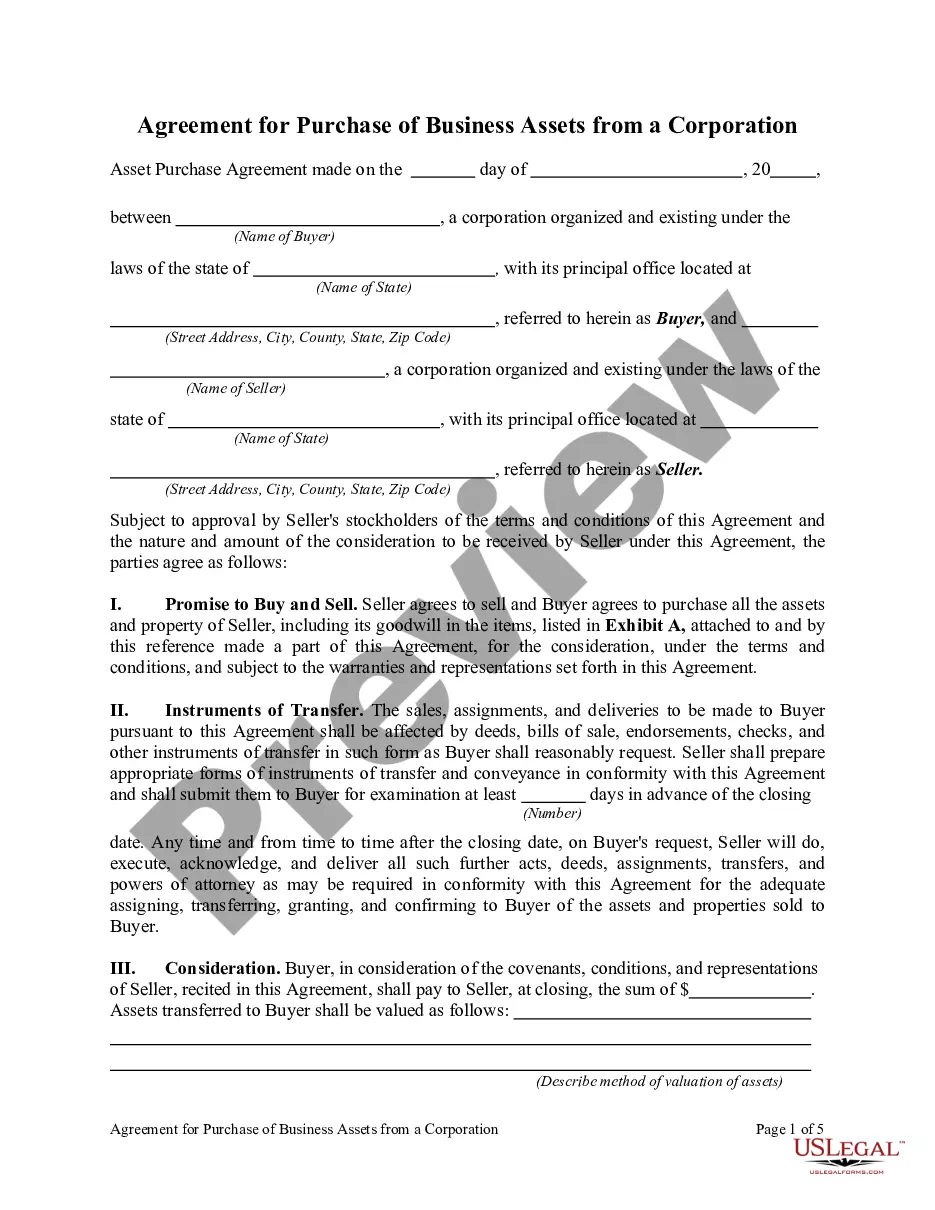

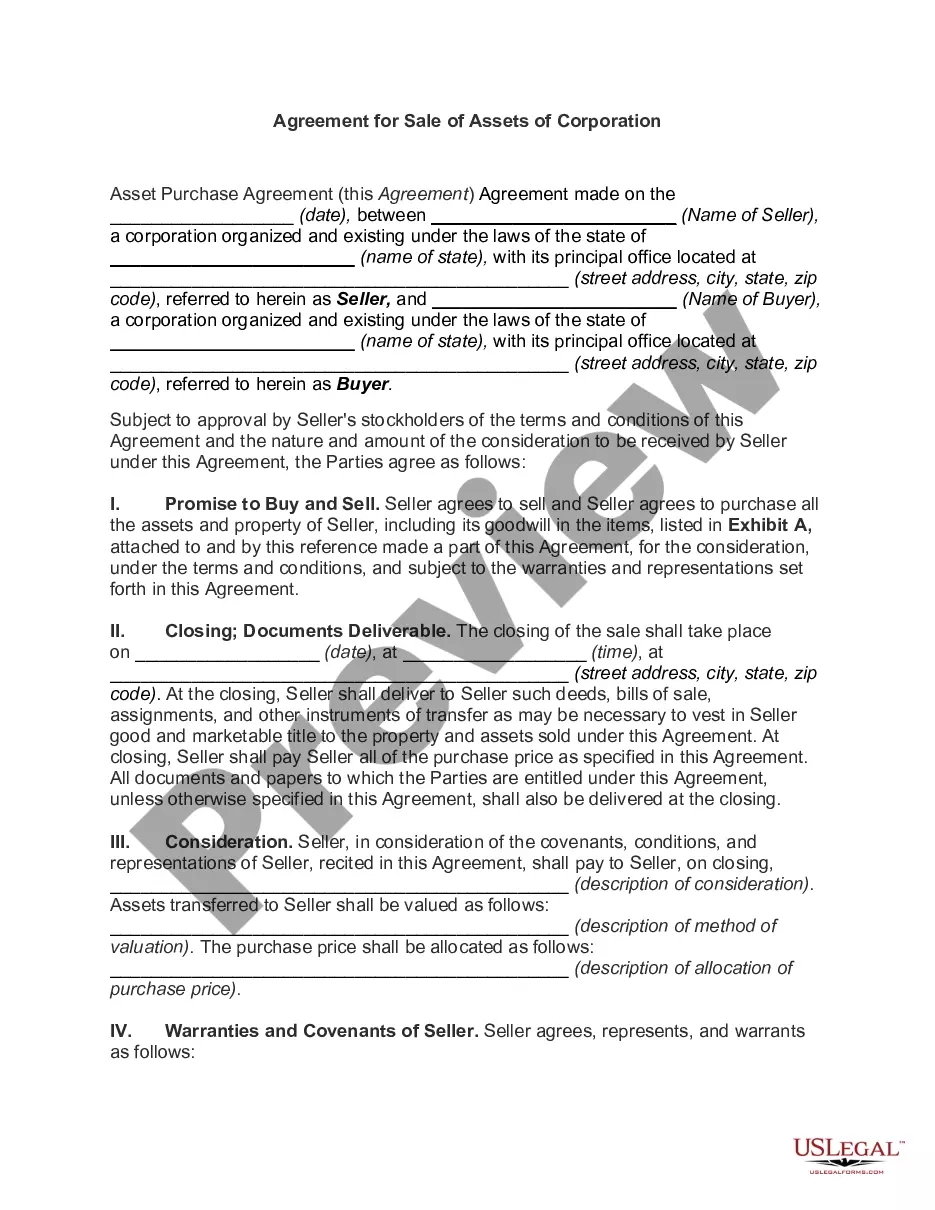

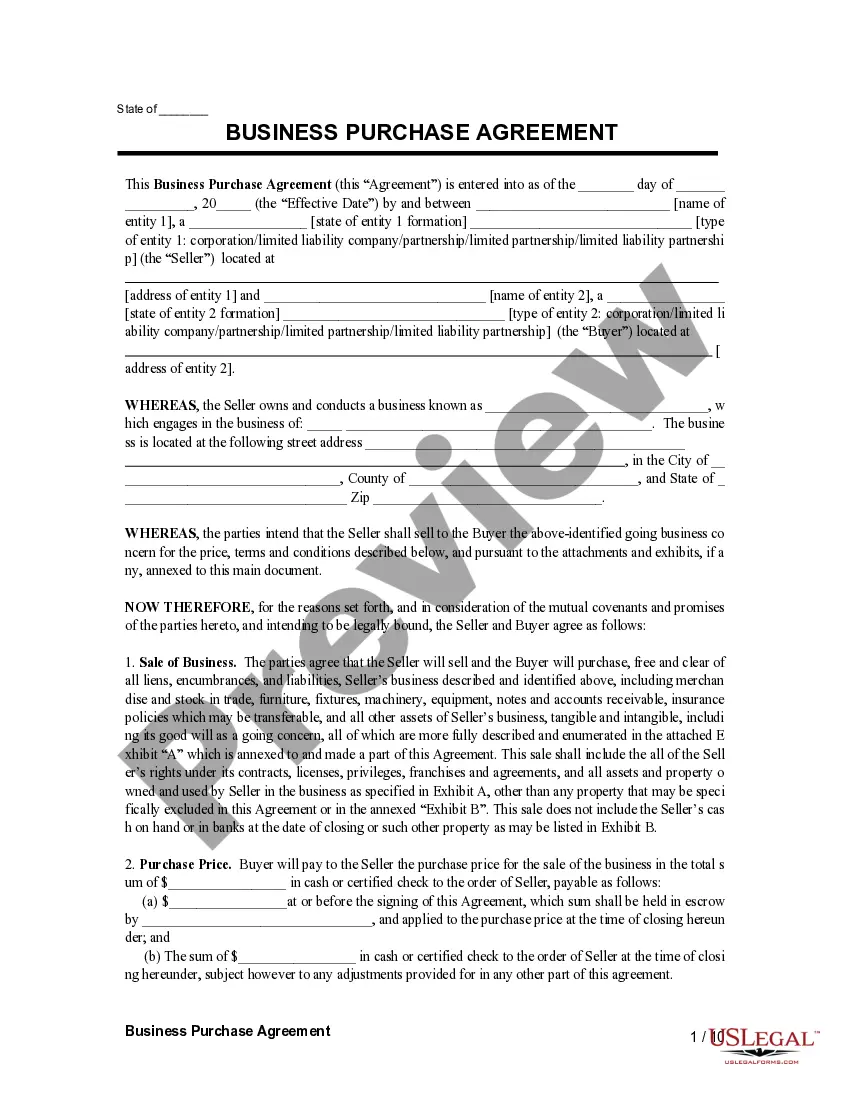

District of Columbia Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets

Description

How to fill out Agreement For Sale Of All Assets Of A Corporation With Allocation Of Purchase Price To Tangible And Intangible Business Assets?

You have the capability to spend time online searching for the authentic document template that meets the federal and state requirements you have.

US Legal Forms offers thousands of valid documents that are reviewed by experts.

You can download or print the District of Columbia Agreement for Sale of All Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets from the platform.

If available, utilize the Review button to preview the document template as well.

- If you already possess a US Legal Forms account, you can Log In and press the Acquire button.

- After that, you can complete, modify, print, or sign the District of Columbia Agreement for Sale of All Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets.

- Each legal document template you purchase is yours permanently.

- To obtain another version of the purchased form, visit the My documents tab and click the relevant button.

- If you are using the US Legal Forms website for the first time, follow the simple instructions outlined below.

- First, ensure you have selected the correct document template for the county or city of your choice.

- Review the form description to confirm you have chosen the right template.

Form popularity

FAQ

Yes, you can file DC Form D-30 electronically, streamlining the process and ensuring timely submissions. Online filing options are available and can help simplify your reporting responsibilities, particularly for transactions involving the District of Columbia Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets. Consider using these electronic options to enhance efficiency and accuracy in your filing.

