Irrevocable Trust which is a Qualifying Subchapter-S Trust

Overview of this form

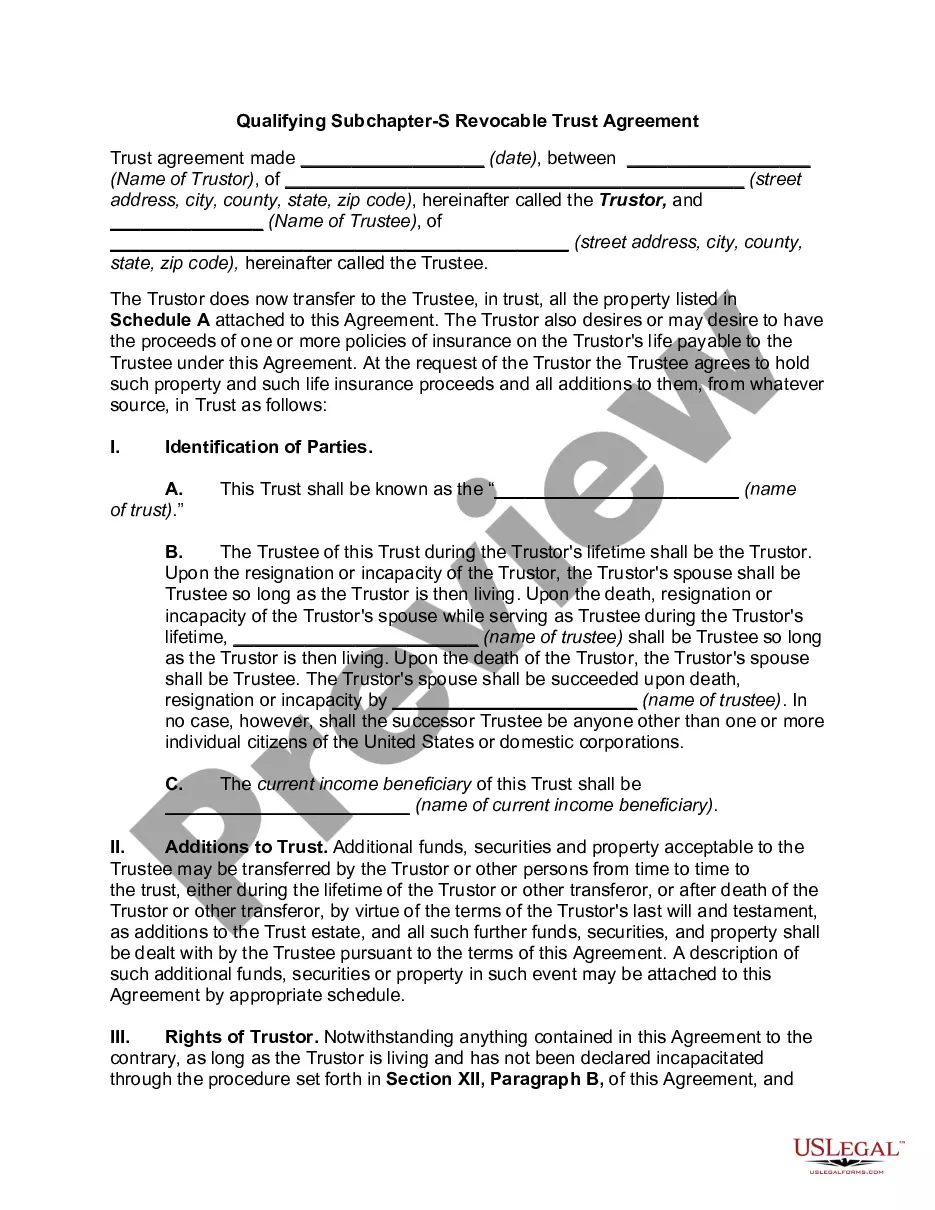

The Irrevocable Trust which is a Qualifying Subchapter-S Trust is a legal arrangement in which the grantor transfers assets into a trust that cannot be modified or terminated without the consent of the beneficiaries. This form serves to establish a trust that meets specific IRS requirements to be classified as a Subchapter-S Trust, allowing certain tax benefits while ensuring that the assets remain protected from the grantorâs creditors. Unlike revocable trusts, this trust type is permanent in nature and cannot be altered after its creation.

Key components of this form

- Transfer of assets from the grantor to the trustee, detailing the property to be included.

- Provisions for the payment of income and the distribution of principal to the designated beneficiary.

- Clear definitions of the rights and restrictions of the grantor, ensuring that the trust remains irrevocable.

