Letter Engagement Statement Format Icai In Cook

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Standards on Review Engagements establish requirements and provide application and other explanatory material on the responsibilities of an auditor, or assurance practitioner, when engaged to undertake a review engagement and on the form and content of the auditor's, or assurance practitioner's, review report.

Standard on Assurance Engagements (SAE) 3400, “The Examination of Prospective Financial Information” should be read in the context of the “Preface to the Standards on Quality Control, Auditing, Review, Other Assurance and Related Services”1, which sets out the authority of the Engagement Standards.

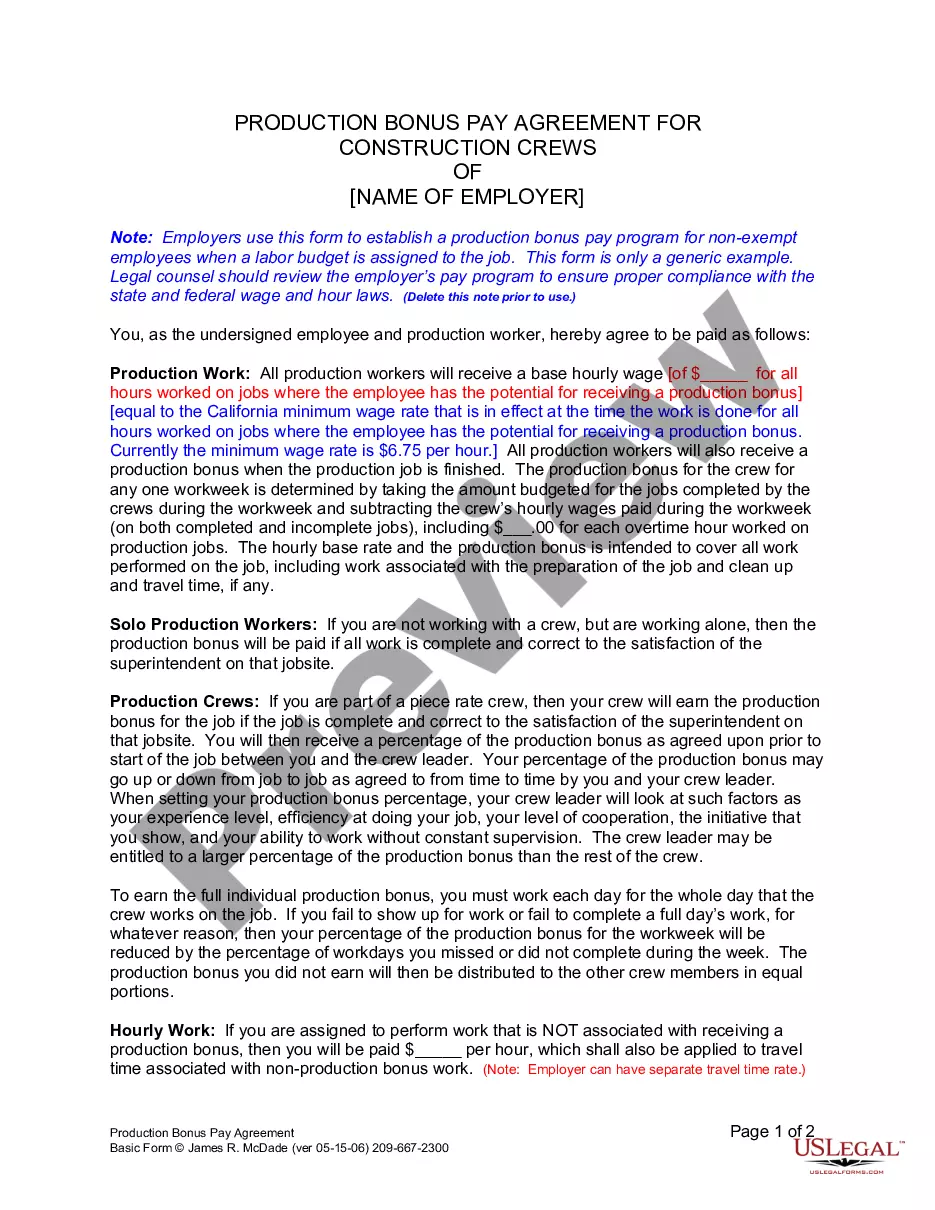

An engagement letter is a written agreement that describes the business relationship to be entered into by a client and a company. The letter details the scope of the agreement, its terms, and costs. The purpose of an engagement letter is to set expectations on both sides of the agreement.

To help you protect yourself and mitigate risk, these eight critical elements should be included in every engagement letter. CLIENT NAME. SCOPE OF SERVICES. CPA FIRM RESPONSIBILITIES. CLIENT RESPONSIBILITIES. DELIVERABLES. ENGAGEMENT TIMING. TERMINATION AND WITHDRAWAL. BILLING AND FEES.

Standard on Assurance Engagements (SAE) 3410, Assurance Engagements on Greenhouse Gas Statements, should be read in the context of the Preface to the Standards on Quality Control, Auditing, Review, Other Assurance and Related Services and Guidance Note on Reports or Certificates for Special Purposes, issued by the ICAI ...

The types of functions generally performed by the Chartered Accountant are varied. The more important ones amongst them are discussed below. This includes the writing up of accounts and the preparation of financial statements. It encompasses a wide area ranging from simple Book keeping to complex financial analysis.

No. As per Chartered Accountants Act, Schedule 2 para 1 clause (3) CA shall be guilty if he signs estimated figures. It should be signed only by client himself. First of all , be aware that there is a difference between Provisional balance sheet and Projected balance sheet. .

A Standard on Assurance Engagement (SAE) that provides guidance for auditors who are engaged to examine and report on prospective financial information.

Non-company entities which are not covered under Level I, Level II and Level III are considered as Level IV entities.