Any business entity, including partnerships, corporations, and certain individuals, that earns income from sources within the District of Columbia must file a DC tax return. This requirement ensures that all businesses, especially those engaged in actions like the District of Columbia Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets, report their earnings comprehensively. Consulting a tax professional can help clarify your specific obligations.

Yes, the sale of intangible assets, such as trademarks or copyrights, can be classified as a capital gain. This classification typically arises if the assets were held for investment purposes, separate from the District of Columbia Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets. It's wise to seek professional tax advice to understand how these sales will impact your overall tax situation.

DC tax form D-30 is specifically designed for corporate income reporting in the District of Columbia. It requires businesses to detail their income, deductions, and other financial specifics that may relate to transactions, such as the District of Columbia Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets. Correct completion of this form is essential to avoid penalties and ensure compliance.

Corporations that conduct business in the District of Columbia must file DC form D-30. This includes both domestic and foreign corporations earning income in D.C. If your transaction involves the District of Columbia Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets, your filing obligations may include completing the D-30 to ensure accurate tax reporting.

The D-30 is a tax form used by corporations that operate within the District of Columbia. This form captures corporate income and applicable deductions, specifically those relating to transactions, like the District of Columbia Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets. Understanding the D-30 can be crucial for compliance and accurate reporting of your business transactions.

Individuals who do not meet specific thresholds in income or asset ownership often do not need to file form 10iea. For instance, if your organization does not operate in a certain capacity or lacks substantial business activities related to the District of Columbia Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets, you might qualify for exemption. It's vital to consult a tax professional to determine your obligations accurately.

The DC D 20 form is a corporate income tax return required for corporations operating in the District of Columbia. This form helps the government assess the corporation's tax liability accurately. When preparing a District of Columbia Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets, understanding the D 20 form is crucial because it may affect the financial considerations of the sale. To streamline this process, uslegalforms provides access to templates and guidance on fulfilling these requirements.

Yes, the District of Columbia recognizes S-corporations. These corporations allow for pass-through taxation, meaning profits and losses pass directly to shareholders, avoiding double taxation. This recognition can be beneficial when drafting a District of Columbia Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets, as it influences how the sale and allocation of assets are treated tax-wise. If you need assistance navigating this process, uslegalforms offers resources tailored for such agreements.