Qualifying Subchapter-S Revocable Trust Agreement

About this form

The Qualifying Subchapter-S Revocable Trust Agreement is a legal document designed to establish a Qualified Subchapter S Trust (QSST). This type of trust allows beneficiaries, who are typically different from the grantor, to enjoy significant income tax and estate tax benefits while allowing the trustor to maintain control over the assets during their lifetime. Unlike other S corporation trusts, a QSST ensures that income generated by the trust is reported directly to the beneficiary, which can lead to favorable tax implications.

Key components of this form

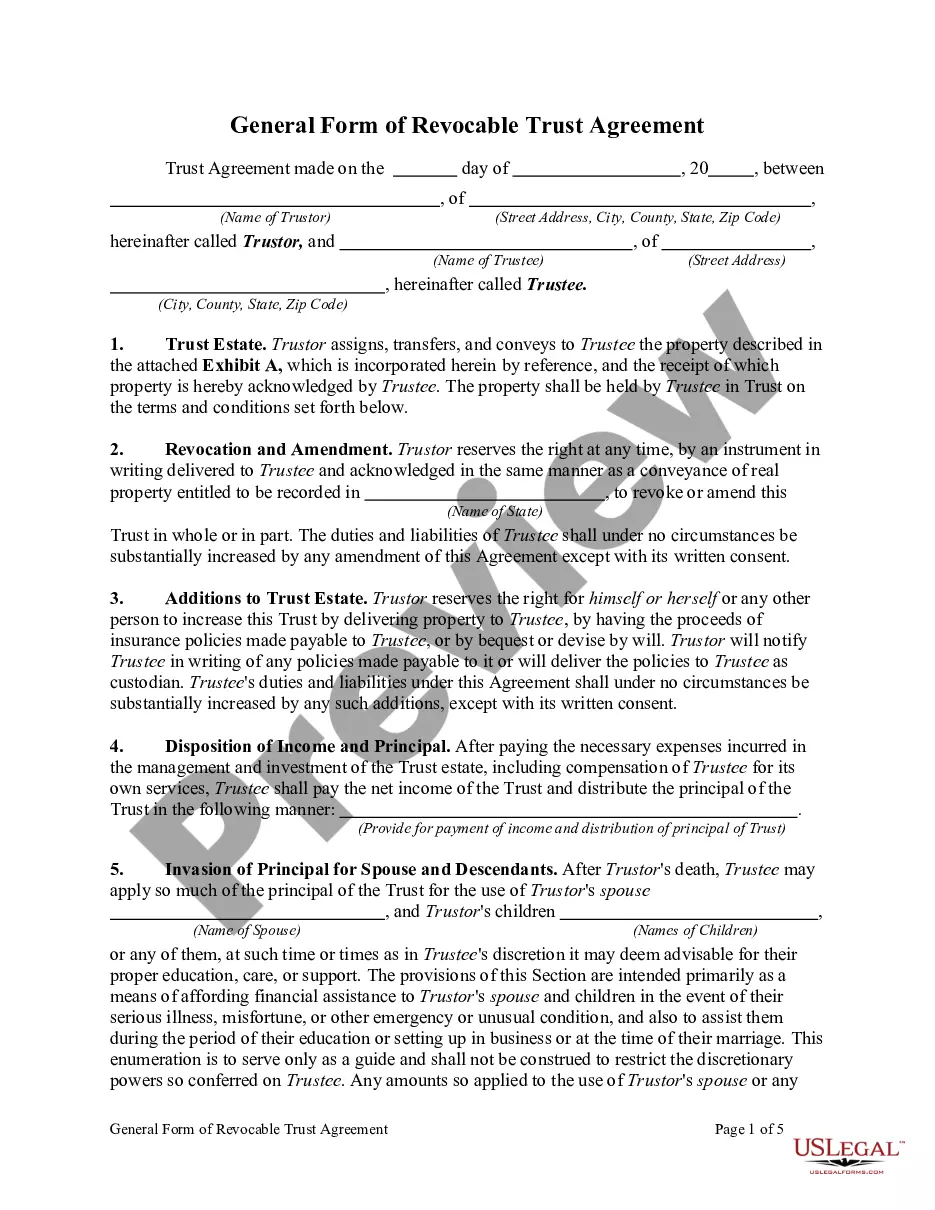

- Identification of parties, including the Trustor and Trustee.

