Second Request for Correction of Billing Error

About this form

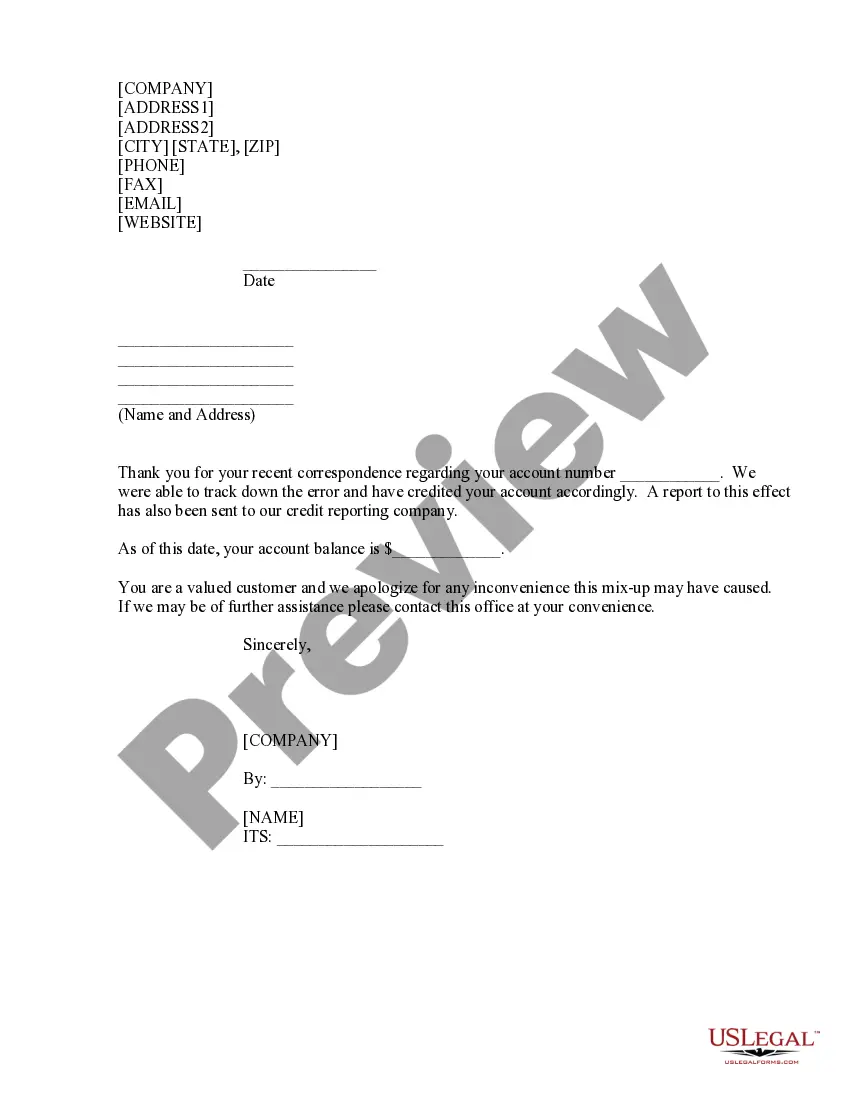

The Second Request for Correction of Billing Error is a legal document used to formally address a billing discrepancy with a creditor. This form assists in documenting your efforts to rectify an error in a previously issued bill, ensuring that the issue is clearly communicated. It differs from a first request for correction by indicating that you have already reached out once and are following up to seek resolution.

