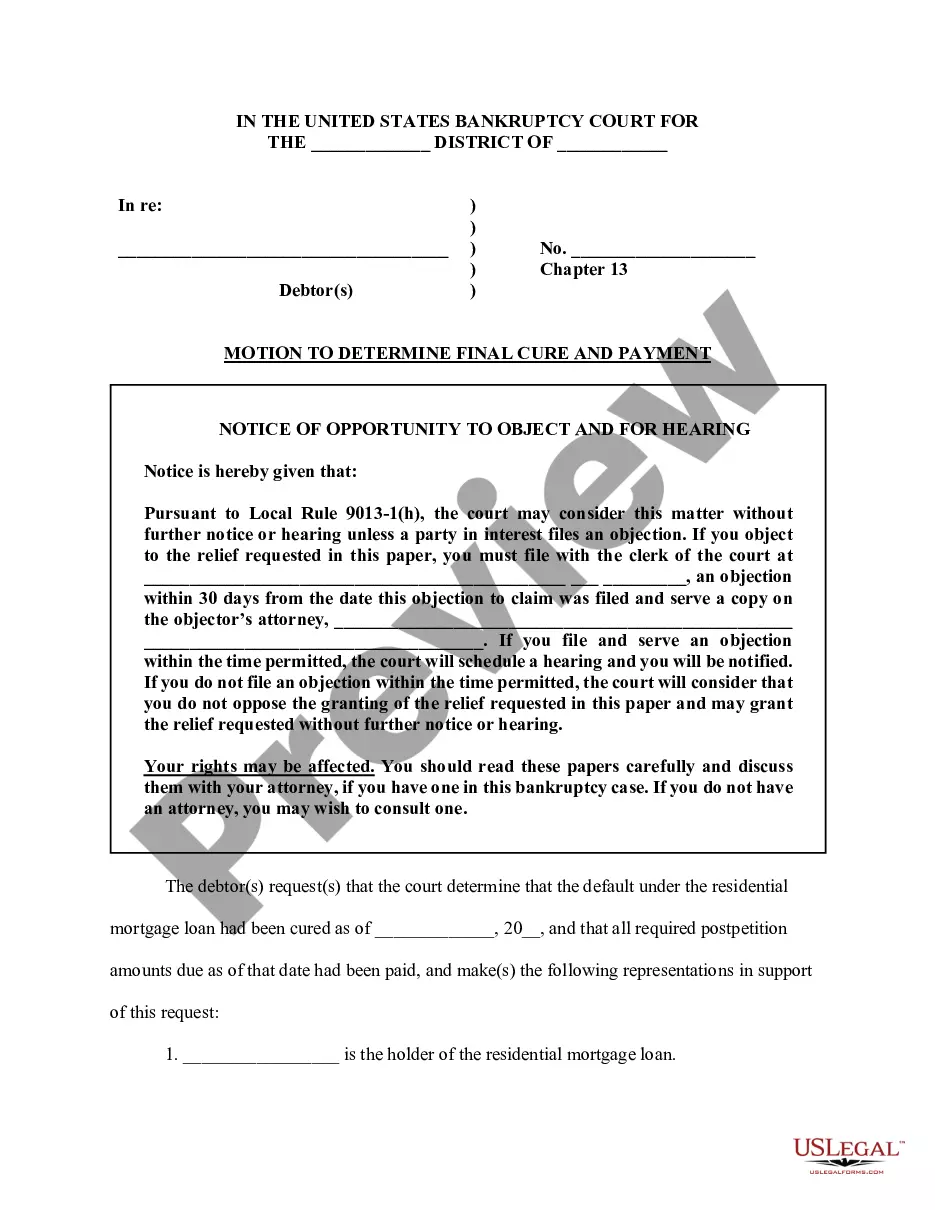

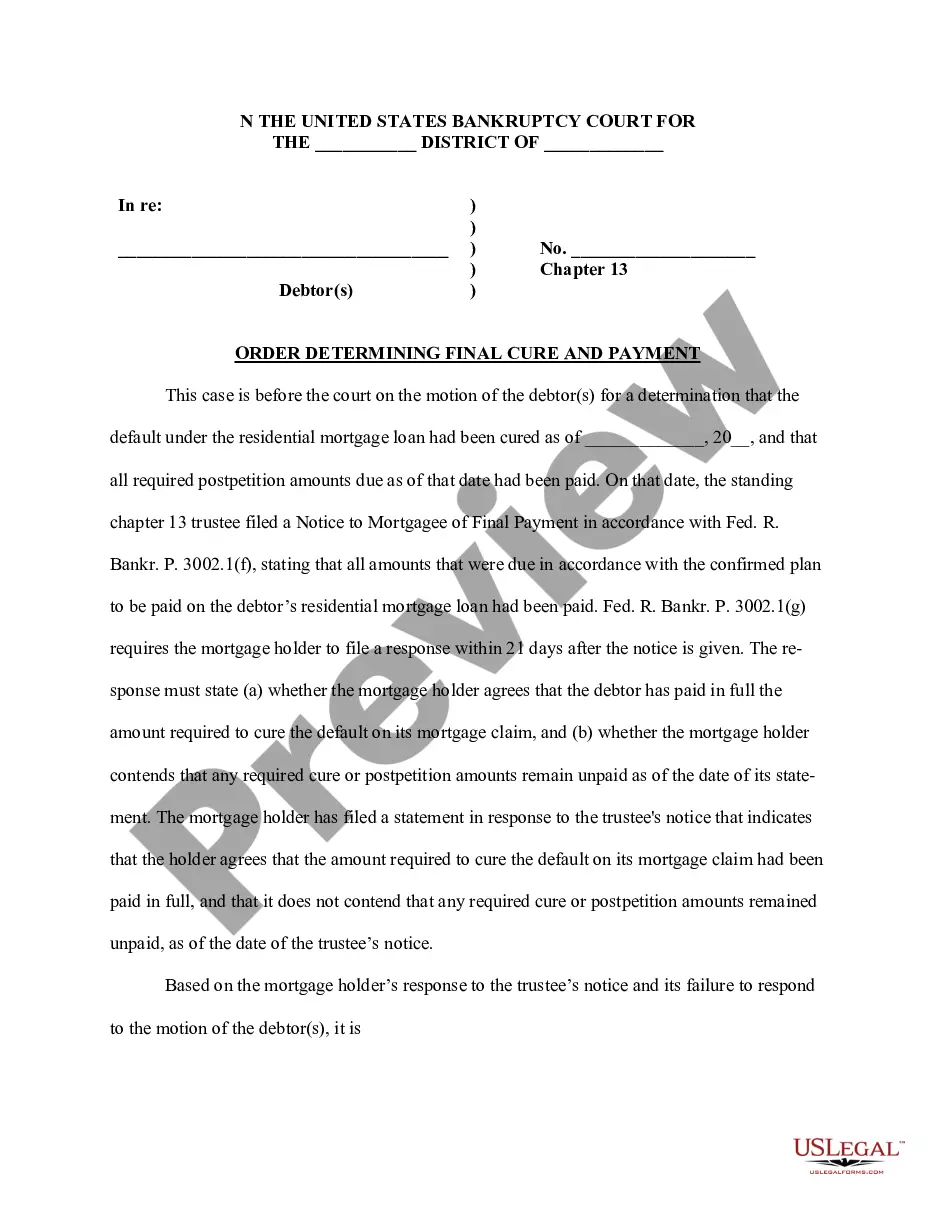

Motion to determine final cure and payment (mortgagee's response agrees with trustee's notice)

