General Guaranty and Indemnification Agreement

Understanding this form

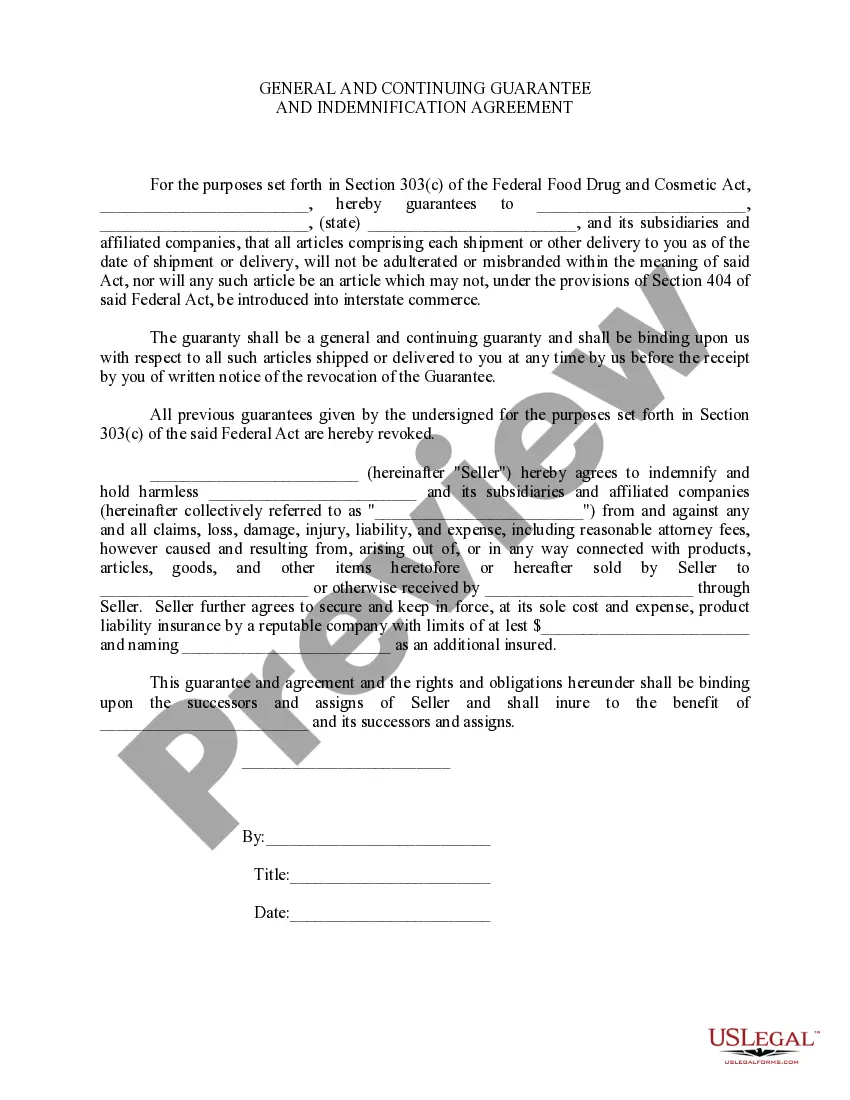

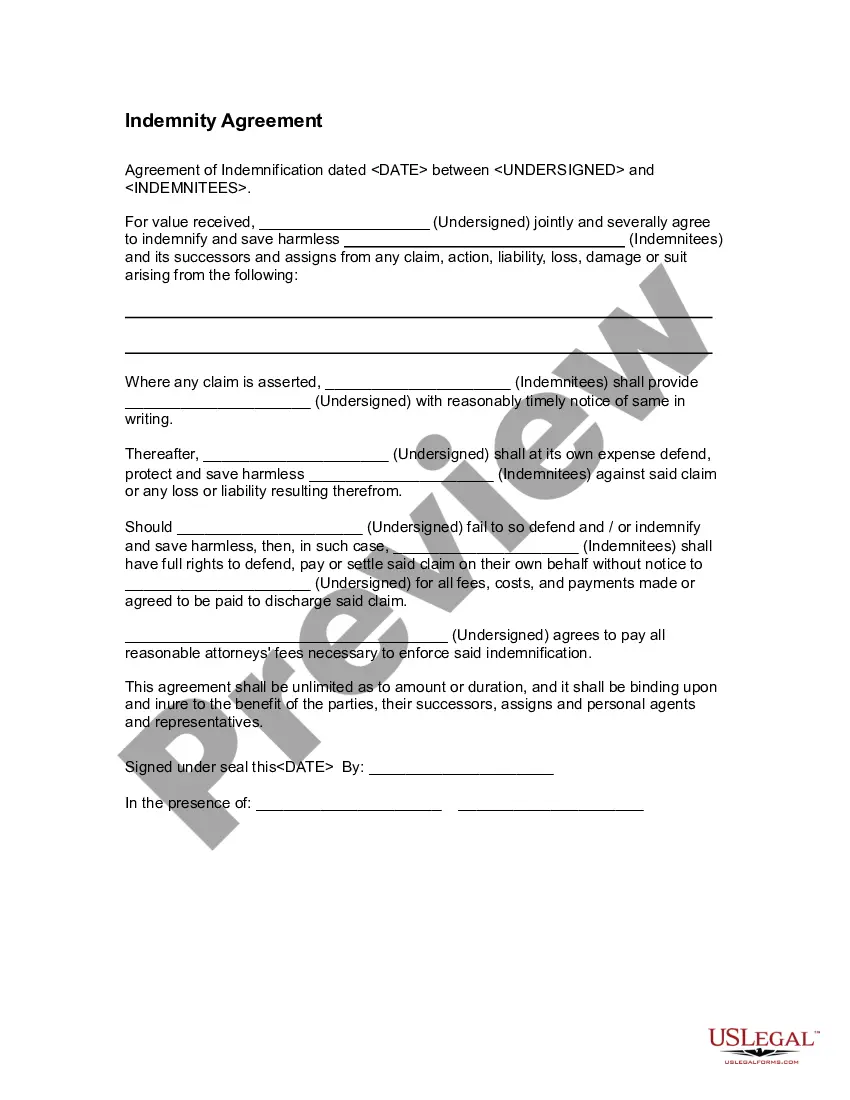

The General Guaranty and Indemnification Agreement is a legal document in which a guarantor agrees to unconditionally guarantee the obligations of a seller, protecting the seller from potential losses or claims. This form differs from other agreements in that it not only secures the seller's interests but also includes an indemnification clause, which holds the indemnitor responsible for any damages that may arise, including attorney's fees. It is essential for situations where a guarantor wants to affirm their commitment to cover obligations if the primary party fails to do so.

What’s included in this form

- Parties involved: Identifies the guarantor, indemnitor, and seller.

- Guarantee clause: Clearly states the obligations being guaranteed.

- Indemnification provision: Specifies the indemnitor's responsibilities for damages or losses.

- Waiver of notices: The guarantor waives the right to receive various notices related to the agreement.

- Duration of guarantee: Indicates the period during which the guaranty is effective.

- Governing law: Establishes which state's laws will govern the agreement.

When to use this document

This form should be used when a seller wants assurance that they will be compensated for any potential losses stemming from the actions or inactions of the purchaser. Typical scenarios include real estate transactions, business loans, or any contractual obligations where the seller seeks added security. It can also be relevant for personal guarantees related to leases or service agreements.

Who needs this form

Individuals or entities should consider using this form if they are:

- A seller who wants additional protection against non-performance by a purchaser.

- A guarantor who is willing to take on financial responsibility for the obligations of others.

- An indemnitor looking to secure the seller from possible claims or damages.

Steps to complete this form

- Identify all parties involved: clearly list the names of the guarantor, indemnitor, and seller.

- Fill in the specific obligations being guaranteed, ensuring clarity on what the guarantee covers.

- Enter the duration for which the guaranty will remain effective.

- Ensure the indemnification section accurately reflects the responsibilities of the indemnitor.

- Include the applicable state laws that govern the agreement.

- Collect signatures from all parties, including notarization if required by law.

Notarization requirements for this form

This form must be notarized to be legally valid. US Legal Forms provides secure online notarization powered by Notarize, allowing you to complete the process through a verified video call.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to identify all parties correctly can lead to enforcement issues.