- Transfer of property and life insurance proceeds to the Trustee.

- Rights reserved by the Trustor to amend or revoke the trust agreement.

- Distribution terms for income and principal to beneficiaries.

- Rules regarding successor Trustees and management powers.

- Spendthrift provisions protecting the trust from creditors of the beneficiaries.

When to use this document

This form is essential when an individual wishes to establish a trust that qualifies as a QSST, primarily to provide income tax and estate tax advantages. It is applicable in situations such as securing a stream of income for a beneficiary while maintaining control over the trust assets or managing assets in a tax-efficient manner. This agreement is particularly useful when the grantor wishes to separate the legal ownership of assets from the personal ownership to minimize tax liabilities.

Who should use this form

- Individuals looking to create a trust to benefit specific beneficiaries.

- Individuals aiming to achieve tax savings through a Qualified Subchapter S Trust.

- Trustors who want to maintain control over trust assets during their lifetime.

- Those seeking to provide continued financial support to dependents or individuals with special needs.

Completing this form step by step

- Identify the parties by entering the names and addresses of the Trustor and Trustee.

- List the property being transferred to the trust in the designated sections.

- Specify the name of the trust as well as the current income beneficiary.

- Detail the conditions under which distributions will be made to the beneficiaries.

- Ensure all parties sign and date the form as required for validity.

Does this form need to be notarized?

Notarization is generally not required for this form. However, certain states or situations might demand it. You can complete notarization online through US Legal Forms, powered by Notarize, using a verified video call available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to clearly identify all parties and beneficiaries involved in the trust.

- Not specifying the correct terms for distribution of income and principal.

- Omitting to keep copies of all amendments to the trust agreement.

- Neglecting to update the trust with changes in personal circumstances or state law.

Benefits of using this form online

- Convenience of accessing and completing the form from anywhere at any time.

- Editability allows users to tailor the document to their specific needs.

- Reliable templates drafted by licensed attorneys ensure legal compliance.

- Secure download and easy storage options for personal records.

What to keep in mind

- The QSST offers tax benefits and is designed for specific income beneficiaries.

- Clear identification of parties and provisions is critical for validity.

- Proper execution and adherence to local laws enhance the enforceability of this trust agreement.

Looking for another form?

Form popularity

FAQ

Only estates, individuals, and certain trusts can own shares in an S corp. Corporations, partnerships, and non-resident aliens cannot own stock.If the trust is a grantor trust, testamentary trust, qualified Subchapter S trust (QSST), revocable trust, or retirement account trust, the trust counts as one shareholder.

Houses and other real estate (even if they're mortgaged) stock, bond, and other security accounts held by brokerages (but think about naming a TOD beneficiary instead) small business interests (stock in a closely held corporation, partnership interests, or limited liability company shares)

Generally, estates and six types of trusts are eligible as S corporation shareholders, these include grantor trusts, electing small business trusts (ESBTs), qualified subchapter S trusts (QSSTs), and testamentary trusts (for two years after funding.

1361(d)(3), for a trust to qualify as a QSST, its terms must require that during the life of the current income beneficiary, the trust will have only one income beneficiary; and all of the trust's accounting income must either be required by the terms of the trust instrument to be distributed, or actually be

A Qualified Subchapter S Trust, commonly referred to as a QSST Election, or a Q-Sub election, is a Qualified Subchapter S Subsidiary Election made on behalf of a trust that retains ownership as the shareholder of an S corporation, a corporation in the United States which votes to be taxed.

While there can only be one income beneficiary, a QSST may designate successor beneficiaries. With an ESBT, you can set up one trust that includes all of the income beneficiaries. However, note that any ESBT designated beneficiaries must be an individual, estate or charity eligible to own S corporation stock.

In order to become an S corporation, the corporation must submit a completed Form 2553 (Election by a Small Business Corporation) that has been signed by all the shareholders. The following information must be provided: The corporation's name and address. The tax year when the election will take effect.

A Qualified Subchapter S Trust, commonly referred to as a QSST Election, or a Q-Sub election, is a Qualified Subchapter S Subsidiary Election made on behalf of a trust that retains ownership as the shareholder of an S corporation, a corporation in the United States which votes to be taxed.

Only estates, individuals, and certain trusts can own shares in an S corp.If the trust is a grantor trust, testamentary trust, qualified Subchapter S trust (QSST), revocable trust, or retirement account trust, the trust counts as one shareholder.