Understanding this form

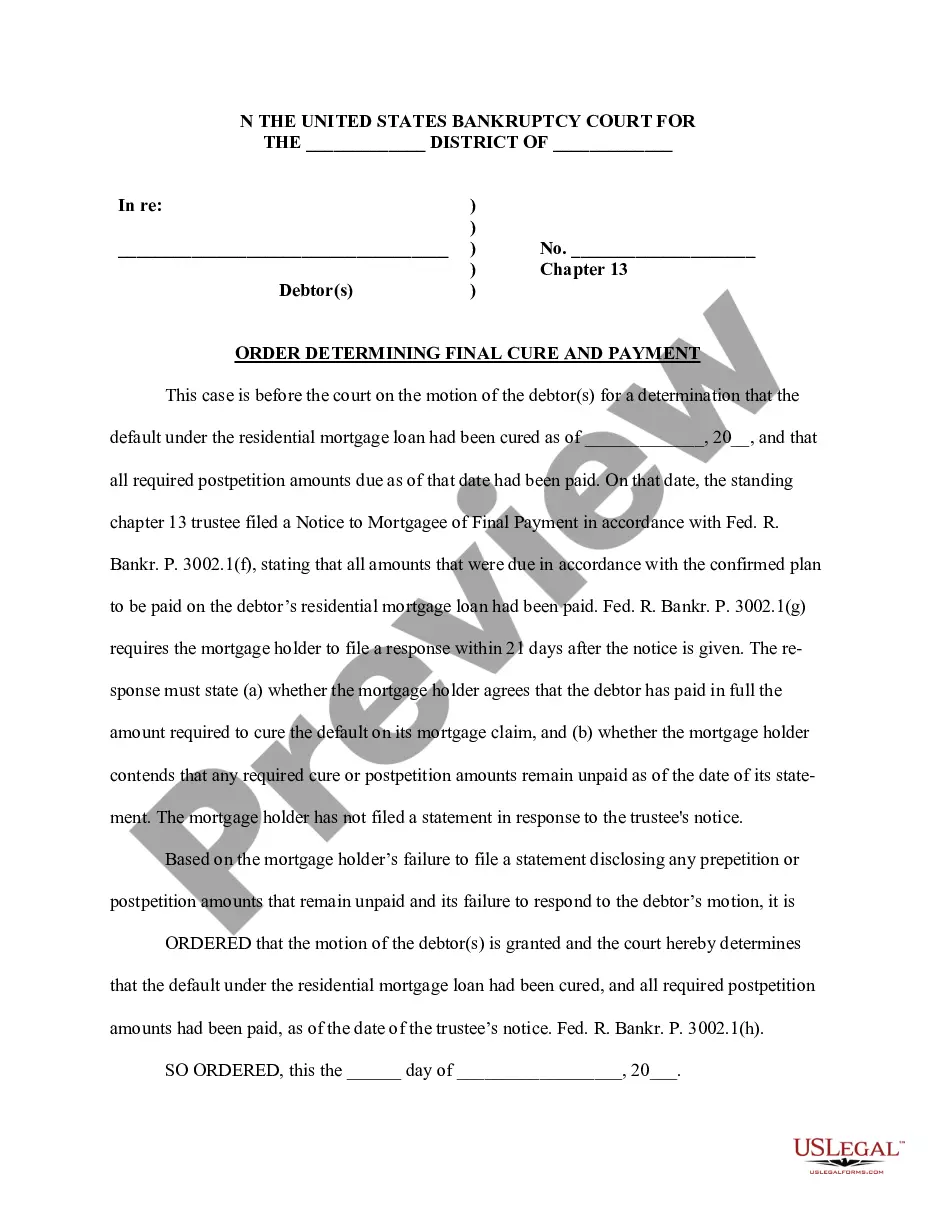

The Motion to Determine Final Cure and Payment is a legal document used in bankruptcy cases, specifically under Chapter 13. This form serves to request the court to confirm that a borrower has cured any defaults on a residential mortgage loan and that all necessary payments have been made. This motion also indicates that the mortgagee agrees with the trustee's notice regarding these payments, distinguishing it from other motions in bankruptcy proceedings.

Key parts of this document

- The basic information about the court and case number.

- A notice of the opportunity to object and for hearing.

- Representation of the mortgage holder and payment status.

- A section for observing the response timelines for objections.

- Certification of service indicating who received copies of the motion.

")

")

When this form is needed

This form is essential when a debtor believes they have remedied any defaults on their mortgage during a bankruptcy proceeding. It is used when the mortgagee's response aligns with the trustee's notice of postpetition payment status, particularly following the deadlines established in bankruptcy procedure rules.

Who this form is for

- Debtors who are undergoing Chapter 13 bankruptcy and have a residential mortgage.

- Mortgagees who agree with the trusteeâs notice of payment.

- Attorneys representing debtors or mortgagees in bankruptcy cases.

Instructions for completing this form

- Provide the case caption information, including the court name and debtor's details.

- Fill in the date when the debt is considered cured.

- Specify the mortgage holder's name and their acknowledgment of payment receipt.

- Enter any additional allegations or statements relevant to the motion.

- Complete the certificate of service to indicate who received the documents and how.

Is notarization required?

This form does not typically require notarization unless specified by local law. Always check state regulations to ensure compliance.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to provide accurate case details.

- Missing the deadlines for opposing the motion.

- Neglecting to properly serve the motion to interested parties.

- Not including a lawyer's signature if applicable.

Benefits of completing this form online

- Convenience of downloading and filling out from anywhere.

- Easy editing of the document as needed before submission.

- Access to templates drafted by licensed attorneys ensuring compliance with legal standards.

- Time-efficient process versus traditional methods of obtaining legal forms.

Quick recap

- The Motion to Determine Final Cure and Payment is essential for clarifying mortgage defaults in Chapter 13 bankruptcy.

- Timely filing and accuracy are crucial to ensure the court recognizes the cure of payments.

- Employing this form can streamline the resolution of mortgage issues during bankruptcy proceedings.

Looking for another form?