- Using vague language in the obligations section may create confusion later.

- Not specifying the duration of the guarantee can result in disputes.

- Neglecting to consider local state laws can affect the document's validity.

Why use this form online

- Convenient access: Download the form anytime without the need for physical paperwork.

- Editability: Tailor the form to your specific needs and requirements easily.

- Reliability: Use forms drafted by licensed attorneys to ensure legal compliance.

Key takeaways

- The General Guaranty and Indemnification Agreement protects sellers from potential losses.

- It emphasizes the unconditional nature of the guarantor's responsibilities.

- Careful completion, including notarization, is essential for the validity of the form.

Looking for another form?

Form popularity

FAQ

The guarantee and indemnity will provide that, in the event the borrower fails to perform its obligations under the loan, the lender can ask the guarantor to carry out the obligations on the borrower's behalf. A guarantee and indemnity is generally required where the borrower is a high credit risk.

The key differences between guarantees and indemnities include: a guarantee is a secondary liability, which means that there will be another person who is primarily liable for the obligation; whereas, an indemnity imposes a primary liability.a guarantor's liability is limited by the extent of the debtor's liability.

In a contract of indemnity, there is a single promise or contract; a promise to pay if there is a loss. In a contract of guarantee, by contrast, there are multiple promises, including the original promise to pay or perform and the guarantor's promise to pay or perform in the event of default.

When the term indemnity is used in the legal sense, it may also refer to an exemption from liability for damages. Indemnity is a contractual agreement between two parties. In this arrangement, one party agrees to pay for potential losses or damages caused by another party.

Liability: In a contract of indemnity, the liability of the indemnifier is primary (Fire Insurance), whereas in a contract of guarantee, the debtor is primarily liable, and the surety assumes secondary liability because the customer is primary liable in default of his payment then after the surety has liability.

A guarantor is a person, third party or organisation that agrees to guarantee your loan. The guarantee is a legal assurance given by the guarantor to pay the loan if the borrower defaults and is unable to pay.

Unlike a guarantee, an indemnity need not be in writing or signed by the indemnifier in order to be effective. More robust. Being a primary obligation, an indemnity will be valid even if the underlying transaction is set aside; unlike a guarantee, which is dependent on the underlying transaction.