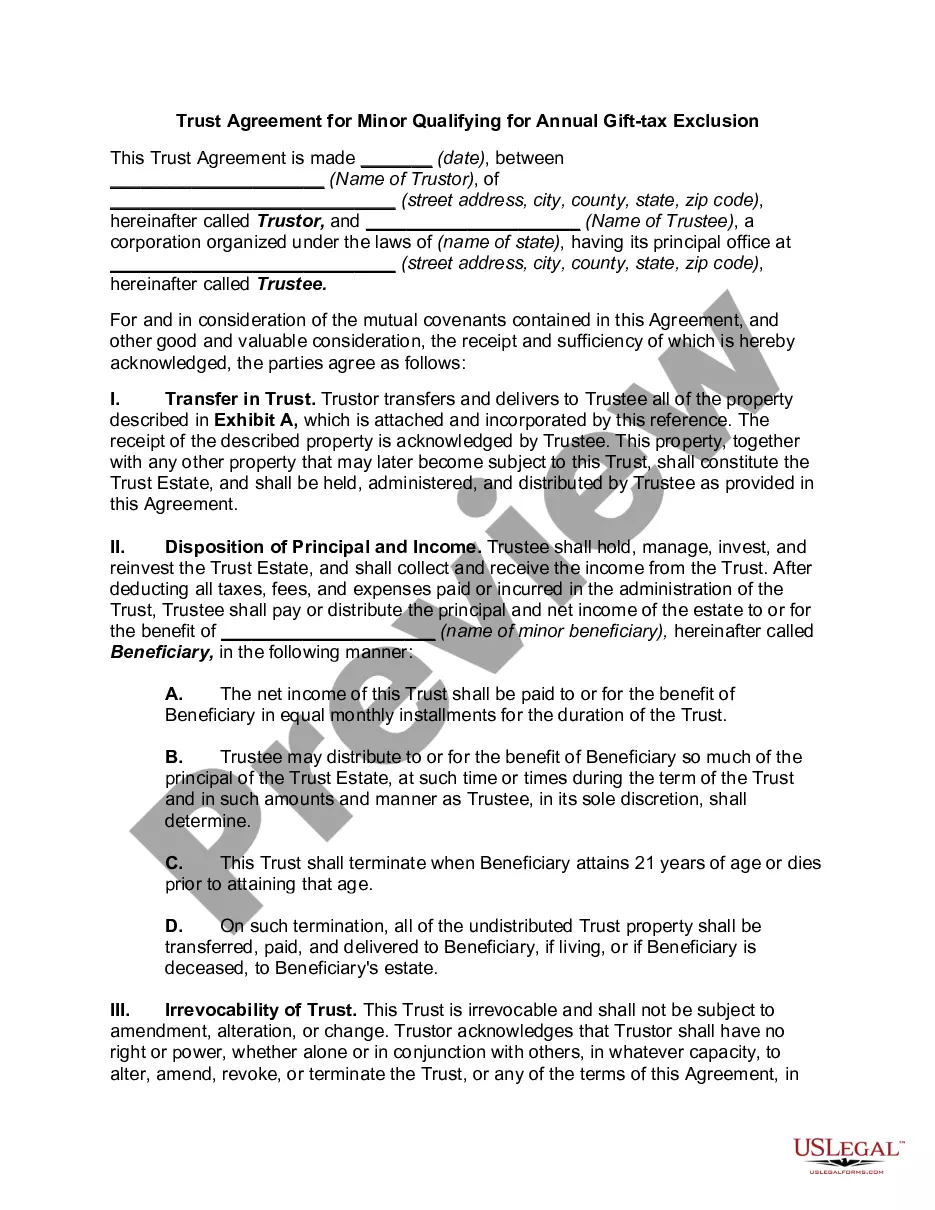

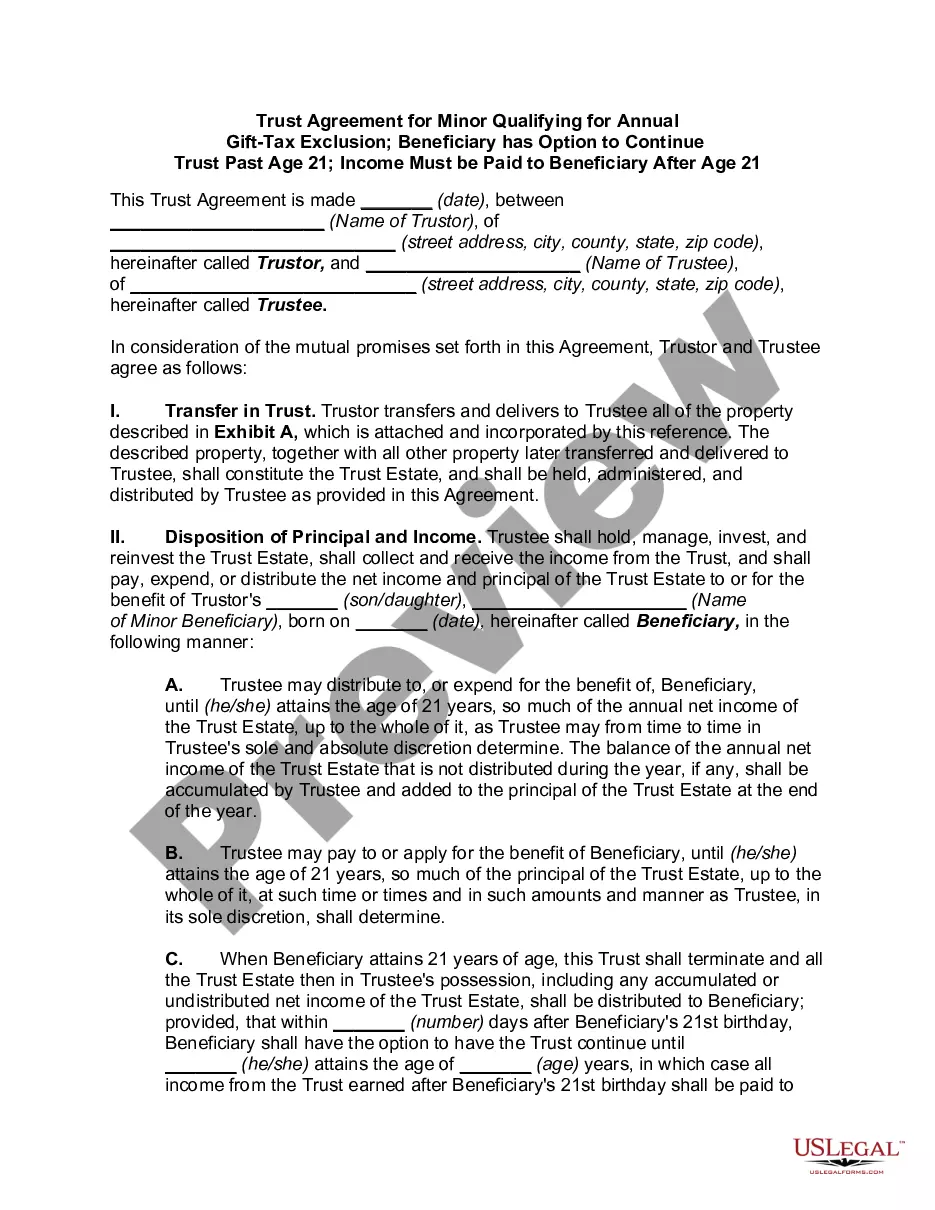

This form is a Trust Agreement for Minors qualifying for the Annual Gift Tax Exclusion, specifically designed for multiple trusts set up for children. It establishes present interest trusts, which allow parents or guardians to transfer assets into trusts that benefit their minor children. By adhering to Section 2503(c) of the Internal Revenue Code, this form ensures that gifts made to the trusts qualify for the annual gift tax exclusion.

Key parts of this document

- Identification of Grantors and Trustee, including their names and addresses.

- Establishment of irrevocable trusts for the benefit of minor children.

- Distribution guidelines for income and principal to beneficiaries.

- Provisions for the Trust Committee, including powers to change the Trustee.

- Clauses for final distributions upon the beneficiaries' reaching specified ages.

- Details for handling the property designated for the trusts.

Common use cases

This form is used when parents or guardians want to create irrevocable trusts for their minor children, ensuring that funds can be managed and distributed according to their wishes. It is particularly useful when planning to transfer assets in a tax-efficient manner under the annual gift tax exclusion, thereby providing financial security and potential tax benefits for the child's future.