- Powers and duties of the trustee, including authority over the management and investment of trust property.

- Succession planning for trustee roles and conditions under which alternate trustees can be appointed.

Common use cases

This form is typically used when an individual wants to create an irrevocable trust to manage their assets for the benefit of a specific beneficiary while taking advantage of certain tax benefits. It is particularly relevant for those looking to ensure long-term asset protection and maintain control over how assets are used for the beneficiary's health, education, and support without retaining ownership of the assets.

Intended users of this form

- Individuals seeking to establish a permanent trust for their beneficiaries.

- Individuals desiring tax advantages associated with a Subchapter-S Trust.

- Estate planners and financial advisors managing client assets.

- Grantors who wish to protect their assets from creditors and secure benefits for their heirs.

How to prepare this document

- Identify the parties involved: the grantor and the trustee, including their respective addresses.

- Specify the assets being transferred into the trust, outlining them in an attached Schedule A.

- Designate the beneficiary and outline how income and principal will be transferred during their lifetime.

- Document any powers you wish to grant the trustee regarding managing the trust assets.

- Include any provisions regarding successor trustees and their powers in case the original trustee is unavailable.

Notarization requirements for this form

This form does not typically require notarization unless specified by local law.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to clearly describe the assets in Schedule A, which can lead to disputes later.

- Not specifying the beneficiaryâs age for distributions, causing ambiguity when the beneficiary becomes of age.

- Overlooking to include necessary provisions for trustee succession, which might complicate management of the trust.

- Assuming IRS regulations are automatically met without explicit elections for qualifying as a Subchapter-S Trust.

Benefits of completing this form online

- Immediate access to a properly formatted and legally compliant trust agreement.

- Editability allows for customization according to specific needs and preferences.

- Secure document management, ensuring sensitive information remains protected.

- Guidance provided throughout the completion process, making it easier for individuals without legal experience.

Legal use & context

- This trust is legally enforceable and must adhere to IRS requirements for a Qualified Subchapter-S Trust.

- Failure to comply with the regulations can lead to tax disadvantages or invalidation of trust provisions.

- Consulting legal counsel is advisable to ensure compliance with specific state laws and regulations.

Summary of main points

- An irrevocable trust cannot be altered or revoked without the beneficiary's consent.

- This form provides tax advantages and protects assets for beneficiaries.

- Accurate completion and notarization are crucial for the formâs validity.

Looking for another form?

Form popularity

FAQ

Generally, estates and six types of trusts are eligible as S corporation shareholders, these include grantor trusts, electing small business trusts (ESBTs), qualified subchapter S trusts (QSSTs), and testamentary trusts (for two years after funding.

Only estates, individuals, and certain trusts can own shares in an S corp. Corporations, partnerships, and non-resident aliens cannot own stock.If the trust is a grantor trust, testamentary trust, qualified Subchapter S trust (QSST), revocable trust, or retirement account trust, the trust counts as one shareholder.

Generally, estates and six types of trusts are eligible as S corporation shareholders, these include grantor trusts, electing small business trusts (ESBTs), qualified subchapter S trusts (QSSTs), and testamentary trusts (for two years after funding.

A Qualified Subchapter S Trust, commonly referred to as a QSST Election, or a Q-Sub election, is a Qualified Subchapter S Subsidiary Election made on behalf of a trust that retains ownership as the shareholder of an S corporation, a corporation in the United States which votes to be taxed.

A Qualified Subchapter S Trust, commonly referred to as a QSST Election, or a Q-Sub election, is a Qualified Subchapter S Subsidiary Election made on behalf of a trust that retains ownership as the shareholder of an S corporation, a corporation in the United States which votes to be taxed.

While there can only be one income beneficiary, a QSST may designate successor beneficiaries. With an ESBT, you can set up one trust that includes all of the income beneficiaries. However, note that any ESBT designated beneficiaries must be an individual, estate or charity eligible to own S corporation stock.

Only estates and certain types of trusts can own shares of an S corporation.An irrevocable trust that is setup as a grantor trust, qualified subchapter S trust or as an electing small business trust may own shares of an S corporation.

Testamentary trusts. This trust type is established by your will. It's an eligible S corporation shareholder for up to two years after the transfer and then must either distribute the stock to an eligible shareholder or qualify as a QSST or ESBT.

A trust can hold stock in an S corp only if it (1) is treated as owned by its grantor for income tax purposes under us grantor trust rules, (2) was a grantor trust immediately before its grantor's death (the trust can be a shareholder only for two years from that date), (3) received stock from the will of a decedent (