Alabama Deed with Mortgage Assumption

What is this form?

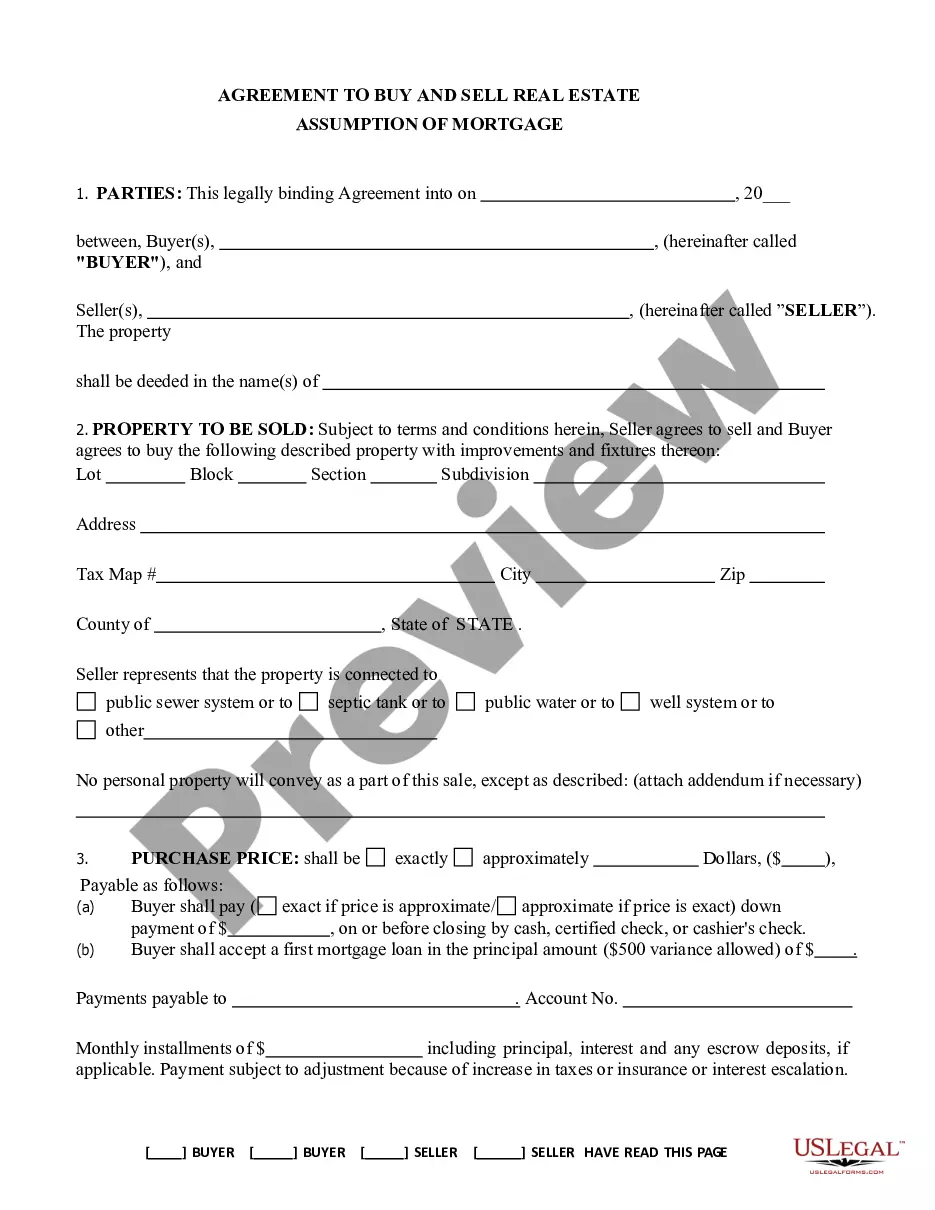

The Deed with Mortgage Assumption is a legal document used to transfer ownership of property to a new owner, or grantee, who agrees to assume the responsibility for any remaining mortgage debt on the property. This form is essential when the seller wants to pass on the mortgage obligations to the buyer, allowing for a smoother transition of ownership without refinancing the loan. Unlike a standard deed, this form includes specific clauses regarding the mortgage assumption, ensuring all parties are aware of their responsibilities regarding the outstanding balance.