What’s included in this form

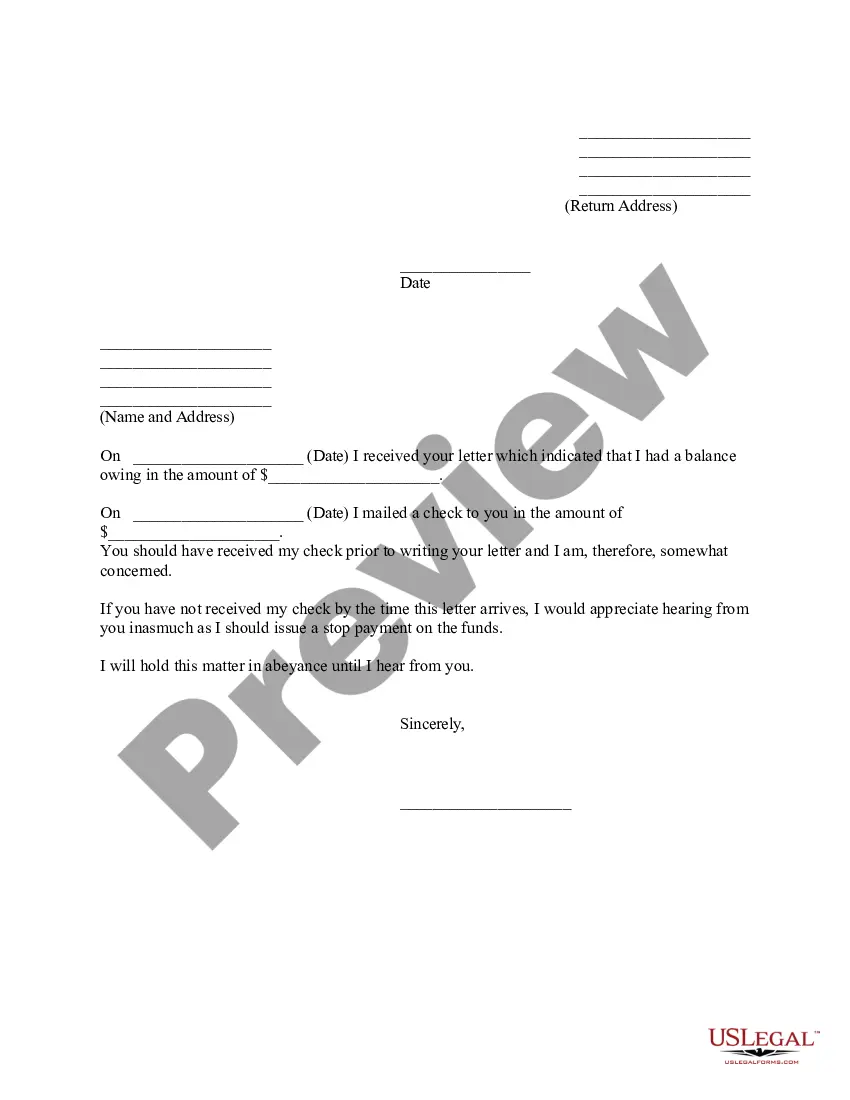

- Return address: Your address where you want a response sent.

- Date: The date you are sending the request.

- Name and address of the creditor: The creditor's contact information.

- Account balance details: Information about the balance you believe is incorrect.

- Details of your previous payment: The date and amount of the payment you made.

- Request for correction: A statement requesting that the error be corrected promptly.

Common use cases

You should use the Second Request for Correction of Billing Error when you have previously notified a creditor about a billing discrepancy and have not received a satisfactory resolution. It is effective in situations where you have documentation of a payment that has not been credited to your account, and you need to reinforce your request for correction in writing.

Who this form is for

- Consumers who have noticed billing errors on their accounts.

- Individuals who have already submitted a first request and need to follow up.

- Anyone wishing to formally document communication with creditors regarding billing issues.

Instructions for completing this form

- Fill in your return address at the top of the form.

- Add the date when you are sending the request.

- Provide the name and address of the creditor you are contacting.

- State the date of your previous correspondence and the balance you believe is erroneous.

- Include the details of the payment made, such as the date and amount.

- Sign the form with your name to finalize the request.

Notarization guidance

This form does not typically require notarization unless specified by local law. Always confirm your specific state's requirements to ensure compliance.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to include your return address or the creditorâs address.

- Not mentioning the date of your previous payment.

- Omitting important account balance details.

- Neglecting to sign the form.

Advantages of online completion

- Instant access to a correctly formatted legal document.

- Ability to download and complete the form at your convenience.

- Guidance from licensed attorney-drafted templates, ensuring compliance with legal standards.

Looking for another form?

Form popularity

FAQ

I am writing to dispute a charge of $ to my credit or debit card account on date of the charge. The charge is in error because explain the problem briefly. For example, the items weren't delivered, I was overcharged, I returned the items, I did not buy the items, etc..

You generally have at least 60 days to dispute credit card charges when there's a billing error or fraudulent transaction, and 120 days if you have a complaint about the quality of goods or services.

Billing Errors: You can dispute a billing error up to 60 days after the date your bill was issued. Some credit cards give you more time, but make sure you dispute the error as soon as possible.

The creditor must send you written acknowledgement of your dispute within 30 days, unless the problem has been resolved. The creditor cannot take any legal action against you while your complaint is pending. The creditor must investigate and resolve your dispute within two billing cycles, but no more than 90 days.

The credit card company must acknowledge receipt of your dispute notice within 30 days, unless it corrects the bill within that time. Then, within two billing cycles?but not more than 90 days?the company must either correct the error or explain why it believes the amount on the statement is correct.

There has surely been a mistake. Therefore, I request you to kindly recheck and update your records and issue me a fresh bill. As proof I am attaching herewith last month's bill payment receipt. I hope to receive the correct bill soon and settle our obligations for this month as soon as possible.

For purposes of this section, the term billing error means: (1) A reflection on or with a periodic statement of an extension of credit that is not made to the consumer or to a person who has actual, implied, or apparent authority to use the consumer's credit card or open-end credit plan.

If you believe an error has been made on your credit card bill, you should send your credit card company a written letter within 60 days of the charge appearing on your billing statement. The letter should include information that identifies yourself and what you are disputing.