Form popularity

FAQ

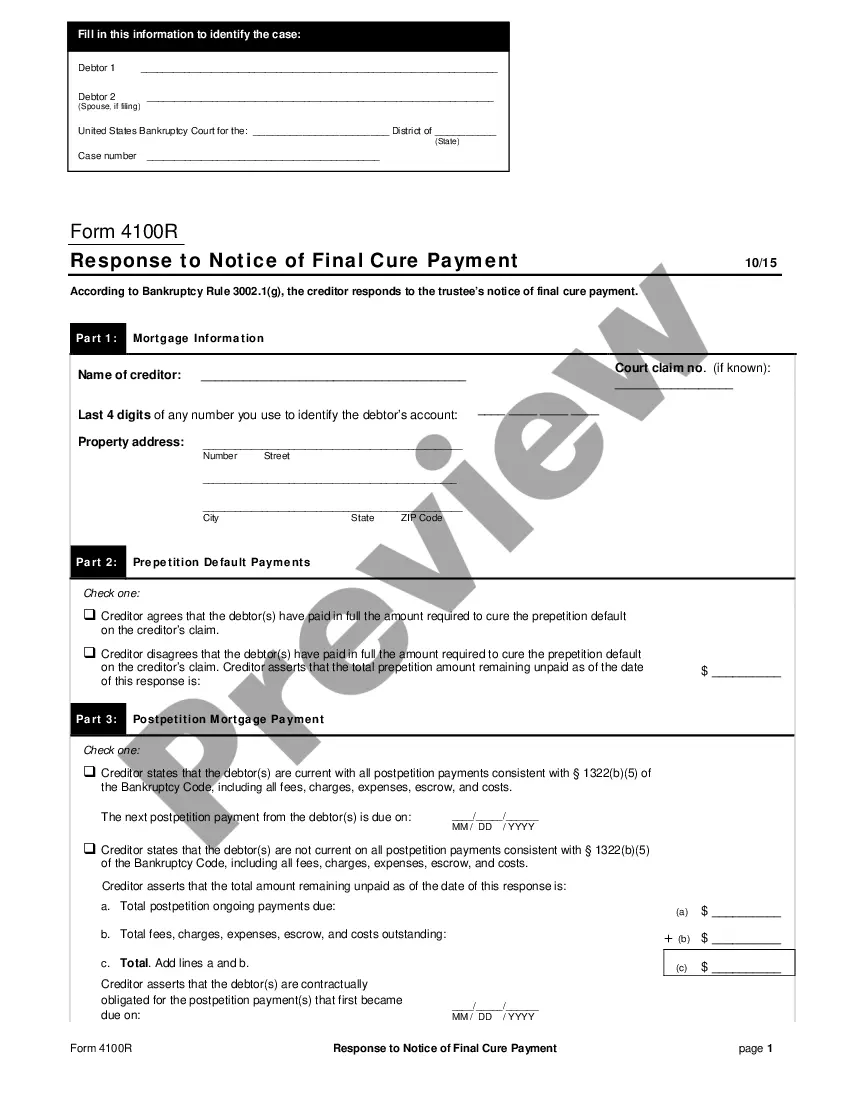

Creditors must file a response to the notice of final cure payment within 21 days after service of the notice. This response will state whether the creditor agrees that all arrears have been paid. The response will also state whether any post-petition amounts under the mortgage loan remain unpaid.

Bankruptcy Rule 3002.1(g) provides that once the trustee files a Notice of Final Cure of mortgage payments, a mortgage lender must file a response within 21 days indicating whether it agrees that the arrears have been fully cured and whether payments are current.

Cure Payment means the payment of Cash or the distribution of other property (as the parties may agree or the Bankruptcy Court may order) that is necessary to cure any and all defaults under an executory contract or unexpired lease so that such contract or lease may be assumed, or assumed and assigned, pursuant to

Cure Amounts means all amounts, costs and expenses required by the Bankruptcy Court to cure all defaults and other amounts outstanding under the Assumed Contracts and Additional Assumed Contracts to the extent required so that they may be assumed by the applicable Selling Entities and assigned to Buyer pursuant to

Overview. A Notice of Final Cure Mortgage Payment is filed by the trustee within 30 days of the date the debtor completes all payments under the plan. The purpose of the notice is to state whether the debtor has paid the full amount required to cure the mortgage default.

Stopping the Foreclosure Process Once the foreclosure process has started, a property owner, or another lienholder, may stop the process by ?curing? the default. A written Notice of Intent to Cure must be filed with the Public Trustee's Office no later than 15 days prior to the scheduled sale date.

The discharge releases the debtor from all debts provided for by the plan or disallowed (under section 502), with limited exceptions. Creditors provided for in full or in part under the chapter 13 plan may no longer initiate or continue any legal or other action against the debtor to collect the discharged obligations.