Key parts of this document

- Identification of the grantor (current property owner) and grantee (new property owner).

- Details of the mortgage to be assumed, including the lender's information.

- Legal description of the property being conveyed.

- Statement affirming the grantee's agreement to assume the mortgage debt.

- Signatures of both parties, along with necessary notarization.

When to use this document

This form is typically used in real estate transactions where the buyer intends to take over the existing mortgage of the property. It is beneficial in situations where the current mortgage terms are favorable, and the buyer is unable or unwilling to secure new financing. Examples include family transfers, sales among friends, or situations where the seller is relocating and wishes to simplify the sale process.

Who can use this document

- Homeowners looking to transfer property ownership while passing along the existing mortgage.

- Buyers interested in purchasing property with an assumable mortgage.

- Real estate agents facilitating transactions involving mortgage assumptions.

- Legal professionals assisting clients in real estate matters involving property transfers.

How to complete this form

- Identify the parties involved, including the full names of the grantor and grantee.

- Provide the exact address and legal description of the property being transferred.

- State the details of the existing mortgage that the grantee will assume, including the lender's information.

- Have both the grantor and grantee sign the document and affix their initials where required.

- Arrange for notarization of the form to validate the authenticity of the signatures.

Notarization requirements for this form

This document requires notarization to meet legal standards. US Legal Forms provides secure online notarization powered by Notarize, allowing you to complete the process through a verified video call, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to include the full legal description of the property.

- Not having the document notarized, leading to potential legal issues.

- Incorrectly identifying the parties involved.

- Overlooking the specifics of the mortgage debt being assumed.

Advantages of online completion

- Immediate access to a professionally drafted legal document.

- Convenience of filling out the form at your own pace.

- Editability to ensure all information is correct before final submission.

- Availability of assistance and support as needed during the process.

Quick recap

- The Deed with Mortgage Assumption is essential for property transfers where the buyer assumes the mortgage.

- It is important to include accurate details about the parties and property to avoid legal issues.

- Notarization is required to validate the deed and protect all parties involved.

Looking for another form?

Form popularity

FAQ

You can transfer a mortgage to another person if the terms of your mortgage say that it is assumable. If you have an assumable mortgage, the new borrower can pay a flat fee to take over the existing mortgage and become responsible for payment. But they'll still typically need to qualify for the loan with your lender.

You can transfer a mortgage to another person if the terms of your mortgage say that it is assumable. If you have an assumable mortgage, the new borrower can pay a flat fee to take over the existing mortgage and become responsible for payment. But they'll still typically need to qualify for the loan with your lender.

No law forbids adding someone to your mortgaged home's deed or in signing your home over to others through one. Mortgage lenders understand deeds, though, and use loan due-on-sale clauses to prevent unauthorized property sales or transfers.

It is possible to be named on the title deed of a home without being on the mortgage. However, doing so assumes risks of ownership because the title is not free and clear of liens and possible other encumbrances.If a mortgage exists, it's best to work with the lender to make sure everyone on the title is protected.

It is important to note that a quitclaim deed has no effect on a mortgage. A quitclaim transfers a property's title but any mortgage the grantor has will not transfer.

To give the house but keep the mortgage, the parents need permission from the mortgage lender. (And, in the previous example, the value of the gift is $1 million if the mortgage stays with the parents.)

Contact the current lender to request assumption information. Calculate how much you must pay upfront. Qualify with the lender. Pay the down payment, closing fees and mortgage buyout costs. Attend the closing.

The law doesn't forbid adding people to a deed on a home with an outstanding mortgage. Mortgage lenders are familiar and frequently work with deed changes and transfers.When you "deed" your home to someone, you've effectively transferred part ownership, which could activate the "due-on-sale" clause.