Who this form is for

- Parents seeking to establish trusts for their minor children.

- Guardians or family members designated to manage trusts for minors.

- Individuals planning to maximize their annual gift tax exclusions through present interest trusts.

- Wealthy individuals interested in providing a structured financial future for their children.

Instructions for completing this form

- Identify the parties by filling in the names and addresses of the Grantors and the Trustee.

- List the minor children who will be the primary beneficiaries of the trusts.

- Specify the properties to be conveyed to the trusts in Exhibit A.

- Detail the terms for distributing income and principal to the beneficiaries based on age milestones.

- Sign and date the agreement to formalize the establishment of the trusts.

Does this document require notarization?

This form does not typically require notarization unless specified by local law. However, having it notarized can provide an extra layer of authenticity and security.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to clearly identify all parties involved in the trust agreement.

- Inaccurately specifying the properties to be included in the trust.

- Neglecting to detail the distribution timeline or conditions effectively.

- Not considering the implications of state-specific trust laws.

- Forgetting to sign and date the form, which can render the agreement invalid.

Benefits of using this form online

- Convenience of immediate access and download without needing a lawyer's visit.

- Editability allows users to tailor the form to their specific needs.

- Reliable templates drafted by licensed attorneys ensure legal soundness.

- Easier completion compared to handwritten versions with clear, structured fields.

Legal use & context

This Trust Agreement is designed to be legally enforceable, providing structure for managing assets for minors. Its compliance with tax regulations enhances its legitimacy and ensures that the Grantors can achieve their gifting goals without unnecessary tax burdens.

What to keep in mind

- A Trust Agreement for Minors allows for efficient asset management and tax benefits.

- The Trust must be irrevocable, providing stability for beneficiaries.

- Proper execution and understanding of the Trust terms are crucial to uphold legal validity.

Legal terms and meanings

- Grantors: Individuals who create the Trust and contribute assets to it.

- Trustee: The appointed individual or institution responsible for managing the Trust.

- Primary Beneficiaries: The minors for whose benefit the Trust is established.

- Irrevocable Trust: A Trust that cannot be altered or terminated by the Grantors once established.

Looking for another form?

Form popularity

FAQ

Gifts that are not more than the annual exclusion for the calendar year. Tuition or medical expenses you pay for someone (the educational and medical exclusions). Gifts to your spouse. Gifts to a political organization for its use.

The primary way the IRS becomes aware of gifts is when you report them on form 709. You are required to report gifts to an individual over $14,000 on this form. This is how the IRS will generally become aware of a gift.

If you give more than $15,000 in cash or assets (for example, stocks, land, a new car) in a year to any one person, you need to file a gift tax return. That doesn't mean you have to pay a gift tax. It just means you need to file IRS Form 709 to disclose the gift.

You may need to file a gift tax return If you make a taxable gift (one in excess of the annual exclusion), you must file Form 709: U.S. Gift (and Generation-Skipping Transfer) Tax Return. The return is required even if you don't actually owe any gift tax because of the $11.58 million lifetime exemption.

A Section 2503c trust is a type of minor's trust established for a beneficiary under the age of 21 which allows parents, grandparents, and other donors to make tax-free gifts to the trust up to the annual gift tax exclusion amount and the generation skipping transfer tax exclusion amount.

The value of all gifts made during the year to a single beneficiary count towards the donor's $15,000 annual exclusion, no matter what their form. Thus, if you give your child a $10,000 automobile, you have used $10,000 of your annual exclusion and have $5,000 left to give that child within the annual exclusion amount.

The annual exclusion is the amount of money that one person may transfer to another as a gift without incurring a gift tax or affecting the unified credit. This annual gift exclusion can be transferred in the form of cash or other assets.

4. Do gifts to a Gift Trust qualify for the annual exclusion?Gifts in trust do not qualify for the annual exclusion unless the trust either qualifies as a Minor's Trust under Internal Revenue Code Section 2503(c) or has certain temporary withdrawal powers called Crummey powers.

Trusts for minors, or minor's trusts, are very specific types of trusts that are used to hold and distribute property or assets to minors. They typically provide instructions that the money or property assets will be held in trust until the minor reaches the age of majority.